Blackstone’s flagship property fund failed to generate enough cash to cover its dividend last year, putting strain on a vehicle the private capital group views as a beachhead in the retail investor marketplace.

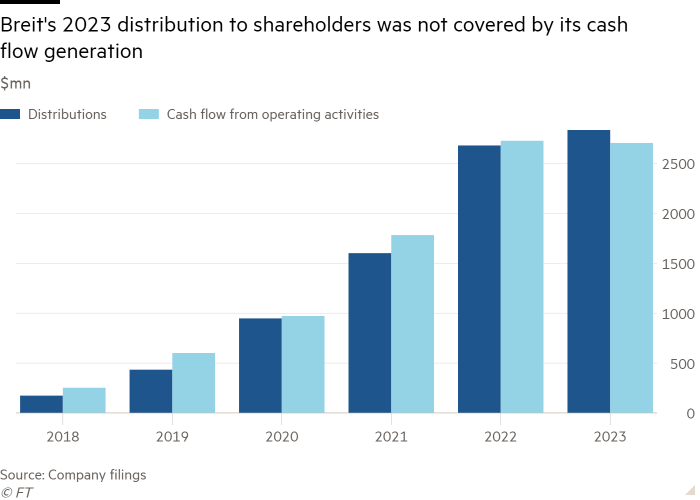

The $60bn Blackstone Real Estate Income Trust generated $2.7bn in cash flows in 2023, mostly in rents from a portfolio spanning thousands of warehouses, apartment buildings and data centres across the US, according to its annual report.

It paid out a distribution of more than $2.8bn, resulting in the first annual shortfall of cash from operations to cover payouts to shareholders.

The deficit underscores risks for tens of thousands of individual investors who have ploughed money into the unlisted property fund, Blackstone’s first product for wealthy retail investors.

Property investors widely consider payout ratios exceeding cash flows to be a problem in the long term. Reits tend to pay out 90 per cent of income but anything over 100 per cent is seen as unsustainable because funds might eventually need to take on more debt, issue new shares or sell assets to fund dividends. Funds not earning enough to handle dividend payments are often forced to cut payouts.

“I would always be cautious about any company that does not have its dividend covered,” said Nate Koppikar, a partner at hedge fund Orso Partners, which has bet against Blackstone shares.

Most publicly listed property trusts in the US can handily cover dividends using cash flows from rents, according to Green Street, a commercial real estate research group.

“For the most part, in the listed Reit world, dividend coverage is just fine,” said Michael Knott, head of US Reit research at Green Street. Listed Reits on average currently cover 125 per cent of their dividend payouts from cash flows, he said.

By contrast, Breit struggled to cover its distribution with cash flow from operating activities. Those cash flows covered just 95 per cent of the payout in 2023, according to its annual report.

Breit’s cash flows from operating activities fell slightly in 2023 as it sold property and left cash in liquid investments to meet redemptions. It has sold property for gains to make heavy investments into data centres that are still being completed and not generating rent.

Its cash flows were also lowered by the timing of property purchases, sales and collections of rental revenues, and payments of expenses, among other factors, according to people briefed on the matter.

Despite the modest decline in cash flow, Breit’s total distributions grew nearly 3 per cent, mostly as a result of an increase in average shares outstanding during the year, according to securities filings.

Breit discloses other metrics more commonly used by public real estate investment trusts. Its adjusted funds from operations, which Green Street uses to analyse public property trusts, was $2.1bn, or 74 per cent of dividends, while Breit’s “funds available for distribution” were $1.7bn, or 61 per cent.

Large private property trusts similar to Breit managed by investment groups, including Starwood Capital and Brookfield, also reported cash flows falling short of distributions in 2023, filings show.

People close to Blackstone acknowledge that Breit did not fully cover its distribution in 2023, but said its cumulative cash flow from operations since its 2017 creation has covered 103 per cent of its payout due to high coverage ratios in prior years.

The shortfall is not creating a cash crunch for the fund because just over half of Breit investors elect to take their dividend in cash, while the remainder take their distribution in additional shares, they noted. Breit’s cash flows did cover the cash portion of its dividend.

The people also noted that any shortfall will not affect investors’ overall returns because it will be met with a corresponding drop in the fund’s net asset value. Breit has generated a 10.5 per cent annualised total return inclusive of distribution since its creation, according to Blackstone’s calculations.

“Breit covered more than 95% of 2023 distributions with cash flow from operations. Any excess distributions are fully reflected in Breit’s reported net asset value, resulting in zero impact on total returns,” Blackstone said in a statement.

Breit has more than $8bn in liquidity, it recently told investors.

The shortfalls come amid heightened anxiety over real estate values and Breit in particular.

In December 2022, Blackstone was forced to put limits on a flurry of redemption requests from cash-hungry investors. In recent months, Breit has been able to fulfil all of its redemptions, a positive trend for the fund. Yet investors continue to pull billions of dollars each quarter.

Blackstone has prominently featured Breit’s distribution yield of 4.6 per cent in marketing materials. The yield has been a significant draw for many investors who ploughed more than $50bn into the fund between 2017 and 2022, when rock-bottom interest rates meant there were few products that offered similar returns.

In its financial filings, Breit warned that if it is unable to generate enough cash flow from operations to fully fund the distribution, the payout may be made through additional borrowings, asset sales or a return of investor capital that would “result in us having less funds available to acquire properties or other real estate-related investments”.

“As a result, the return you realise on your investment may be reduced,” a filing said, while noting that such measures could “negatively impact our ability to generate cash flows” or “dilute your interest in us on a percentage basis and may impact the value of your investment”.