Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Political upheaval in Paris is prompting the financial vulnerabilities of the Eurozone’s second-biggest economy to be reappraised, investors have warned.

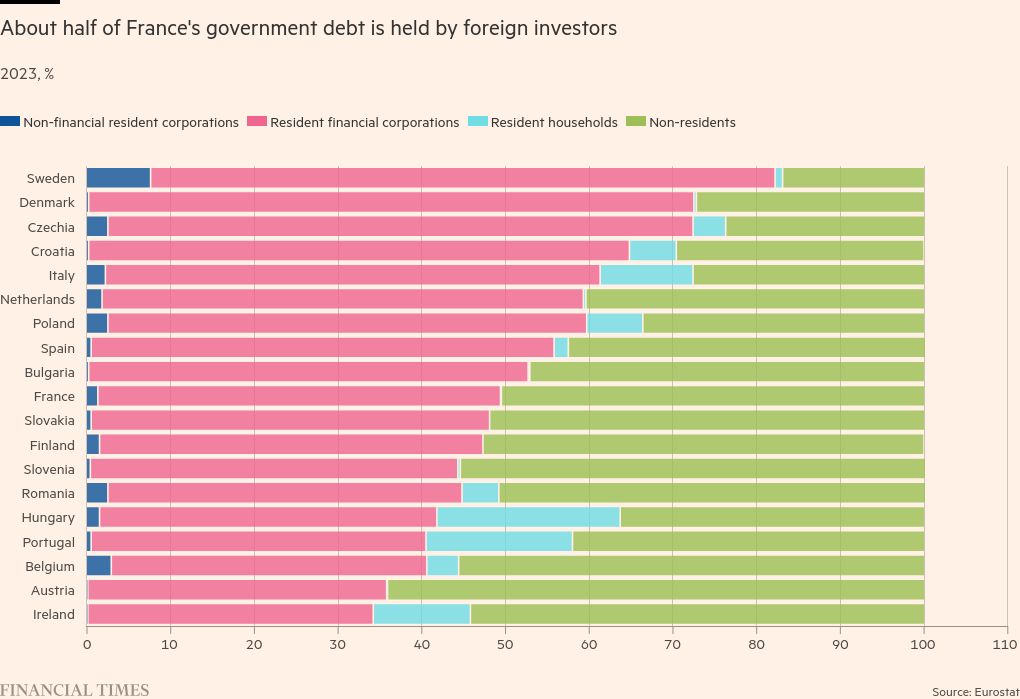

Many fear that the prospect of dysfunctional politics, flagging growth and a steadily rising debt burden may dent France’s long-term attractiveness to foreign investors who hold around half the country’s government debt.

Traders doubt that this will result in turmoil akin to the gilts market crisis triggered by former UK prime minister Liz Truss in 2022, as the country’s finance minister has warned. But they fear that France’s bond market could increasingly resemble Italy’s over time, facing permanently higher borrowing costs and becoming a potential flashpoint when bloc-wide crises hit.

“This is causing some consternation amongst those investors who maybe have been complacent about France’s political risks and fiscal sustainability risks,” said Mark Dowding of RBC BlueBay Asset Management.

If France enacts the wrong policies over time, “there is no reason why it can’t end up in a situation akin to where Italy sits today,” he added.

Borrowing costs have already widened in response to the prospect of either the far-right Rassemblement National forming the next government, or the increasingly likely prospect of an unstable hung parliament.

Since President Emmanuel Macron announced a snap election early last month, the gap between yields on 10-year French and German debt — a measure of risk — has rocketed from 0.48 percentage points to 0.85 percentage points last week, although it has since fallen to 0.71 percentage points.

According to Rohan Khanna of Barclays, the yield on French bonds is at its highest level relative to a combination of those on ultra-safe German Bunds and traditionally riskier Spanish debt since the beginning of the 2000s.

The first-round victory of Marine Le Pen’s RN and its allies on Sunday and the NFP’s second-place finish have bolstered fears of further political turmoil ahead of the second round on July 7. It has also intensified market fears of either political deadlock or a potential move away from market-friendly policies, which could damage confidence after the election.

Pollsters believe a hung parliament or an outright majority for the RN are the most likely outcomes after the second round. In the case of a strong finish for the RN, President Emmanuel Macron could face an uncomfortable power-sharing arrangement with the far-right known as “cohabitation”.

