This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Chip stocks are having a moment in the sun. The Philly semiconductor index is up 27 per cent year to date and even laggards are enjoying a bump. Intel stock is up almost 30 per cent in March after some encouraging news on its process tech. Got a good-news equity story you’re watching? Email us: [email protected] and [email protected].

Markets after SVB

Unhedged has spent the past few weeks hitting the Silicon Valley Bank story from all angles, and neglected the broader market as a result. So, with the SVB failure slipping (we hope!) into the rear-view mirror, where are markets?

There has been, to start, a sea change in interest rates. In the face of the banking stress, futures markets gave up their faith in higher-for-longer rates in favour of pricing in Fed rate cuts. The market-implied fed funds rate for December peaked at 5.5 per cent near the start of March. Now it’s down to 4.3 per cent. Bond yields have followed. The two-year yield has repriced down almost 100bp, and the 10-year nearly 50bp, since early March.

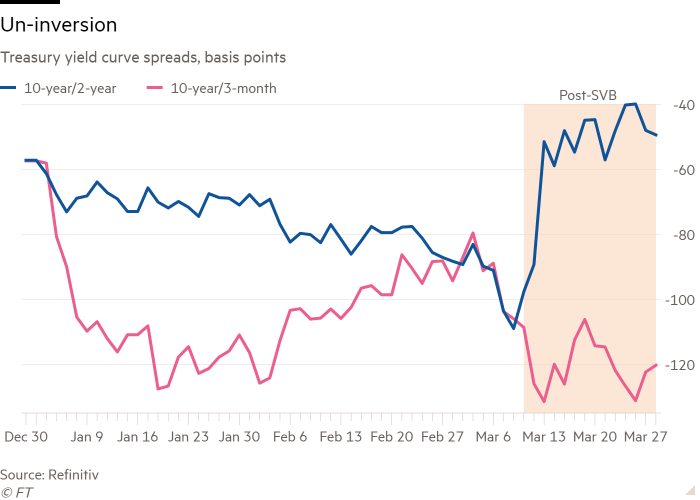

The move in the two-year has had a curious effect on the shape of the yield curve. It remains deeply inverted just about everywhere, signalling recession. But the 10-year/two-year spread (the second-best recession indicator) is now much less inverted, while the 10-year/three-month spread (the best one) has stayed put:

There is a clear rationale here: Sean Darby and Kenneth Chan of Jefferies call it a “classic end-of-cycle story”. After a banking crisis and credit crunch, the bond market is bracing for an imminent halt to the tightening cycle as (in all likelihood) a recession or sharp slowdown arrives. The Fed seems to feel the same way. From Bloomberg on Tuesday:

Federal Reserve Chair Jerome Powell, asked in a private meeting with US lawmakers Wednesday how much further the central bank will raise interest rates this year, referred to policymakers’ latest forecasts showing they anticipate one more increase, according to Republican Representative Kevin Hern.

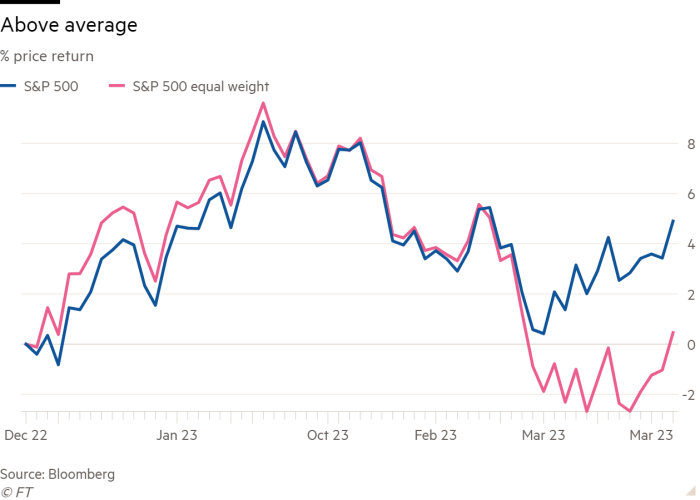

If the change in rates is legible, the sanguine behaviour of risk assets is a puzzle. Despite some widening in corporate credit spreads, they still look much too tight, as we argued earlier this week. For its part, the S&P 500 simply shrugged off the whole SVB imbroglio. Even as bond market volatility has remained high, stock vol has returned to normal:

Within the S&P, the pre-SVB story — outperformance by growth in 2023, after they trailed value in 2022 — looks intact. The Russell 2000 growth index continues to outperform Russell 2000 value this month. In terms of sector performance, there have been a few changes since SVB blew up. Financials have been crushed recently for obvious reasons. Consumer staples are doing better (up 2.6 per cent post-SVB vs minus 3.6 per cent pre-SVB), and consumer discretionary worse (10.6 per cent post vs 1.4 per cent pre). With higher recession risk now, that makes sense. But the biggest two sectoral winners, communication services and technology, were the same in both periods.

