Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Turkey’s central bank has handed back to Saudi Arabia a $5bn deposit, underscoring Ankara’s progress in replenishing its foreign currency stores as part of its economic turnaround effort.

The deposit agreement Turkey forged with the Saudi Fund for Development in March 2023 was terminated by mutual agreement, the Turkish central bank said on Wednesday.

Turkey’s move to unwind the agreement is the latest sign of how President Recep Tayyip Erdoğan’s pivot to more conventional policies following his re-election in May 2023 is steadying the country’s $1tn economy.

“Turkey is on the right track and is moving towards its goals with sure steps,” Erdoğan told members of his Justice and Development party in parliament on Wednesday, pointing to the recent decision by Moody’s Ratings to increase Turkey’s junk-level credit rating two notches.

Policymakers, led by finance minister Mehmet Şimşek, have made it a priority since the new economic programme was put into action a year ago to refill Turkey’s foreign currency coffers that were depleted in recent years.

Erdoğan’s previous insistence on holding interest rates at ultra-low levels despite scorching inflation had sent Turks rushing into dollars. The low rates combined with huge pre-election giveaways also ignited runaway demand for imported goods, sharply widening the current account deficit.

The race into dollars and yawning current account deficit severely eroded the central bank’s foreign currency reserves, and were widely seen by local and foreign investors as a major economic vulnerability. The $5bn Saudi Arabian injection was seen as a show of confidence that Ankara would eventually turn around its economy.

A series of interest rate rises that began in June 2023, which have brought the central bank’s main interest rate from 8.5 per cent to 50 per cent, has lifted the rates Turks can earn from holding lira. That has prompted local savers to begin swapping some of their dollar holdings to the local currency.

At the same time, a strong influx of dollars and euros from international tourists and a moderation in consumer demand for imported goods has helped reduce Turkey’s current account deficit, relieving pressure on the central bank’s reserves. Foreign investors have also been warming to Turkey’s markets, pumping about $12.5bn into local government debt since last June.

“Our reserves have strengthened as a result of increased foreign resource inflows, reverse dollarisation and decreasing external financing needs with our [economic] programme,” Şimşek said on Wednesday.

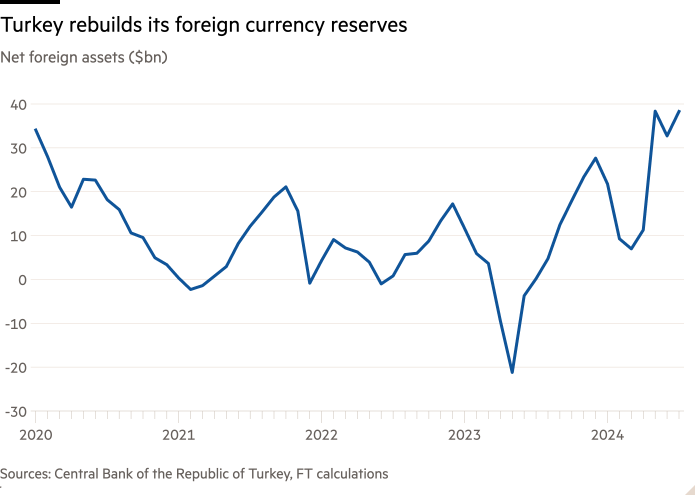

Net foreign assets, a proxy for foreign exchange reserves, have recovered to about $38bn from minus $21bn directly after the May 2023 election, according to Financial Times calculations based on official data.

The removal of the Saudi deposit is not expected to affect the net figure since it sat both in the bank’s gross reserves and liabilities, according to Haluk Bürümcekçi, an Istanbul-based economist.

Şimşek said that despite the termination of the deposit agreement, “our co-operation with Saudi Arabia on economic and financial matters will continue”.

In a sign of how a years-long normalisation process between the two countries remains intact, two senior Saudi officials visited Turkey this month. Defence minister Prince Khalid bin Salman signed a memoranda of understanding with Turkish defence companies while foreign minister Prince Faisal bin Farhan signed a protocol to create a co-ordination council after meeting with Erdoğan in Istanbul.

During his visit, Prince Faisal “emphasised significant progress in Saudi-Turkish relations across political, economic and security domains,” according to a statement published by the official Saudi Press Agency.