Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

“A once-in-a-century pandemic, eruption of geopolitical conflicts and extreme weather events have disrupted supply chains, caused energy and food crises, and prompted governments to take unprecedented actions to protect lives and livelihoods.” Thus does the IMF’s latest World Economic Outlook describe economic events since early 2020.

Yet, overall, the world economy has shown resilience. Unfortunately, however, but unsurprisingly, high-income countries — blessed with more policy space — have shown more of it, while developing countries have shown less. In sum, “[w]hereas the former have caught up with activity and inflation projected before the pandemic, the latter are showing more permanent scars”.

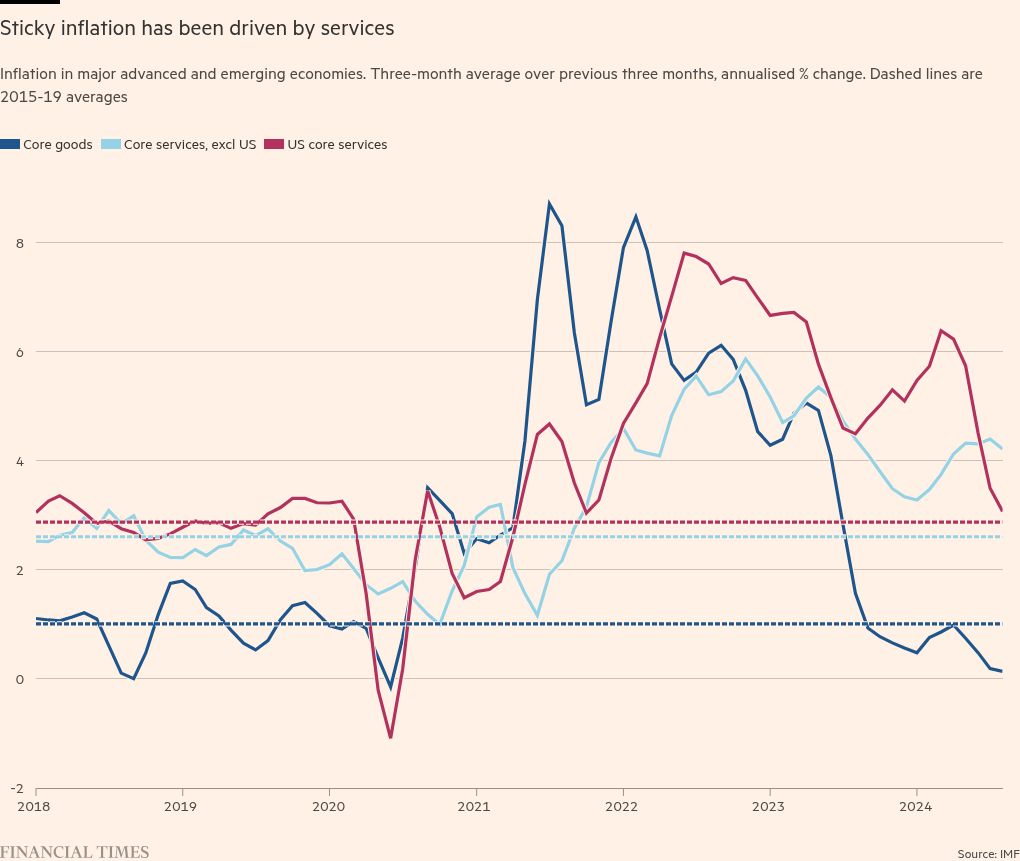

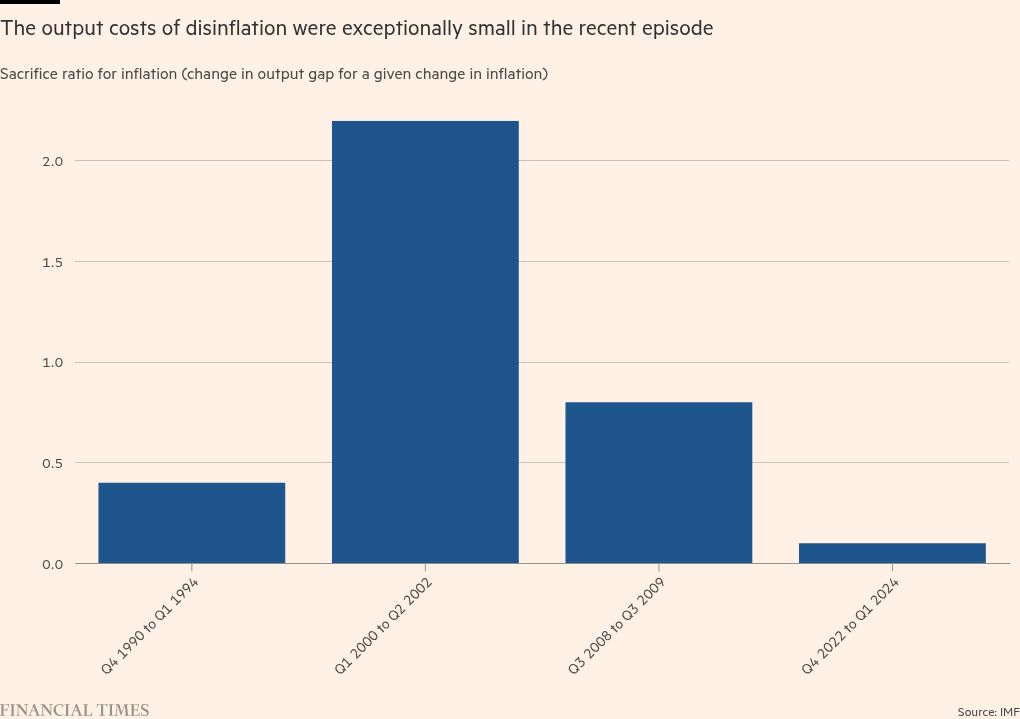

A notable fact, however, is that the largely unexpected upsurge in inflation has subsided at a low cost in terms of output and employment. Yet core inflation has also been showing signs of stickiness, notes the IMF. Crucially, “[a]t 4.2 per cent, core services price inflation is about 50 per cent higher than before the pandemic in major advanced and emerging market economies (excluding the US)”. Pressure to bring wages back in line with prices is the main driver of the robust core inflation in services. But, as output gaps close, the fund hopes, this wage pressure, too, should subside.

Both the spike in inflation and its remarkably painless fall need explanations. These, argues the WEO, include a faster-than-expected decline in energy prices and a strong rebound in labour supply, bolstered by unexpected (and unpopular) surges in immigration.

A more subtle explanation of the behaviour of inflation is that the interaction of surging post-pandemic demand with constraints on supply made the relationship between economic slack and inflation (known as “the Phillips curve”) steeper (or, in economists’ jargon, “less elastic”). Thus, inflation rose more than expected when demand surged, but fell faster than expected as supply and demand came together. Monetary policy played a role in both directions, by stimulating and then restraining demand, but also, when tightened, by reinforcing the credibility of inflation targets.

