A couple of weeks ago, Alphaville wrote that sterling looked doomed, with dollar parity seemingly inevitable in the next few months.

We weren’t expecting things to move this quickly, and for all the good parity headlines to be used so quickly. Following Friday’s ‘Fiscal Event’ (a phrase that surely deserves to become shorthand for ‘Post-Budget market boke’), UK assets have had quite a time.

Just writing about daily UK market moves feels like catching a falling knife (good luck, punters). The pound, at time of pixel, had turned negative against the dollar:

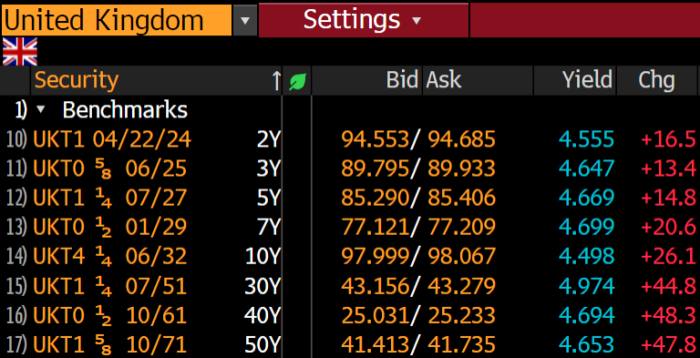

Meanwhile gilts, which are generally a more troublesome area, suffered some serious indigestion at the long end Tuesday. Eww:

Let’s focus on sterling for the moment.

The flash crash in cable to $1.035 on Monday, which landed during thin Asian trading, was a rude awakening for the UK but probably needs to be treated as an anomaly for now. The pound bounced back as London trading kicked into gear, and was calmish until Andrew Bailey cracked out the monetary policy version of texting “OMG I only just saw your messages!!! Let me know if you still need help xx” days after your friend gets run over.

It was enough to prompt a couple of decisive sellside calls on the imminence of pound-dollar parity. Robin’s written a great piece today explaining why the UK is so defenceless against this decline.

Nomura’s, released early yesterday afternoon, was probably the most eye-catching (their emphasis):

What we witnessed this morning, with the slight recovery in GBP from the depths of sub-1.04, is likely to be short-term profit-taking rather than any material reason for cheer. Short GBP and short gilts is a very consensus trade but that doesn’t mean it is not the right one to hold from here. None of the above risks to holding GBP shorts change the medium-term message from the UK’s collapsing terms of trade: we now expect GBP to reach parity by end-November, 0.975 by year-end and 0.95 in Q1.

Jane Foley at Rabobank, which is in the process of revising its $1.08 medium-term target for cable, adds:

GBP/USD has edged higher in early European hours this morning, suggesting the extreme cheapening of UK assets over the past couple of sessions is attracting some interest. That said, the causes of the sell-off in both gilts and in GBP have not been addressed and this suggests that the pound remains an extremely vulnerable currency.

Kit Juckes from Société Générale agrees that this is just the “eye of the storm” for sterling:

As for sterling, there will be plenty of volatility ahead and with no new news likely to emerge, the next bout of weakness will come along soon enough.

But you’re in the process of swapping your pound for dollars/gold/bitcoin/Beanie Babies, wait! It’s not all grim. Credit Suisse’s strategists reckon that sterling may have hit the bottom, and close out their bearish stance . . .

While GBP shorts had already been built up over the past month, the level of bearishness was not extreme until recently. This dramatically changed with the government’s fiscal announcement on Friday. In fact, option markets — judging by the more timely pricing of risk reversals — suggest that GBP bearishness increased rapidly to levels not seen since the Brexit referendum in 2016. As such, downside risks to the GBP are rapidly and increasingly priced in, and may turn out more symmetric in the near term.

And Berenberg’s Kallum Pickering has chimed in with the “hang on everyone . . . ” take:

We do not rate the drop in sterling to a record low versus the US dollar as the start of a genuine currency crisis. To some extent, it is a typical response to a change in policies. But as is often the case, markets have overdone their reaction. Even with larger fiscal deficits, the UK remains a solid advanced economy with trend growth of c1.5% per year. The UK does not have large external liabilities in a foreign currency and will almost certainly be able to meet its debt liabilities in its own currency for the foreseeable future. The UK borrows in its own currency and has the longest average debt maturity in the OECD of c16 years.

As philosopher Billy Ray Cyrus once said, there is much to think about.

Things remain febrile and fast-changing. But for now, here are the two pounding questions keeping us up at night:

-

If parity, when?

-

If parity, who cares?

