Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The Bank of England is set to keep interest rates unchanged this week as it hunts for clearer signs that pay growth and services inflation are cooling sufficiently to permit a cut in the cost of borrowing.

Financial markets are overwhelmingly betting that the BoE’s benchmark rate will be kept at 5.25 per cent when the Monetary Policy Committee announces its latest decision on Thursday. It would mark the fifth successive meeting that the rate is held unchanged, after 14 consecutive increases.

Pricing in the swaps market — which reflects predictions of the future level of BoE interest rates — suggests the first downward move will only come by August, with one or two further cuts by the end of the year.

Steady monetary policy in the UK this week would chime with the approach of big central banks including the Federal Reserve and the European Central Bank, which are making it clear they will start reducing rates only when they have enough evidence that inflation is heading durably lower.

The ECB kept rates unchanged this month, while the Fed is tipped to do the same on Wednesday.

“‘Not yet’ is the key phrase that unites the message of the Bank of England, the Federal Reserve and the ECB at present,” said Sandra Horsfield, economist at Investec.

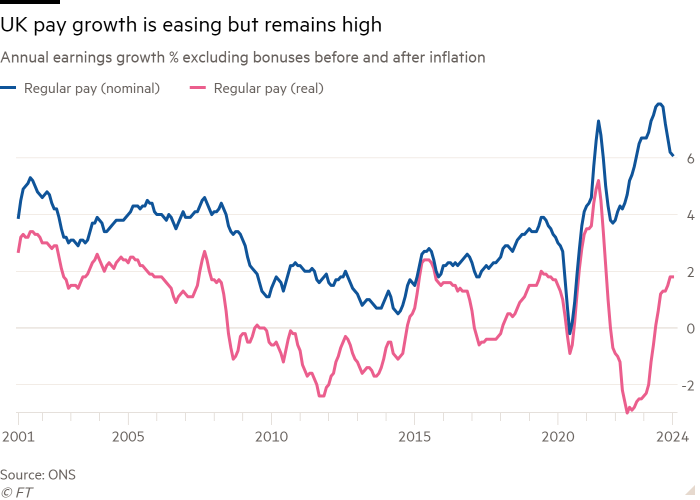

Official data this month pointed to softer conditions in the UK labour market, as slightly slower wage growth combined with a fall in job vacancies, stalling growth in the number of payrolled employees, and an increase in the number of claimants for jobless benefits.

Excluding bonuses, annual wage growth slowed to 6.1 per cent in the three months to January, from 6.2 per cent previously.

But the BoE is wary of putting too much weight on single labour market releases given continued quality problems with Office for National Statistics surveys. In any case the pace of pay growth remained well above levels consistent with the central bank’s 2 per cent inflation target, analysts said.

A crucial question for the MPC will be the shape of pay deals struck by employers in March and April. The median pay increase across the economy has held steady at 5 per cent in the three months to January, according to analysis of pay awards by Incomes Data Research.

However, a quarter of the 63 deals examined were worth 6 per cent or more. A key factor in April is the upcoming 9.8 per cent increase in the National Living Wage — a boost that will also have knock-on effects for the pay of some employees who earn somewhat more than the statutory floor.

Andrew Goodwin, economist at consultancy Oxford Economics, said the recent data did not suggest pay would undershoot the BoE’s first-quarter forecast of 5.7 per cent. “We think the majority of the MPC will be keen to see more data on new year pay settlements before committing to rate cuts,” he added.

Waiting has another benefit: it gives the BoE time to compile a full set of economic forecasts, next due at its May meeting.

Officials at the central bank have also been closely watching growth in services prices, which rose 6.5 per cent in January compared with a year earlier. They see prices charged by the UK’s massive services sector as a key gauge of underlying pricing pressures in the economy.

Although the MPC largely backed rate rises between November 2021 and last summer in an effort to tame inflation, the committee was split three ways when its nine members last met in February.

While two policymakers, Catherine Mann and Jonathan Haskel, opted for an increase in rates to 5.5 per cent, fellow external member Swati Dhingra called for an immediate cut. The majority voted for no change.

BoE governor Andrew Bailey said after the meeting that the central bank had seen “good news on inflation over the past few months”. But he cautioned: “We need to see more evidence that inflation is set to fall all the way to the 2 per cent target, and stay there, before we can lower interest rates.”

Pressure for rate cuts is likely to rise in the coming months as headline inflation drops rapidly to the 2 per cent target, thanks to lower energy prices. Consumer price inflation is now at 4 per cent, compared with its 2022 peak of more than 11 per cent.

Official inflation figures for February are due on Wednesday, with the headline rate of CPI inflation expected to drop further to 3.6 per cent, according to a Reuters survey of analysts.

The BoE predicted in February that, after bottoming out in the second quarter, price growth would probably start trending higher later in 2024, bolstering arguments for the central bank to keep policy restrictive.

Other forecasters including the Office for Budget Responsibility, the fiscal watchdog, question the idea that CPI inflation will quickly bounce back.

Markets see both the Fed and ECB announcing rate cuts this summer. Officials at the BoE have been coy about the likely timing of their first reduction, with chief economist Huw Pill recently insisting that he thought the time for the first move remained “some way off”.

“The BoE probably requires more convincing to actually start the ball rolling” on rate cuts, said Allan Monks, UK economist at investment bank JPMorgan. “It is aiming to avoid having to potentially retrace its steps after beginning to ease, and may struggle to contain expectations after it has started.”