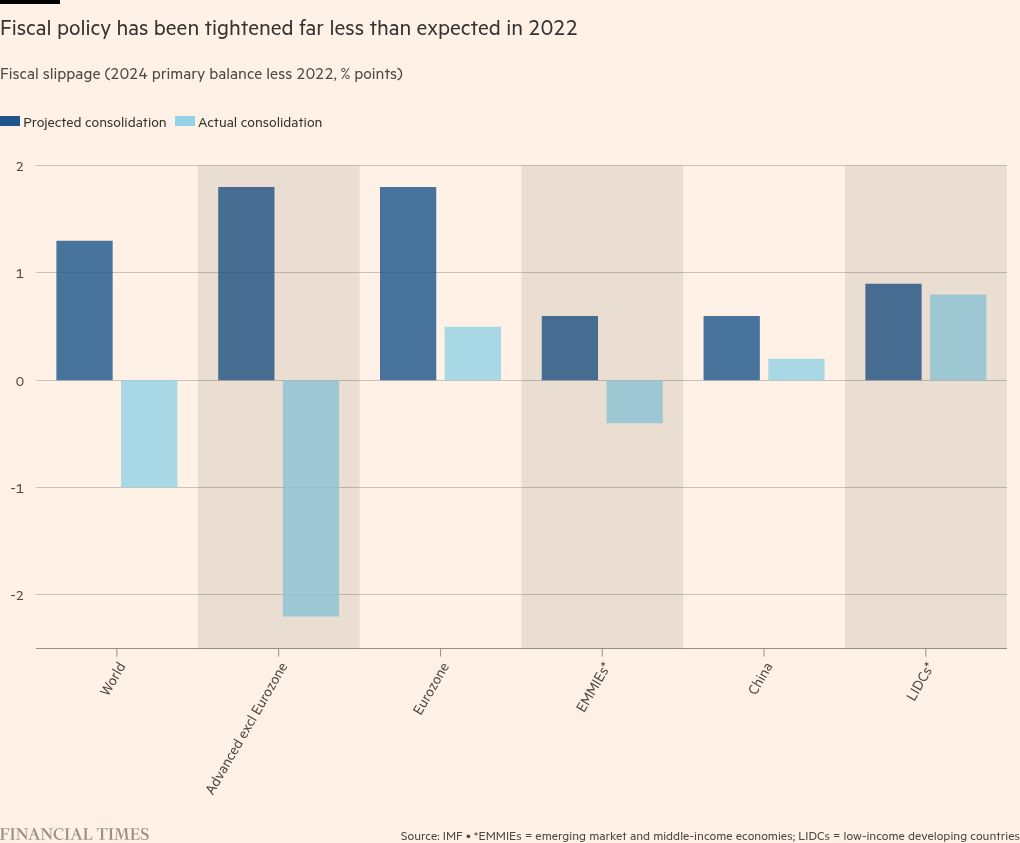

A noteworthy feature since 2020 has been the changing relationship between monetary and fiscal policy. In the pandemic, both were ultra-loose. But, after 2021 monetary policy tightened, while fiscal policy stayed loose, notably in the US. Higher interest rates then increase fiscal deficits. Yet there is a big divergence between the US and the eurozone on fiscal prospects: on IMF projections, US public debt will rise to almost 134 per cent of GDP by 2029; in the eurozone, on the other hand, the ratio of public debt to GDP is expected to stabilise at about 88 per cent in 2024, albeit with large cross-country differences.

