Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The Chinese ecommerce group behind Temu, whose stock plunged this week after it ruled out investor payouts, has accumulated the largest cash pile of any listed company that does not pay a dividend or buy back shares

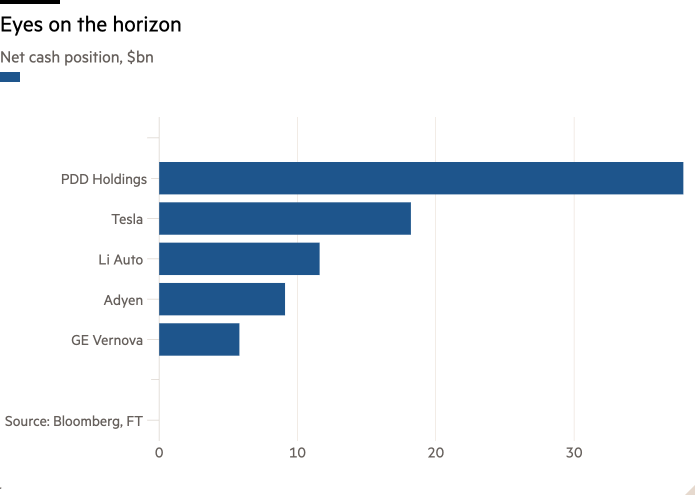

US-listed PDD Holdings is sitting on a $38bn net cash position, according to FT analysis, more than twice the size of the nearest contender, Elon Musk’s Tesla.

While PDD has soared in value as it expanded from China to at least 49 markets in the past two years, its hoarding of cash is regarded as a “red flag” by some investors, who say its financial statements are opaque and its communications sparse.

The Shanghai-based company’s share price fell 31 per cent this week after it warned that record profitability was likely to decline and ruled out dividends or buybacks “for the foreseeable future” in a conference call during which it took questions from only two analysts.

PDD has attracted controversy for the rapid worldwide expansion of ultra-low-cost online flea market Temu, its treatment of staff and suppliers, and its limited financial disclosures as the group grew in size and stock market valuation to rival Alibaba.

Most of the world’s large companies pay dividends or buy back shares, with even the acquisitive and dividend-averse conglomerate Berkshire Hathaway repurchasing billions of dollars in stock this year.

In MSCI’s Investable Market Index, composed of about 2,800 constituents from 47 countries, there were 151 companies with more than $5bn of net cash on their balance sheet as of Wednesday, according to Bloomberg.

Of that cash-rich elite, only five do not pay dividends or buy back stock, an FT analysis found: PDD, Tesla, Chinese electric-car maker Li Auto, European payments group Adyen and GE Vernova, the electric turbine group spun out of GE in April.

Large Chinese companies announcing new buybacks this week include a $5bn programme at JD, a long established rival to PDD, $1bn worth at food delivery group Meituan, and a $1.3bn facility at sportswear group Anta.

PDD generated $6bn of operating cash flow in the second quarter, taking its holdings of cash and short-term investments to $39bn.

The company also has a further $9.3bn of longer-term investments, said to mainly include time deposits and debt securities that PDD declined to detail further. The total for cash and long-term investments is equivalent to 36 per cent of PDD’s $133bn market capitalisation.

Following this week’s results, analysts at JPMorgan wrote in a note to investors that “disclosures by the company remained too limited to understand the drivers behind the financial numbers”, and that “investors are confused by PDD’s unclear guidance and investment strategy”. The bank retained its “overweight” recommendation towards the stock.

Two hedge fund investors with positions in other ecommerce stocks but not PDD both said they considered its lack of share buybacks a “red flag” that could signify potential issues with accounting or the quality of balance sheet assets.

PDD told the FT that “each company makes decisions based on its unique circumstances and strategic considerations. To imply that there is a ‘red flag’ simply because Company A does not follow the same approach as Company B is, quite frankly, absurd.”

A spokesperson added that PDD encouraged investors with specific concerns to reach out to the company, and drew the FT’s attention to a letter to shareholders published in its 2018 prospectus.

The letter said: “It is not easy to take the leap of faith believing in such an unconventional company, which strives to meet both economic and social needs of users, and to make a positive impact to the society.”

Additional reporting by Joseph Cotterill