The strength in tech — benefiting, as it does, some very large-cap companies such as Apple and Microsoft — slightly obscures softness in the performance of the average S&P 500 stock.

Still, it is odd stocks haven’t sold off more, when bonds are telling us recession is growing closer. What’s going on?

One possibility could be that lower yields simply cancelled out higher recession risk. In principle, a lower risk-free rate makes stocks, especially long-duration growth stocks, look more attractive. But (as Unhedged repeats until it is blue in the face) this is not a law of nature. It matters why rates are falling. If rates are falling because the economy is swirling down the drain, for example, the lower discount is offset by lower cash flows. If investors reflexively respond to lower rates with higher stock prices, they are stuck in the old, pre-inflation, easy-money regime that is likely over for good.

Japan goes capitalist?

Something big may be happening in Japan. Investors have hoped for a pivot towards shareholder value in the country for a long time — and been repeatedly disappointed. Yet some feel the winds shifting.

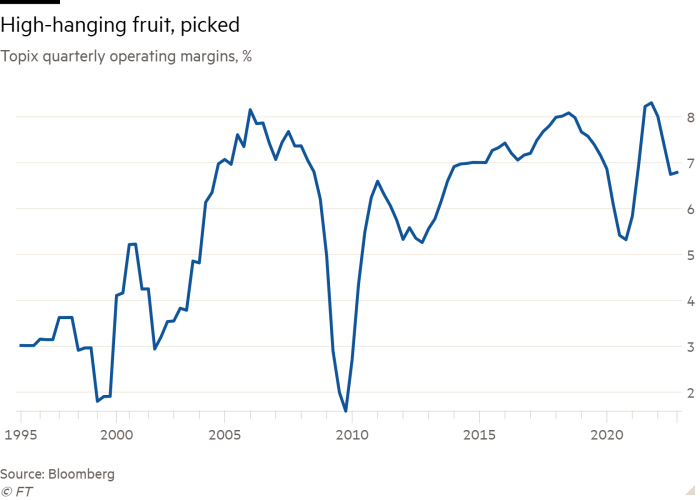

Japanese markets are treacherous places to invest. The 1990s bust created an environment of corporate risk aversion — the hallmarks of which were cross-company shareholding, huge cash hoards and empire building. Weak profits and bloated balance sheets pushed many companies’ price/book ratios below one, meaning the businesses are in principle worth more carved up and sold. However you measure it, something like half of Japan Inc trades under 1 p/b.

From a US shareholder value perspective, Japanese companies are in the peculiar position of having done the hard stuff, such as raising underlying profitability, but struggling with the easy stuff, like returning those profits to shareholders. Look how much operating margins have climbed since the 1990s:

But Japanese companies have mostly just sat on their mountains of cash, rarely raising pay or buying back shares. The average Topix company has a staggeringly high 50 per cent equity-to-assets ratio, according to JPMorgan. As Matt Klein put it in Unhedged last year, “In theory, there is enormous potential for Japanese companies to boost shareholder returns by rejiggering their balance sheets.”

