In a 30-plus-year career in corporate restructuring, consultant Andreas Rüter has seen it all: the dotcom bust, September 11, the global financial meltdown, the euro crisis, Covid-19. But what’s happening right now in corporate Germany is “unprecedented” and “of a completely different order of magnitude”, says Rüter, the country head of AlixPartners.

The federal republic’s all-important automotive sector, chemical industry and engineering sector are all in a slump at the same time. Rüter’s firm is so overwhelmed by demand for restructuring that it’s turning potential clients away.

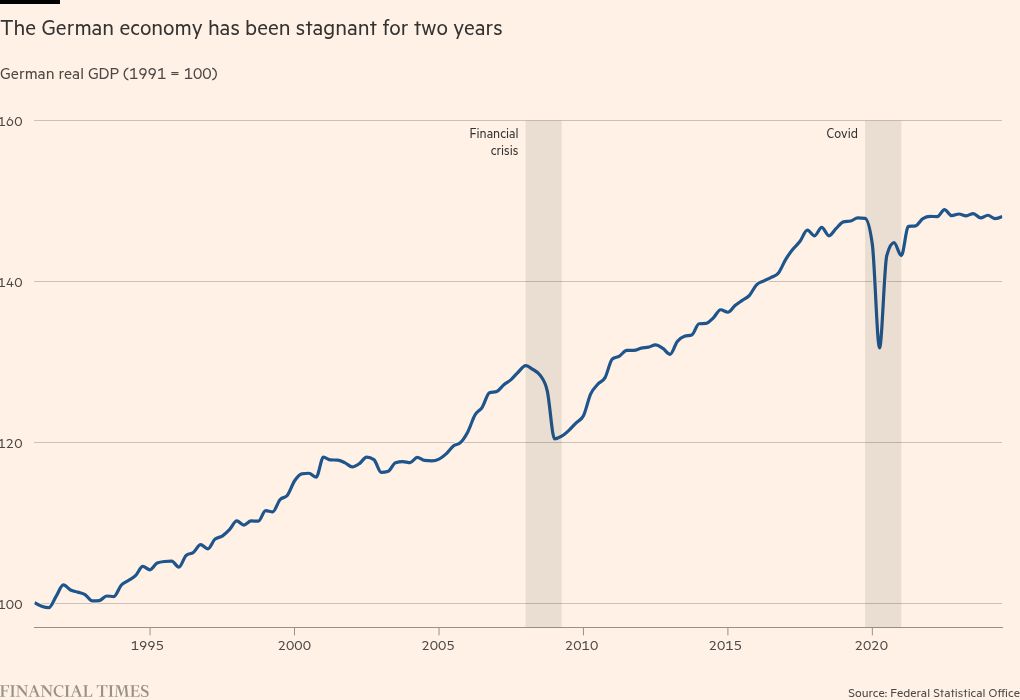

Over the past three years, Europe’s largest economy has slowly but steadily sunk into crisis. The country has seen no meaningful quarterly real GDP growth since late 2021, and annual GDP is poised to shrink for the second year in a row. Industrial production, excluding construction, peaked in 2017 and is down 16 per cent since then. According to the latest available data, corporate investment declined in 12 of the past 20 quarters and is now at a level last seen during the early shock of the pandemic. Foreign direct investment is also down sharply.

Light on the horizon is hard to detect. In its latest forecast, the IMF says that German GDP will expand by just 0.8 per cent next year. Of the world’s largest and richest economies, only Italy is expected to grow as slowly.

In manufacturing, where Germany is Europe’s traditional powerhouse, things look especially bleak. Volkswagen has warned of plant closures on home turf for the first time in its history. The 212-year-old Thyssenkrupp, once a symbol of German industrial might, is bogged down in a boardroom battle over the future of its steel unit, with thousands of jobs at risk. The tyremaker Continental is seeking to spin off its struggling €20bn automotive business. In September, the 225-year-old family-owned shipyard Meyer Werft narrowly avoided bankruptcy with a €400mn government bailout.

Robin Winkler, Deutsche Bank’s Germany chief economist, labels the fall in industrial production “the most pronounced downturn” in Germany’s postwar history. He is far from alone. “Germany’s business model is in grave danger — not some time in the future, but here and now,” Siegfried Russwurm, the president of the Federation of German Industries (BDI), warned in September. A fifth of Germany’s remaining industrial production could disappear by 2030, he said. “Deindustrialisation is a real risk.”

