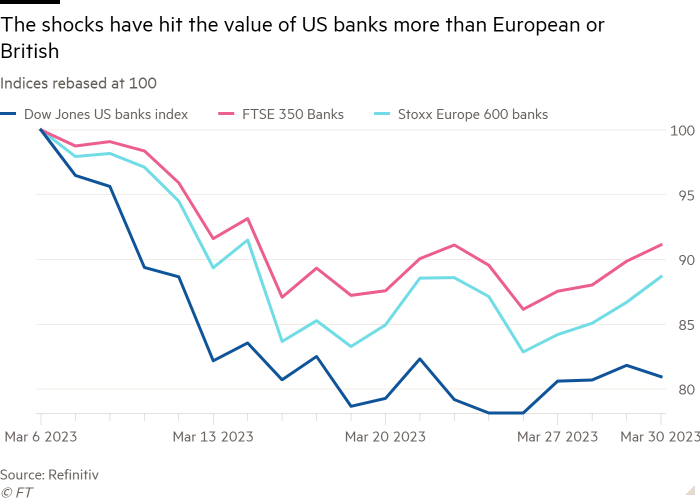

Banks are the Achilles heel of the market economy. The combination of risky long-term assets with liquid liabilities redeemable at par is a standing invitation to illiquidity and insolvency. Contagion is also a permanent danger. The events of recent weeks have reminded us of these realities.

So, what lessons should be learnt, including in the UK? As Andrew Bailey, governor of the Bank of England has reminded the House of Commons Treasury Committee, “Banking is an international industry and the UK is a significant financial centre.” The UK wants to enjoy the benefits, while minimising the risks. What is, at least so far, a “mini” crisis is a reminder of the risks.

So, what are the obvious lessons?

First, an open financial entrepot like the UK is vulnerable to regulatory failures elsewhere. Thus, as Bailey stressed, it was helpful that Silicon Valley Bank UK was a ringfenced subsidiary, not a branch. That allowed the UK to resolve it quickly and independently.

Second, the story of Credit Suisse shows that policymakers may find it hard to impose orderly resolution on politically sensitive institutions, even when a plan for it exists. The UK authorities need to consider whether and how they would have done better in a similar case. Ringfencing of the domestic retail bank did not avoid the problem in that case. That is disturbing.

Third, if resolution is so hard, it is even more important for banks to have so much credibly loss-bearing equity and debt and such strong liquidity that all depositors will feel safe. Otherwise, there are likely to be runs and bailouts.

Fourth, large holes in the regulatory net must be avoided. Losses on the market value of portfolios caused by higher interest rates are a potentially relevant example. The British authorities appear to have been much more aware of the risks created by such losses than those in the US. Such losses must be taken into account in both capital and liquidity requirements and stress tests.

Fifth, bailouts are always systemically significant. If depositors believe they will be protected, banks will be encouraged to behave in a more irresponsible manner. So, any bank whose losses might be bailed out must be regulated as systemic. Again, this risk can be reduced with higher equity capital and “bailinable” debt and stronger liquidity. Equity and long-term debt should also be written down before deposits. Alternatively, there could be more generous formal insurance of deposits, with premiums related to a bank’s riskiness.

Sixth, the story of SVB shows the importance of responsible management. These are not just profitmaking businesses, but also utilities supported in a number of ways by taxpayers. In this case, senior management took tens of millions of dollars out of the bank while it was being driven into the ground. Thereupon, depositors were rescued by taxpayers. This just has to be prevented. As Charles Goodhart of the London School of Economics has noted, managers who fail to manage successfully must share — and know they will share — in the losses. They should bear personal financial liability. That change might permit liberalisation, even abolition, of the UK’s onerous “senior managers” regime.

Seventh, think carefully about opening holes in the regulatory regime in an emergency. The ringfencing recommended by the Independent Commission on Banking (of which I was a member) was an attempt to separate domestic retail banking from the risks created by the relatively large global activities of certain UK banks. That is a far smaller concern for the US, where domestic activities are so large. Ringfencing was also designed to give regulators and the government more options in the case of resolution. By granting HSBC an exemption from ringfencing in its takeover of SVB UK, the government has opened a potentially dangerous loophole. This needs to be closed as soon as possible.

Finally, the best protection against occasional huge banking crises is frequent smaller ones. Fear works. We have seen, for example, some unwise deregulation. That of smaller banks in the US in 2019, which contributed to the recent crisis, is a powerful example. Pressure for deregulation has also been growing in the UK. A shock like this should make mindless deregulation less appealing to politicians and mindless risk-taking less appealing to bankers. Both lessons might have been learnt in the US and elsewhere, for a while.

The regulatory regime and bank supervision in the UK seem to have been quite effective. UK bankers also seem to have been quite sensible. So, we did learn from the last crisis. That is good. The best result of the present shock is that it should reinforce those lessons.

Follow Martin Wolf with myFT and on Twitter