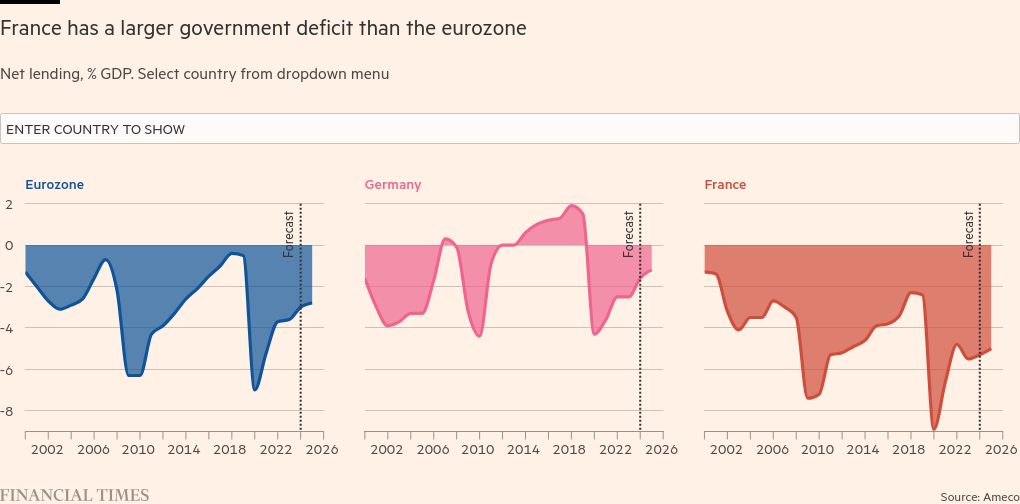

The uncertainty comes at a time of budgetary weakness in France. S&P Global lowered its credit rating in May, following a downgrade by Fitch. France is forecast to run a budget deficit of 5 per cent of GDP next year, modestly down from 5.3 per cent this year but still one of the highest in the EU and above that of Italy, according to the European Commission.

France is also reliant on overseas investors — including a big cohort of Japanese institutions looking for secure European sovereigns — to buy its bonds. While this gives it a more diversified investor base than some, it also leaves it more vulnerable to a sharp change in sentiment, say analysts.

Half of French government debt is held by non-residents, compared with about 27 per cent in Italy and 43 per cent in Spain, according to Eurostat data. While Italian households hold 11 per cent of the country’s debt, that figure for France is 0.1 per cent.

Markets are nervous about what the Japanese investors will do in particular, as shifts in Japanese monetary policy could make their trades less profitable, said Tomasz Wieladek, an economist at T Rowe Price.

On June 19, the commission proposed opening an excessive-debt procedure for France, as Brussels warned of “high risks” emerging from its debt sustainability analysis over the medium term. The general government debt ratio is on track to rise continuously to about 139 per cent of GDP in 2034, it stated.

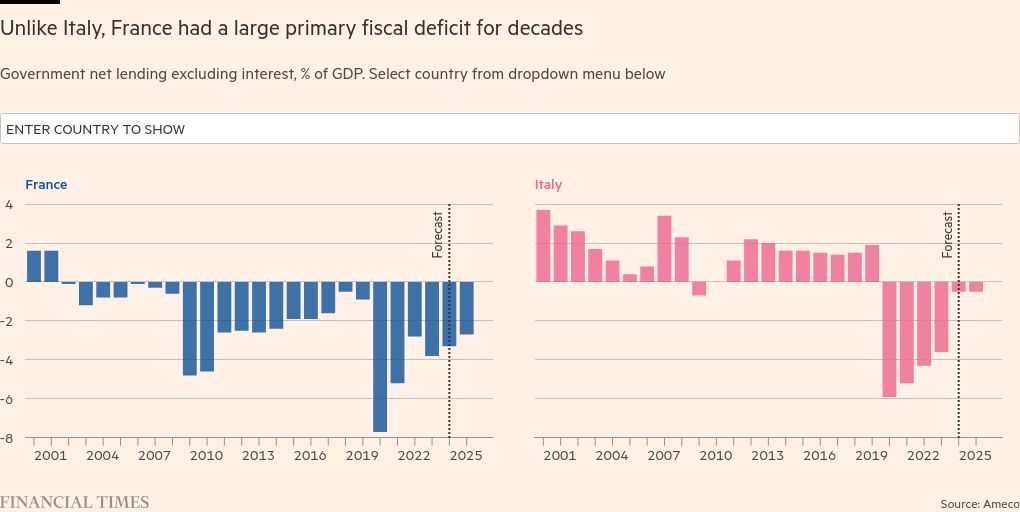

France has so far avoided the kind of crises experienced in Italy and the UK in recent years. In 2018, the spending plans of Italy’s coalition of the Five-Star Movement and the League party pushed the gap between Italian and German 10-year bond yields to more than 300 basis points. That was the highest level since the aftermath of Silvio Berlusconi’s premiership, reflecting investors’ assessment of Italy’s political risk.