These dire predictions come at a time of rising political instability. Relations between the parties in Chancellor Olaf Scholz’s fragile coalition — social democrats, greens and liberals — are at rock bottom, with their policy differences now so deep that many expect that the alliance could collapse in a matter of weeks, ushering in snap elections.

As the political centre has weakened, populist parties such as the far-right Alternative for Germany and the hard-left Sahra Wagenknecht Alliance (BSW) have surged, their fiery rhetoric raising fears for the future of a finely balanced political system based on consensus and compromise.

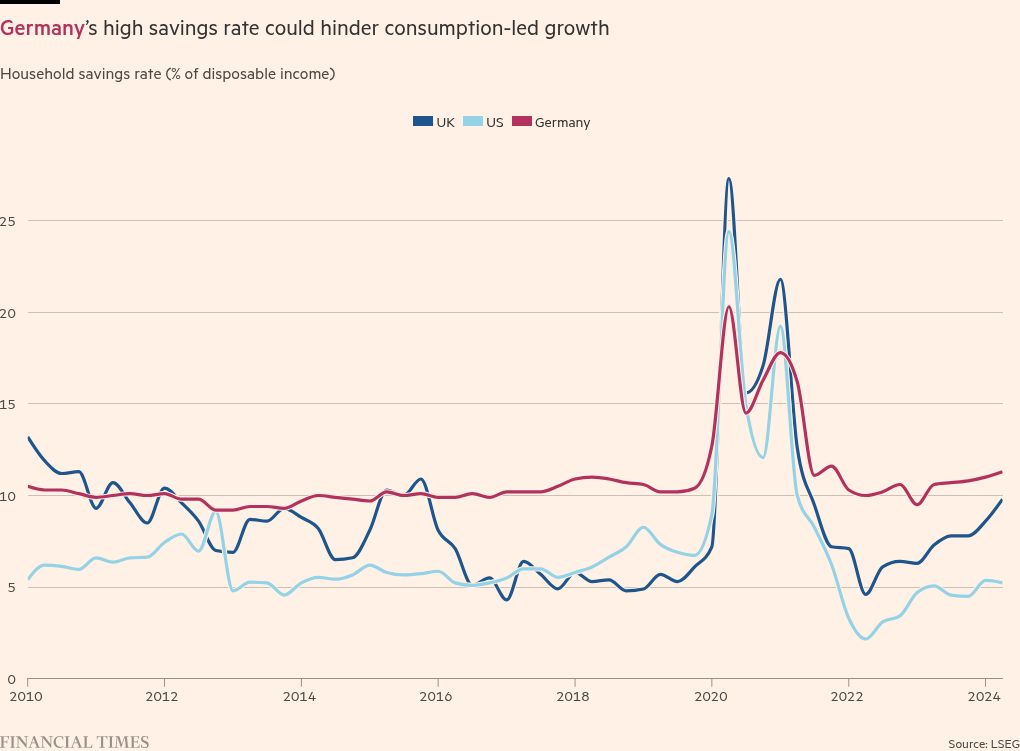

Economists and business leaders blame Germany’s economic woes on high energy costs, high corporate taxes and high labour costs, as well as what they describe as excessive bureaucracy. These issues have been compounded by a shortage of skilled workers and the dire state of the country’s infrastructure after decades of under-investment. Meanwhile, according to the country’s statistical agency, nervous German consumers are now saving 11.1 per cent of their income, twice as much as their US peers — thus slowing down the economy even further.

Not everyone is gloomy. “Germany is not in decline,” Bundesbank president Joachim Nagel insisted in a speech in late September, pointing to the strong labour market — the number of unemployed workers, at 2.8mn, is at the lowest level in a decade — and the strong balance sheets of German companies. “Germany as a business location is better than its current reputation,” Nagel added.

Still, the German Council of Economic Experts warns that the country is facing a new normal of low growth and poor economic performance. It estimates that the potential growth rate — the pace at which the economy can expand without overheating — is now just 0.4 per cent, down from an already low 1.4 per cent, because of labour shortages and poor productivity growth.

After years of condescending lectures from Berlin on reform and fiscal discipline, the rest of Europe might be forgiven for feeling a touch of schadenfreude. But if the EU’s biggest net contributor is in crisis, the entire bloc suffers. Nearly two-thirds of all Germany’s imports come from fellow EU states, and the federal republic accounts for a quarter of EU GDP. Combined with France’s political and economic woes, this risks destabilising the wider EU.

“For 15 years, the German economy was like a ship sailing with a strong tailwind,” says Clemens Fuest, president of the Munich-based economic think-tank Ifo, pointing to strong employment growth, budgetary surpluses and fat industry profits enabled by labour market reforms, low interest rates, cheap Russian gas and buoyant world trade. “Now it is facing a very stiff headwind.”

