Federal regulators are preparing to seize First Republic Bank as soon as this weekend, while major banks including JPMorgan Chase and PNC are vying to buy the lender once it enters receivership, according to multiple reports.

If the San Francisco-based lender falls into receivership, it would be the third US bank to collapse since March, in addition to the Swiss government-brokered buyout of European giant Credit Suisse by UBS.

After failing to find a private buyer for First Republic this week, the US Federal Deposit Insurance Corporation has decided that the bank’s position has deteriorated to the point that time has run out for a private-sector bailout, sources told Reuters.

The FDIC, after gauging initial interest earlier this week, has asked major banks including JPMorgan and PNC to submit their final bids to buy First Republic in receivership by Sunday, according to Bloomberg News.

That suggests the regulator could be planning a swift move to seize First Republic, and then transfer control to a private buyer before the bank reopens for business on Monday morning.

Federal regulators are preparing to seize First Republic Bank as soon as this weekend. JPMorgan Chase and PNC are reportedly vying to buy the lender once it enters receivership

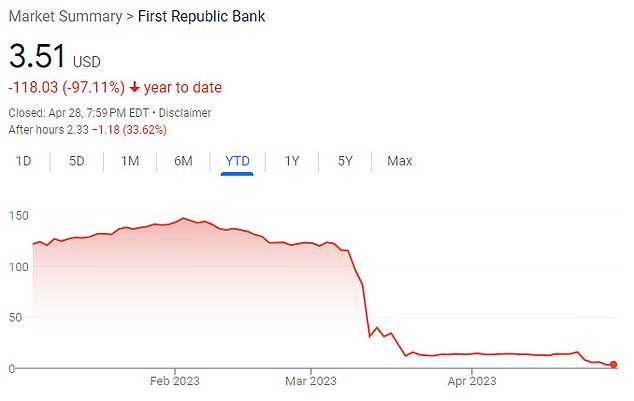

First Republic shares dropped 75 percent from Monday to Friday, after the bank disclosed it had lost $100 billion in deposits in the first quarter

The FDIC reached out to banks late on Thursday seeking indications of interest, including a proposed price and estimated cost to the agency’s deposit insurance fund, the Bloomberg report said.

The FDIC said in a statement: ‘We do not comment on or confirm reports about open and operating banks.’

Spokespersons for First Republic, JPMorgan Chase, and PNC declined to comment when reached by DailyMail.com on Saturday morning.

On Friday, a First Republic spokesperson had said: ‘We are engaged in discussions with multiple parties about our strategic options while continuing to serve our clients.’

For suitors, buying First Republic after it enters FDIC receivership is potentially more attractive than an open-market purchase for a number of reasons, including dramatic reductions in red tape and potential liabilities.

First Republic had some $233 billion in assets at the end of the first quarter, meaning that if it enters receivership, it would become the second-largest bank to fail in US history, eclipsing the collapse of Silicon Valley Bank on March 10.

The collapse of Silicon Valley Bank and, days later, Signature Bank of New York, triggered a run on deposits at First Republic, which is the US lender with the largest share of uninsured deposits above the FDIC’s limit of $250,000.

A $30 billion lifeline from a consortium of 11 major US banks, who injected the funds as deposits in First Republic on March 16, failed to shore up confidence in the lender.

Those deposits are uninsured, and it is unclear what will become of them if the FDIC places First Republic in receivership.

First Republic earlier this week said its deposits had slumped by more than $100 billion in the first quarter. The bank’s CEO Michael J. Roffler is seen above

For suitors, buying First Republic after it enters FDIC receivership is potentially more attractive than an open-market purchase for a number of reasons

Despite the lifeline, First Republic struggled to find support from larger banks or private equity firms on its proposed move to create a so-called ‘bad bank’ to spin off troubled assets.

On Monday, First Republic disclosed that it had lost roughly $100 billion in deposits during the first quarter, triggering a sharp sell-off in the company’s stock.

First Republic shares dropped 75 percent from Monday to Friday, and are now down more than 97 percent since the start of the year, when they traded at around $120.

At its lowest point Friday, the bank had a market capitalization of nearly $557 million, a far cry from its peak valuation of more than $40 billion in November 2021.

The shares, which lasted traded at $2.33 in extended hours on Friday, would be essentially worthless if the company is seized by the FDIC.

However, unlike the events surrounding the collapse of SVB and Signature last month, the concerns surrounding First Republic had little impact on broader markets or other bank stocks this week.

The Dow Jones Industrial Average gained on the week to finish its best month since January, as investors appeared to view First Republic’s troubles as isolated.

John Guarnera, senior corporate analyst at RBC Bluebay Asset Management, told Reuters the First Republic case is an ‘evolving situation.’

‘The rest of the regional bank system feels like it’s in a different place than where [First Republic] is,’ he said.

News of the imminent move to put First Republic in receivership followed reports from the Federal Reserve and FDIC detailed their supervisory lapses before deposit runs caused the collapse of Silicon Valley Bank and Signature Bank in March.

The Fed’s assessment of its inadequacies in identifying problems and pushing for fixes at California-based SVB came with promises for tougher supervision and stricter rules for banks.

Source: | This article originally belongs to Dailymail.co.uk