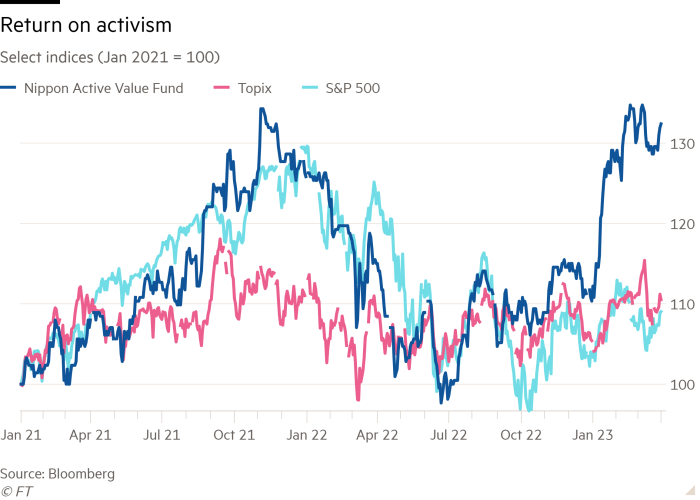

This has for decades lured in activist investors, drooling over the seemingly easy value on offer. The latest wave began building before the coronavirus pandemic, but in recent months has accelerated. A few activists have won important victories, getting management to return cash to shareholders, sell crossholdings and shed non-core assets. Private equity investors such as KKR and Japan Industrial Partners are circling. The investor relations business is booming. The Nippon Active Value Fund, which tracks small and mid-cap activist takeover targets, is up 18 per cent year to date:

Though far from the only one, perhaps the most significant recent example is Dai Nippon Printing, a Japanese conglomerate worth, until recently, ¥900bn. Earlier this month Dai Nippon, under pressure from Elliott Management, announced a mammoth buyback programme, worth ¥300bn ($2.2bn), and pledged to generate billions in cash from trimming crossholdings. The company, now worth ¥1.1tn, is caving to Elliott’s demand to increase return on equity to 10 per cent, modest by international standards but above MSCI Japan’s average ROE. The resulting stock price surge lifted the company’s p/b sharply (with the caveat that measuring p/b is more art than science):

Change is coming from on high, too. In January, the Tokyo Stock Exchange, which has deep ties to Japan’s ministry of finance, revised plans for its “prime” listing tier, the exchange’s new top echelon (investors have long complained that the old top tier contained too many junky minnow companies). With prime, TSE hopes to trim the fat, even if modestly. In time index products should follow, giving prime companies better access to capital. The catch: any firm wishing to stay in the prime tier will need to keep its p/b ratio above 1, or else publish a plan describing how they’ll get there.

The new rules are vague and full of wriggle room, designed more to encourage capital discipline than force it. But they are part of a wider TSE push to get companies to embrace activists. Drew Edwards, a veteran Japan portfolio manager who runs GMO’s Usonian equity funds, sees a broader shift in Japanese society under way:

In the US, compensation drives motivation. In Japan, [management] wants to be esteemed ..

What that “right thing” is is changing now. It used to be do right by your employees, customers and bank. Now, it’s increasingly shifting towards [focusing on] shareholders . . .

There is now this interesting alignment between shareholders and policymakers. [Japan’s national pension plan] needs to get better returns on its national assets, because [Japanese government bonds], where they historically parked all the pension assets, are generating negative returns. They’ve got to get it from earnings and [better] ROE.

Dai Nippon’s bumper buybacks, says Edwards, reflect a “confluence” of forces: changing notions of what companies should do, the TSE’s new guidelines, pressure from Elliott, companies without activists announcing buybacks of their own volition and companies with activists getting embarrassed by them.

Anyone who has watched Japan for long will have heard this story before; scepticism is warranted. While the surge of activist interest is notable, it could lose steam. Corporate Japan may start circling the wagons, as it has before. As the FT’s Leo Lewis and Kana Inagaki reported this month:

Investors will warn the Japanese government this week that a planned revision to rules on anti-takeover defence risks giving companies stealth protections against hostile domestic bids, foreign buyers and shareholder activists . . .

Masatoshi Kikuchi, chief equity strategist at Mizuho Securities, said that . . . there had been an increase in companies introducing target-specific anti-takeover schemes in response to attacks by activist investors.

It’s too much to expect Japan to embrace shareholder capitalism overnight. But alongside a potential breakthrough in wage-price dynamics, it reinforces Japan’s position as, we think, the most interesting equity market in the world. In the near term, the low-hanging fruit is probably abundant enough to keep global investors tempted. Some might even make money this time. (Ethan Wu)

One good read

Whatever you think of Nassim Taleb, he sure is funny: “What people don’t realise is I have my Twitter fights prepared at least a week in advance. And I use that downtime, traffic jam in an Uber or something like that, to start executing.”

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

The Lex Newsletter — Lex is the FT’s incisive daily column on investment. Sign up for our newsletter on local and global trends from expert writers in four great financial centres. Sign up here