Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

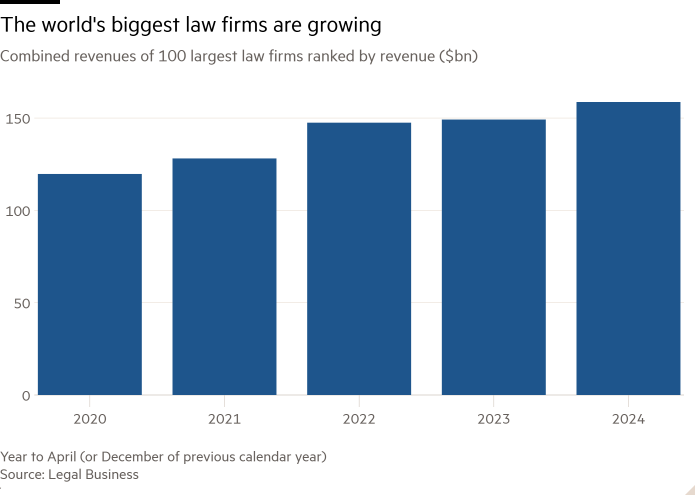

Big law is getting bigger. In May, the UK’s Allen & Overy and New York’s Shearman & Sterling cemented one of the biggest-ever transatlantic legal mergers. This week, the UK’s Herbert Smith Freehills announced plans to form a top-20 global law firm by headcount by combining with the smaller US-based firm Kramer Levin. Interest in such tie-ups is at an all-time high on both sides of the Atlantic, says Kent Zimmerman of consultancy Zeughauser Group.

For a UK firm, the appeal of an American alliance is obvious. Leading US firms generate at least twice the profits per equity partner of most of their UK counterparts — and the gap is growing. Ambitious British firms all want a bigger slice of the lucrative US market. Building from scratch has proved extremely hard.

By contrast, some US firms such as Latham & Watkins and Kirkland & Ellis have successfully built up big operations in London. A cross-border merger is more appealing to smaller US firms, seeking a higher profile and cross-selling opportunities while preserving more autonomy than in a domestic merger. Shearman, a top-tier brand which had hit trouble, was an exception.

The discrepancy in profitability between the US and UK market presents big challenges. If the two firms are similarly profitable, it is relatively easy to come up with a common pay structure. But the firms are still likely to have very different character and clientele.

If profitability differs markedly, the two firms can opt to retain much of their autonomy by adopting a partnership model known as a Swiss verein, which keeps their finances separate. However, this can mean there is little incentive for partners to refer work to overseas colleagues, as it will not contribute to their profit pool.

That problem is overcome if the merger creates a single profit pool. But that can end up diluting the earnings of the US partners and forcing the UK firm to improve profitability by cutting jobs and demoting some equity partners.

Profits per equity partner are two-fifths higher at Kramer Levin than at Herbert Smith Freehill. But the firms insist they will avoid such “de-equitisation” while devising an integrated profit pool that retains their US competitiveness. That will be tough. If it fails, they can expect disgruntled partners to vote with their feet.

The lopsided nature of the deal may help. The ratio of UK to US revenues of the latest tie-up is over three to one; the A&O Shearman deal was similar. Unequal mergers that are really takeovers are less likely to be stymied by politics.

Size matters if these transatlatantic combinations have a hope of managing the cultural clashes, conflicts of interest and differences in profitability to create a successful combination. Either consolidation in this market will stop short of creating the dominant global brands seen in the accountancy profession. Or there will be plenty of “mergers” that prove an unhappy union indeed.