On a late October day, steam rises over a chemical plant by the river Rhine in Krefeld, north-western Germany, and the egg-like smell of sulphur hangs in the air. Chemicals have been produced at this site since 1877.

Inside the facility, manager Michael Vössing explains how his workforce of 280 people dissolves black titanium ore in boiling sulphuric acid to make titanium dioxide, used to whiten everything from paints, plastics and pills to textiles and toothpaste.

“Chemically, it’s a very simple process,” says Vössing, who has worked here for more than 20 years. In that time, he has watched China become the world’s biggest exporter of the chemical. Gesturing at the plant, now owned by the British chemical group Venator, he adds: “You only need money to build this.”

But cash has become a serious constraint. In May, Venator shut down its only other German site producing titanium dioxide, in nearby Duisburg, and some 350 staff lost their jobs. The site had become financially unviable, says Venator’s chief operating officer, Mahomed Maiter.

Reliant on imported hydrocarbons, the chemical industry — one of Germany’s largest manufacturing sectors — has been badly damaged by the increase in energy prices that followed Russia’s invasion of Ukraine. While gas prices appear to have peaked, this summer they were still three times as expensive as before the war. Chemical production in Germany is 18 per cent below its level in 2018.

As the post-pandemic recovery of European industry still lags behind, demand for titanium dioxide has remained weak, and a glut of imports of the pigment from China brought things to a head. This summer, the EU introduced anti-dumping duties on Chinese imports. But, says Maiter, “it’s a little late.”

FT Edit

This article was featured in FT Edit, a daily selection of eight stories to inform, inspire and delight, free to read for 30 days. Explore FT Edit here ➼

An upended relationship with China is at the root of some of Germany’s current woes. The Asian giant’s transformation from lucrative import market to producer and exporter in its own right is stretching some of the mainstays of the German economy beyond breaking point. While China gobbled up 8 per cent of all German exports in 2020, this year the figure is likely to be 5 per cent. “Instead of importing German capital goods, Chinese manufacturers have turned into competitors,” says DWS economist Elke Speidel-Walz.

Those changes are perhaps most visible in Germany’s high-profile automotive industry, particularly among the country’s three big carmakers, VW, Mercedes-Benz and BMW. For most of the past two decades, the Chinese hunger for German gas-guzzling sedans and SUVs seemed insatiable, and margins were far higher than at home.

Easy profits lured German carmakers into doing “more of the same” for years, says Eberhard Weiblen, boss of Porsche Consulting, an advisory firm owned by the eponymous carmaker. But this strategy is now backfiring badly. Homegrown, electric-only marques such as BYD, Nio and Xpeng have wooed Chinese drivers with technologically sophisticated vehicles that, underpinned by subsidies, also sell at far lower prices.

The Germans stand a better chance at defending market share in Europe, analysts say, thanks to strong branding, solid balance sheets and vast investment budgets — not to mention the EU’s recent decision to impose tariffs of up to 45 per cent on Chinese EVs.

But the numbers tell their own story. According to the VDA, Germany’s automotive industry association, vehicle production in Germany peaked in 2016 at 5.7mn cars; last year the number was 4.1mn, down by more than a quarter. Since 2018, 64,000 jobs have been lost in the industry — nearly 8 per cent of the country’s automotive workforce — and tens of thousands more are at risk. Weak demand for EVs also means that from next year many brands may have to pay heavy fines for missing the EU’s ever-tougher CO₂ targets.

“The future of German carmakers will be decided within the next two to three years,” warns Weiblen.

While things are undeniably tough for the major marques, suppliers — who employ a third of all German car workers — face even bigger woes. EVs need far fewer parts than vehicles with combustion engines, with obvious knock-on effects for specialist engineering firms.

“[Germany’s] traditional strengths in transmission and combustion technologies are being replaced,” says Holger Klein, chief executive of its second-largest automotive supplier, ZF Friedrichshafen. Founded in 1915 — originally named Zahnradfabrik Friedrichshafen after its hometown and the German word for “cog factory”, its first product — ZF generated €46.6bn in revenue in 2023.

In an effort to adapt, ZF has spent billions snapping up future-proof technologies, including a $7bn, debt-fuelled deal in 2020 to buy US brake system specialist Wabco. Despite ramped up R&D spending, which helped double the production of electric motors in 18 months, it has still lowered its outlook for 2024 twice. The firm is now bracing itself for a 12 per cent decline in sales and a 40 per cent plunge in operating profit. By 2028, the group is planning to axe as many as 14,000 jobs in Germany — up to a quarter of its home workforce.