Neither question is easy to answer, but here’s a rough attempt:

When?

The events of Friday/Monday were a keen reminder that shit, to use the technical term, happens. Everyone has a price target until they get punched in the face.

This makes it hard to guess exactly when parity might occur. But options markets, as is their wont, reflect a couple of views. Traders finally began making reasonable near-term bets on parity yesterday: a one-month view of cable options shows puts at the $1 and $0.98 strikes, on October 10th and 26th respectively. These aren’t huge wagers (the option of the 26th is a notional of just £100mn), but their newness shows a shift in attitudes about when parity might happen.

November seems relatively quiet, all things considered, with just one sub-parity put evident ($0.99 by the 28th, in an option also bought yesterday), but this might just be a matter of proximity:

Who cares?

That’s a really interesting question, thank you. Who does care? After all, parity ain’t nothing but a number. That attitude certainly seems to have some sway with Prime Minister Liz Truss, per Sky News’ Sam Coates:

Faced with market turmoil, spiking borrowing costs, and the drop in the value of the pound in the foreign exchange markets, the prime minister’s initial instinct was to stand firm and say little or nothing, unwilling to look like she might be shifting position .

The government will reject claims circulating in Whitehall that the meeting between Ms Truss and Mr Kwarteng was “argumentative” and descended into a “shouting match”.

Noice.

Let’s be realistic. In the fuzzy world of political economy, a pound being worth a dollar would be a big stain on an incumbent government. Parity — whether or not this is justified by pure economics — would draw huge media attention and criticism.

To be clear, public perception is not currently a strong suit for the government. Per The Times today:

Labour has surged to its largest poll lead over the Conservatives in more than two decades, with voters turning against Kwasi Kwarteng’s tax-cutting budget. A YouGov poll for The Times today puts Labour 17 points clear of the Tories — a level of support not seen since Tony Blair won his landslide victory in 2001.

The survey that data is based on was conducted between September 23rd and 25th, ie before a bunch of headlines pointing out the government had knocked sterling to a record low. We somewhat doubt any of the respondents would, knowing this, have replied “Oh actually that’s the tipping point my export business needed to get off the ground, howay the Tories!”

These are not ideal conditions for the government or the Bank of England, both of which have effectively decided to play for time.

It’s hard to say who’s in a worse spot. The government has no real democratic mandate for what it is doing, is clearly stalling and hoping it can frame the market’s recent repricing as little more than a tizzy.

But the BoE likely has to move more quickly (the MPC will next meet on November third), and is under more direct pressure in the sense that members of the new government have been taking pretty open shots at its credibility.

Despite this, Bailey has chosen to cleave communications extremely closely to Kwarteng. Former MPC member Adam Posen, writing for the PIIE, has done a postmortem on yesterday’s Threadneedle Street comms, which includes this line:

Certainly, I would not have included in the statement the seemingly complimentary comment, “I welcome the Government’s commitment to sustainable economic growth,” when the option was available to make no normative comment at all.

Posen adds (with our emphasis):

Now, the Truss-Kwarteng fiscal policy package has taken the UK policy regime right back to 1974, bringing pound weakness front and centre. The years that followed were the nadir of British postwar economic performance and awful for the British people.

One key difference now is that the Bank of England is independent. That independence should be exercised to put up rates quickly all the while explaining to the public that interest rates will have to go even higher for longer than they otherwise would have, given the government’s fiscal stance and its impact on the pound.

As with Brexit, UK elected officials have the right to disregard predictable and predicted economic costs. And as with Brexit, the Bank was right to stay publicly silent on those costs until the political decision was made. Now, however, the Bank of England should not hesitate to respond to those sad realities and to matter of factly attribute them to the government’s choices.

Posen doesn’t specify a terminal rate expectation, but right now markets are pricing in interest rates at nearly 6 per cent by March:

This opportunity for an “I am Spartacus!” moment might be tempting for the MPC. It could also be, as Pantheon Macroeconomics points out, disastrous. Play ’em off, Samuel Tombs:

Raising Bank Rate to almost 6% also would lead to a sharp rise in mortgage defaults. Borrowers have been stress-tested in recent years to see if they could cope with only a 300bp increase in mortgage rates. The average quoted rate for a two-year fixed- rate mortgage likely would rise to about 6% early next year, if the MPC increased Bank Rate as quickly as markets expect, 400bp higher than two years earlier.

This suggests that households refinancing a two-year fixed rate mortgage in the first half of next year will see monthly repayments jump to about £1,490 early next year, from £863 when they took on the mortgage two years prior. That £627 increase is equal to about 14% of the average household’s disposable income.