Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The scorching rally in Chinese stocks over the past week or so underlines one of the key rules of markets: always keep an eye on the crowd.

Shortly before an extended market holiday, authorities in Beijing sent a forceful message that enough was enough. The economy is stuck (by Chinese standards — most western economies would be delighted with growth rates of a bit above 4.5 per cent) and the stock market had been bleeding out for months.

So the central bank and other authorities unleashed a volley of turnaround measures, ranging from interest rate easing, to lighter demands on banks to stuff reserves away, to direct stock market-boosting efforts and the promise of fiscal support to come. Are these fiscal measures super detailed? No. Will a sliver of a percentage point off interest rates turn the long-suffering property sector around? Also no. But do traders care about that? Again, no.

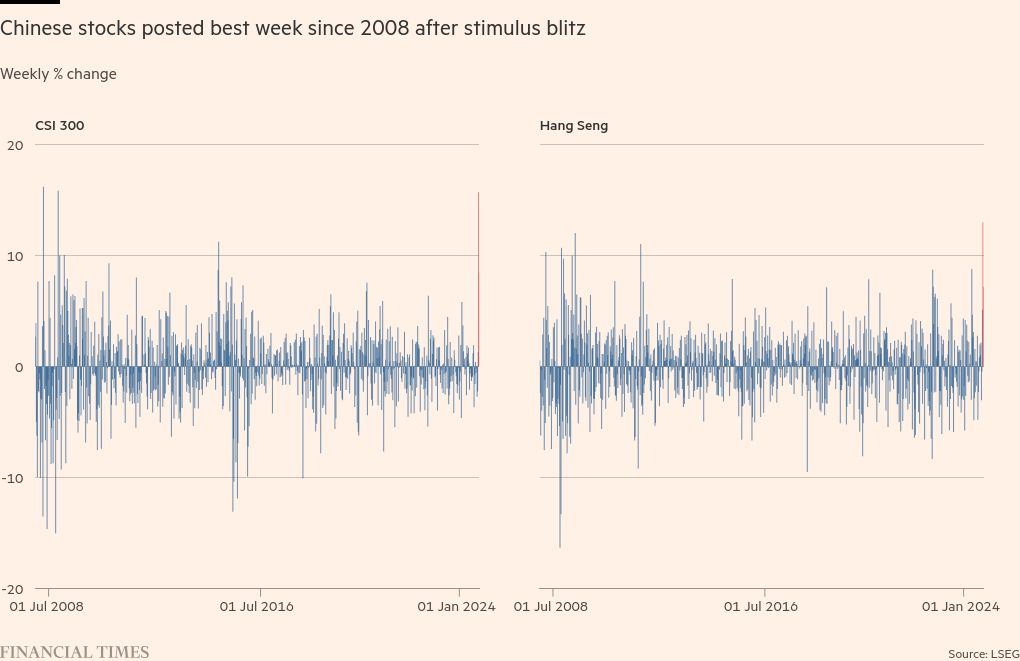

The result, then, is a rip-your-face-off rally for the ages. The CSI 300 index of Chinese stocks added more than 20 per cent in less than a week. Hong Kong’s Hang Seng index is now the best-performing major market in the world this year, having added 30 per cent, compared with a relatively puny 19 per cent in the US S&P 500.

Timing played a role here — the broad assumption was that Beijing would hold out for longer before taking anything like this kind of action. Scale matters, too; Deutsche Bank says the fiscal stimulus is a “big deal” that, when measured against the size of the economy, is the third biggest of its kind for the country ever — a Mario Draghi-style “whatever it takes” moment.

It could take months until we know the real economic impact. But markets are not hanging around to find out. That is because before this injection of support, investors were just allergic to China. Bank of America’s regular survey of fund managers found last month that “macro pessimism was centred on China” with growth expectations at the lowest point in the three years the bank has been tracking them in this form.

At around the same time, I spoke to Amundi’s chief investment officer, Vincent Mortier, who said he had “never seen such a big pushback” from clients against the idea of putting money to work there. He was making the case that it was unwise to avoid China entirely, but the conversation was a non-starter. The bet was “totally, totally dead”, he said.

Pity the hedge fund manager who told me this week he almost took that as a trigger to buy China, but backed out. As any good professional investor will tell you, when everyone seems to hate a particular corner of global markets, it is time to buy. But it can be hard to pluck up the courage.

It is not the first time this year that the power of positioning has been made clear, with the other prime example being Japan. In its quarterly markets review earlier this month, the Bank for International Settlements noted that “concentrated hedge fund positions” played a key role in the speed and size of the Japanese “turbulence” in early August.

Carry trades — selling currencies with low interest rates and buying those with higher rates — were unusually popular with hedgies in the run-up to August’s shake-out, the BIS said. Over the period from 2022, that meant there was a lot of speculative money buying dollars at the expense of yen — a force that helped cram the yen down to its lowest point in decades. Carry trades, and related bets around US stock market volatility, became an unusually weighty influence on hedge fund returns.

At the same time, speculators gravitated towards buying Japanese stocks too. This was all fine until, in early August, it abruptly wasn’t. A scare over US growth that raised expectations of interest rate cuts hit these strategies on several fronts, denting the dollar, particularly against the yen where it was especially stretched, and fuelling volatility in stocks. The exits from this correlated set of trades proved to be crowded on the way out.

Cue an alarming drop in the dollar-yen exchange rate and, on one especially scary Monday, a double-digit decline in the Japanese stock market — the biggest fall since the great crash three decades ago and leaving a shadow over the “buy Japan” thesis that had become popular. “Crowdedness, combined with high leverage, set the stage for the amplification of stress and cross-asset spillovers,” the BIS report said.

Other examples are easy to find, such as the massive accumulation of bets on US chipmaker Nvidia — a stock that became overcrowded over the summer and shed a third in value in six weeks.

With all that in mind, it is worth looking for the points of greatest consensus among investors now, just in case it makes sense to take the other side. For instance, the same survey from BofA that said China was a contrarian buy also pointed to buying commodities, which investors are avoiding on the greatest scale since 2017.

Thematically, the biggest point of consensus is for a soft landing in the US economy — an expectation held by nearly 80 per cent of fund managers. That many clever people can’t all be wrong about something, right?