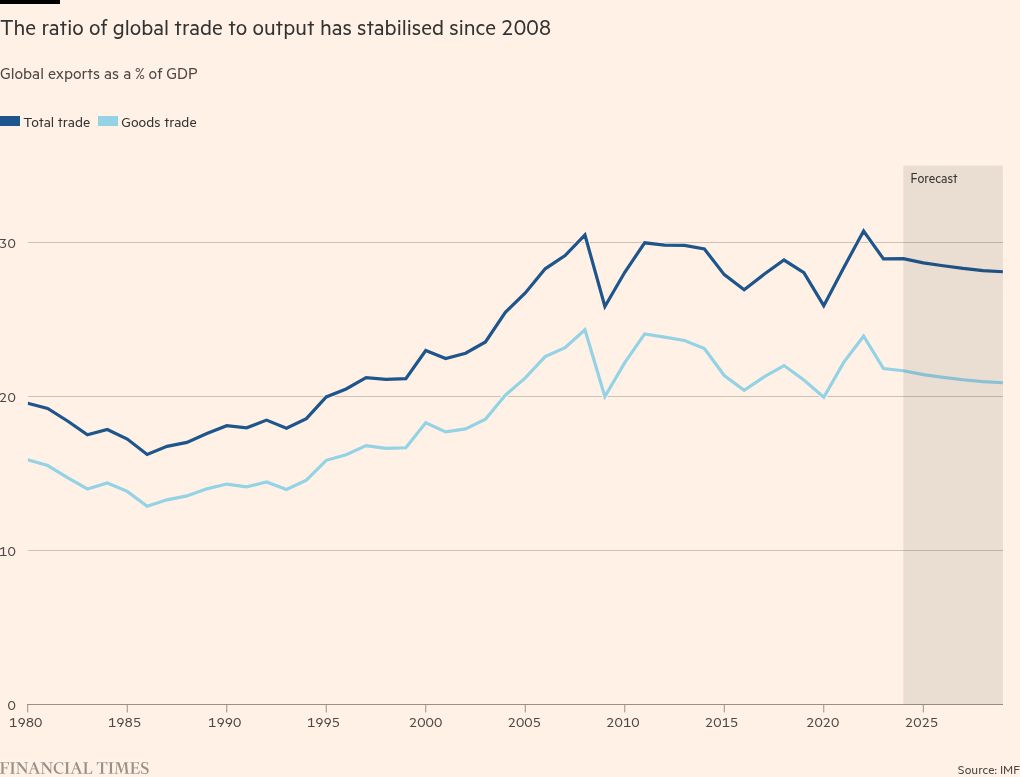

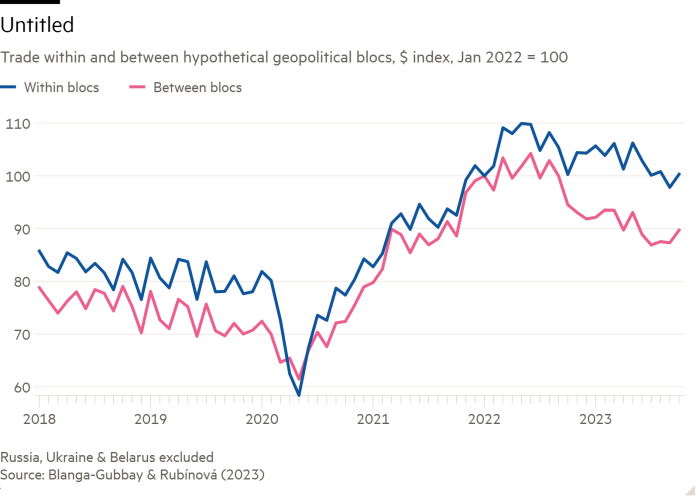

Yet another significant recent feature of the world economy is that since Russia’s assault on Ukraine in February 2022, the rate of growth in trade between “blocs” has fallen more than that within “blocs”, with one centred on the US and Europe and another centred on China and Russia.

The fund has not changed its view much, projecting global growth of close to 3 per cent. This assumes there are no big negative shocks, trade grows in line with output, inflation stabilises, monetary policies loosen and fiscal policies tighten. Its projections show US growth from fourth quarter to fourth quarter falling from 2.5 per cent in 2024 to 1.9 per cent in 2025, while it rises slightly, to 1.3 per cent, in the eurozone. Over the later period, developing Asia’s growth is projected at 5 per cent, China’s at 4.7 per cent and India’s at 6.5 per cent.

Downside risks are, alas, plentiful. Past monetary policy might bite harder than now expected, perhaps generating recessions. If inflation is more robust than expected, monetary policy would be tighter than assumed, which could affect financial stability. The impact of higher interest rates on debt sustainability might turn out to be greater than expected, especially in emerging and developing countries. China’s macroeconomic woes might turn out be greater than now expected, as its property sector retrenches and countervailing policy measures remain too limited. Should Donald Trump become US president and launch his trade measures, the chances of an out-and-out trade war must also be considerable, with unpredictable consequences for the world economy and international relations.

Moreover, will the US election be decided peacefully? The worsening of existing wars or the outbreak of new ones are also possible. Such events could lead to new spikes in commodity prices, possibly (or even probably) aggravated by rapid changes in the global climate.

All this is scary stuff. Yet it is worth noting potential upsides, too. Reform and renewed confidence might lead to an upsurge in investment. Artificial intelligence and the energy revolution might boost investment and growth. It is even possible that humanity will decide that it has better things to do than raise hostility and stupidity to ever higher levels.

The IMF stresses the need to ensure a smooth landing on inflation and monetary policy. It also stresses the more immediate need to stabilise public finances, while promoting growth and reducing inequality. In the medium term, it hopes for stronger structural reform, including improving access to education, reducing labour market rigidities, raising labour force participation, reducing barriers to competition, supporting start-ups and advancing digitalisation. Not least, it desires acceleration of the green transition and enhanced multilateral co-operation.

If only a divinity would compel humanity into being that sensible. In practice, it is, as always, up to us.

Follow Martin Wolf with myFT and on Twitter