The change in focus at the Fund Forum in Monaco last month was striking. At previous gatherings, the audience of European asset and wealth managers listened to panels highlighting ESG investments and emerging markets. But, in 2024, these once in-vogue topics have been replaced by geopolitics and artificial intelligence.

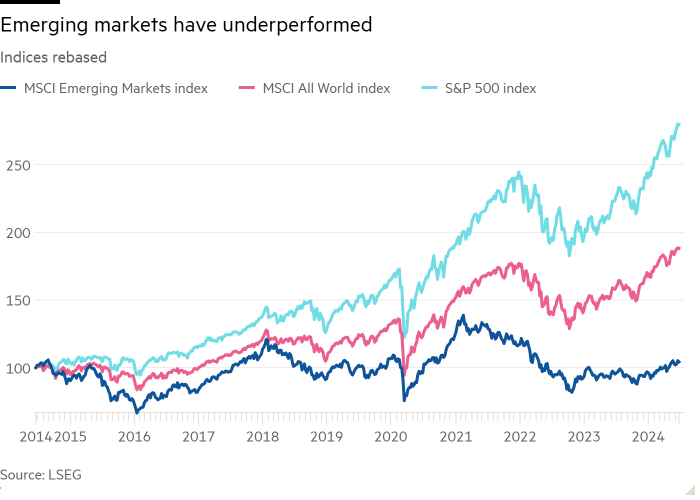

“Family offices have largely fallen out of love with emerging markets, due to underperformance of EM stocks — led by Chinese stocks — since 2021,” explained Edmund Shing, global chief investment officer at BNP Paribas Wealth Management, shortly after appearing on the opening panel of the Monte Carlo event.

Outperformance of US large-cap stocks also contributed to portfolio managers changing their allocations, as did heightened geopolitical risk around China and foreign exchange volatility in countries such as Turkey.

At the same time, index funds’ weightings underwent a similar rebalancing. Their exposure to the developing world fell due to its markets’ underperformance, while US equities’ outperformance has driven increased exposure to North American themes, such as the so-called “Magnificent Seven” tech companies.

It is a shift that partly mirrors some asset managers’ view of a world divided into two blocs: one democratic and investible, the other authoritarian and opaque.

“Emerging markets are more difficult to analyse and understand, given their drivers are largely geopolitical, FX-and macro-driven,” noted Shing at the Fund Forum event, with investment houses preferring to focus on more transparent US or European stocks.

“The US is one big very liquid market with the same currency,” he pointed out, “while EM is a collection of markets with lower liquidity, country-specific drivers, and a basket of currencies to boot.”

This changing sentiment is backed by the annual Global Asset Tracker (GAT) survey of chief investment officers, carried out by Professional Wealth Management, an FT publication. In 2023, 78 per cent of them rated global EMs as “attractive” or “the most attractive” asset class. In 2024, that proportion had fallen to 38 per cent. US equity is currently the top regional theme. CIOs taking part in the latest survey represent 54 private banks and manage total client assets exceeding $22tn.

Interest in this once ubiquitous asset class has similarly waned in the family offices that manage money for rich dynasties. Again, the reason is EMs’ “massive underperformance” over the past decade versus developed markets, says Didier Duret, Geneva-based head of investment at Omega Wealth Management which oversees the portfolios of wealthy European and Middle Eastern families. “EMs have essentially been victims of deglobalisation of investment flows,” he argues.

Risk factors — political, dependence on China’s fate, market risk and underperformance risk — have all simultaneously increased, according to Duret.

Professional Wealth Management Global Asset Tracker

78%

Proportion of chief investment officers rating emerging markets an “attractive” asset class in 2023

38%

Proportion of chief investment officers rating emerging markets an “attractive” asset class in 2024

He recalls the “golden days”, when the veteran investor Mark Mobius, who once managed close to $50bn in EM assets for Franklin Templeton, criss-crossed Asia “kicking tyres” at thriving factories, and headlining at Fund Forum to share insights with his disciples.

That era’s orthodoxy depended on the ‘Bric’ investment theme — backing the growing economies of Brazil, Russia, India and China — which was popularised by former Goldman Sachs economist Jim O’Neill, who later became a UK government minister.

“Gone are the golden days of the BRICs, where allocations were promoted as strategic,” says Duret. “The current allocation reality in family offices is pragmatic — more tactical, selective and based on proven merit of companies.”

Even so, there are some private banks and investment firms that find exceptions to the arguments for EM divestment. BNP Paribas favours investment in South Korea and Turkey for offering “a combination of value and fundamental catalysts.” The French bank also likes EM sovereign bonds for their high yield and “decent fundamental outlook,” which compare favourably with US and European sovereign and corporate bonds.

Some family offices, meanwhile, are focusing on “specific areas that have a place in the AI sun,” according to Omega’s Duret — which include companies in Taiwan and Malaysia. They also like companies in India and Vietnam that are benefiting from the reorganisation of supply chains.

For several of these investors, India is the EM “bright spot.” “India increasingly looks like the next big thing in geopolitics, as it naturally benefits from the West’s ‘de-risking’ approach towards China,” says César Pérez Ruiz, head of investments at Pictet Wealth Management in Geneva. Southeast Asian nations are also likely to pick up production relocated from China, as a result of the west’s geopolitical rivalry with Beijing.

Shing backed India at the Fund Forum event, although he was careful not to write off Beijing. “High-net-worth investors still buy the Modi India transformation story and potential to catch up with China in economic terms,” he said. But he added: “Chinese stocks, although still volatile, could be a good long-term investment for patient investors at this point.”

Whether portfolio managers and clients are behaving rationally when underweighting developing markets is a moot point, though.

EM portfolio allocations, at 10 to 15 per cent on average, are lower than a GDP-weighted average would recommend, according to Chris Richmond, head of manager research at asset management consultancy WTW.

He puts this down to the fact that holding shares in US exporters gives most investors a built-in allocation to EM dynamics. “If you look through earnings in global equity in the US market, you pick up a huge amount of emerging market exposure,” he says — and this creates less incentive “for a more strategic, longer-term weighting.”

But he does not think this is the best approach to investing in EMs. “We believe we can find a manager who does a really good job in emerging markets and, through active management by engagement, is investing in some world class companies that have dominant positions in their sector,” he explains. “They do exist and that’s a great investment opportunity. It’s just much harder.”