Analysis by JPMorgan suggests France could weather a sudden leap in borrowing costs. A “shock” under which borrowing costs leap by 1.5 percentage points over a two-year period would only lift the debt-to-GDP ratio to just over 115 per cent, marginally above its central projections, the bank said in a recent note.

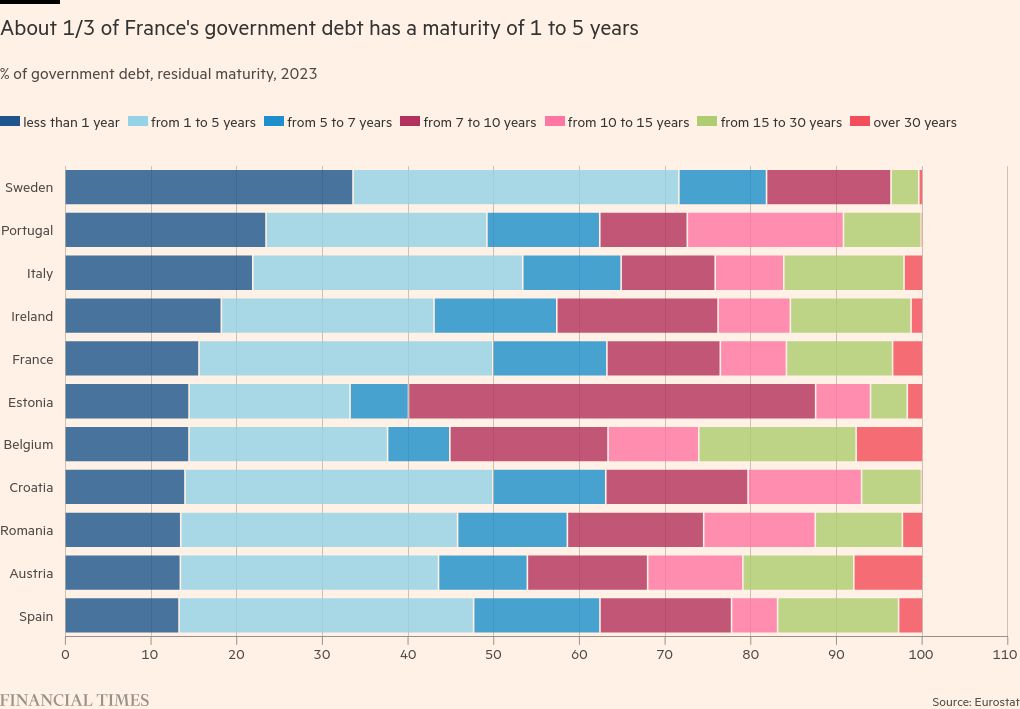

That is partly because France’s debt stock is relatively long-dated, with an average maturity of 8.5 years, according to S&P. That means that just 8-10 per cent of its debt comes up for refinancing every year, according to Barclays, slowing the impact of a rise in borrowing costs.

“The Liz Truss scenario seems unlikely at this point — I don’t see a sudden disruption to the French bond markets,” said Holger Schmieding, chief European economist at Berenberg, who predicts Le Pen’s party will seek to be relatively moderate on fiscal policy.

However, the country’s long-term fundamentals are not good, Schmieding said, especially if France diverges from Macron’s pro-growth policies. A confrontational approach with Brussels is seen as raising the risk of wider turbulence in the EU. Some investors also worry that a wider sell-off in French debt would spark contagion in other European countries, forcing the European Central Bank to intervene.

France’s public debt rose above 115 per cent of GDP in 2020, nearly double that in 2007. Last year, its debt-to-GDP ratio was the EU’s third-largest, after that of Greece and Italy, at 111 per cent of GDP.

Against that backdrop, Schmieding pointed to the potential for higher borrowing costs or further credit rating downgrades, particularly if growth falters.

“It adds up to a serious fiscal issue over the longer term,” said Schmieding.