Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

A Goldman Sachs banker at a recent investor event repeated a well-worn joke about private equity executives investing their final-ever funds: the punchline was that the PE executives just did not know that their demise had arrived.

Hedge funds typically allow their backers to redeem their capital almost immediately. As such, a bad year, or quarter or even a single trade can lead to the fund immediately going out of business. The judgment is harsh but it remains the law of that jungle.

Private equity drawdown vehicles, in contrast, have seven to 10-year lives. Deals struck in a zero interest rate environment suddenly look catastrophic. But the consequences for buyout gurus will play out over several years as they struggle to raise successor funds, unable to persuade limited partners to pony up again. Less money raised will lead to lower fee income and ultimately fewer jobs. Some funds may just decide to throw in the towel and wind down.

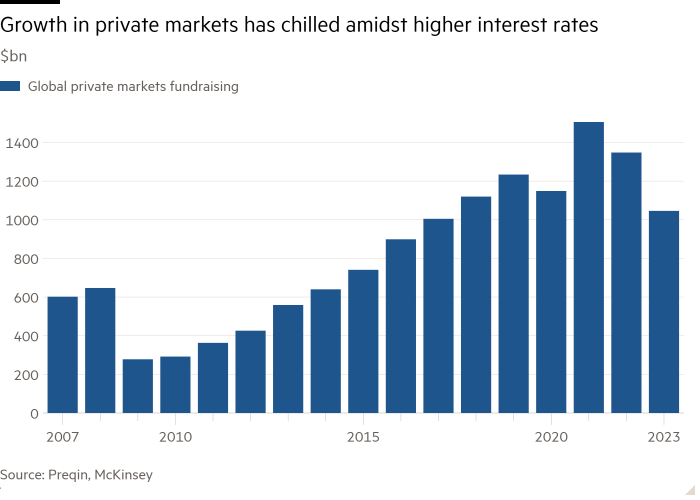

Even before the dislocation of 2022 and 2023, the big pension and sovereign wealth funds were choosing to work with fewer money managers and giving the select group more of their money to invest across multiple private capital strategies.

There are at least 18,000 private funds in the United States, most investing in middle and lower middle market companies. That figure grew by more than 50 per cent in the previous five years, according to data compiled by the Securities and Exchange Commission. Institutional investors were told that they must allocate more to private equity so existing and challenger firms easily raised capital.

But even stalwart funds such as Carlyle and Apollo have missed their mark in raising recent buyout funds. Capital pools had ended up over-allocated to private equity with the drop in public market valuations and suddenly new areas such as infrastructure, private credit and real estate were competing with corporate funds.

In the same way that actively managed mutual funds almost never consistently beat the market, there is a question over how a particular private equity fund could consistently earn 20 per cent returns over multiple decades.

The firms themselves would say that they have proprietary sourcing, due diligence, or operational chops. But in the crowded middle market, plenty of firms look remarkably the same. A long fund life may be a job preserver for some period. But on the other side, the bar to get allocators to write new cheques and lock up their capital will understandably be very high indeed.