“[It is the] most challenging period the European automotive industry has ever faced,” Klein says.

German economists and business leaders have long been aware of the crisis. But for months, Chancellor Scholz appeared to deny there was a problem. Indeed, in March 2023 he promised a second economic miracle, thanks to hundreds of billions of euros of investments in green technology. “Germany will for a time be able to achieve growth rates last seen in the 1950s and 60s,” he asserted.

In early 2024, the chancellor dismissed dire warnings from business associations about industrial decline by citing an old German adage that merchants always moan. For months, he and his ministers had clung to the hope that the economy would start to recover in the second half of this year. Some even banked on Germany’s men’s football team winning the Euro 2024 tournament, hoping for a vibe shift.

In the end, the team were knocked out in the quarterfinals and the economic data kept getting darker. Last month, ministers admitted the country was facing its first two-year recession since the early 2000s. Meanwhile, Scholz’s quarrelsome coalition seems ever more paralysed by fundamental disagreements about Germany’s constitutional “debt brake”, how much public debt the government is permitted to raise.

In a caustic speech that went viral over the summer, Deutsche Börse chief executive Theodor Weimer articulated the growing despair felt by many among Germany’s business elite, saying that their nation was at risk of becoming a “developing country”. He also claimed the government was viewed as “stupid” by international investors and was turning the country into a “junk shop”.

As the economic clouds have gathered, Scholz’s rhetoric has started to shift. In July, his cabinet adopted a set of reforms designed to stimulate growth, including incentives for companies to invest and for workers to re-enter the labour market, as well as energy subsidies for some industrial companies — though most of these measures have yet to be enacted.

Scholz has also promised a “new industrial agenda”, last month summoning business leaders and union bosses to a summit to discuss safeguarding industrial jobs. Yet, in a sign of how fractious the coalition he leads has become, he didn’t invite his own economy minister Robert Habeck of the Green party, nor his own finance minister, the FDP leader Christian Lindner, who held his own rival roundtable on the same day instead.

Business leaders are sceptical that the current administration is capable of changing things for the better, citing uncertainty caused by coalition strife and constantly changing policies. “Companies currently cannot rely on the German government to sort out the problems’ root causes,” says Rüter of AlixPartners.

This has provided an opening for Friedrich Merz, leader of the opposition Christian Democrats (CDU) — the man many in Germany expect will be the country’s next chancellor. The CDU has established a strong lead in the polls, even though large numbers of voters hold the party and its former leader, Angela Merkel, accountable for many of Germany’s current ills.

Merz, however, has sought to pin the blame directly on Scholz: “After three years, 300,000 industrial jobs have been lost,” he said in a recent speech. “That is not the legacy of former governments . . . that’s the result of your economic policy of the past three years.”

The conservative party leader has promised to put in place an “Agenda 2030” to reduce the burden of red tape, which he describes as a “key obstacle to growth”; to cut taxes on companies; and halve electricity network charges for industrial customers, and so improve Germany’s competitiveness. His model is the “Agenda 2010” that Chancellor Gerhard Schröder pushed through in 2003 when Germany, haunted by record postwar unemployment, was seen as the sick man of Europe.

Some share Merz’s optimism that, with the right policies, Germany can indeed turn itself round. Holger Schmieding, chief economist at Berenberg Bank, argues that the country is still in a much better position than it was in the early 2000s, because of a strong labour market and sound public finances.

Schmieding also points to the mid-1990s, when Germany was struggling with the cost of reunification, growing long-term unemployment and a loss of international competitiveness. “The awareness that there is a problem is higher today than back then,” he suggests, adding that, whoever wins federal elections scheduled for 2025, “the next government can and will put things on the right track.”

Optimists also emphasise Germany’s strengths in new sectors, particularly those related to the green transition. “Germany is well-placed to build up new value creation in climate technologies, industrial automation and health,” says Michael Brigl, managing partner at Boston Consulting Group, adding that these can generate “economic growth . . . in the foreseeable future.”

Habeck has also sought to project confidence. Presenting the government’s downgraded forecasts last month, he emphasised that, despite everything, Germany was “full of strengths”. It was the third-largest economy in the world, had innovative companies “that think in generations”, unparalleled research institutions and a highly trained workforce.

Yes, he acknowledged, the environment was “unsatisfactory”. “But we are in the process of working our way out of this, as we have done so often in our history,” he said. “We will break free.”

Data visualisation by Keith Fray