Europe’s last major cross-border bank merger, cooked up in 2007 by the continent’s banking elite during clandestine meetings in Geneva’s grand Four Seasons Hotel des Bergues, did not end well.

But 17 years after Dutch lender ABN Amro was carved up in a three-way transaction that contributed directly to four multibillion-euro bailouts during the financial crisis, European bank executives are contemplating mergers once again.

Andrea Orcel, who as a senior investment banker at Merrill Lynch was a key architect of the takeover of ABN Amro by Royal Bank of Scotland, Santander and Fortis, is in the vanguard. UniCredit, the Italian bank of which he is now chief executive, has shaken up the top echelon of European finance by taking a substantial stake in Commerzbank, Germany’s second-biggest lender.

After acquiring a chunk of shares from the German government, which bailed out Commerzbank during the financial crisis, and building up an under-the-radar position using derivatives, UniCredit shocked the country’s political and business establishment last month by revealing a 9 per cent stake.

If it receives permission from the European Central Bank, which should be a formality, UniCredit will be able to convert all its derivative positions into shares — giving it a 21 per cent stake and making it the lender’s largest shareholder.

A full merger between the two is not the only potential outcome of UniCredit’s overtures but even so, the swoop is the latest and most eye-catching sign that dealmaking among Europe’s banks is back on the cards.

Profitability at many of the continent’s lenders has improved markedly thanks to rising interest rates. Combined with their cleaner balance sheets and more robust capital levels, that has meant they are in a healthier position to acquire rivals.

Nicolai Tangen, chief executive of Norway’s $1.7tn oil fund, which owns shares in most of Europe’s biggest banks, says the continent needs more financial institutions with global heft.

“It’s very healthy to get bigger banks in fewer hands because scale matters in this industry,” he says. “There is just so much cost in having the whole regulatory system in place for a bank, and there is little evidence that larger banks give worse deals for consumers.”

There is also widespread agreement among Europe’s policymakers and politicians on the need to encourage larger, multinational banks as a way to fend off competition from US lenders, which have dominated global banking since the financial crisis, and fast-growing Asian rivals.

“Governments that nationalised banks during the financial crisis are now ready to draw a line under it and are selling their stakes,” says Marco Troiano, a banks analyst at Scope Ratings. “This means all those banks have come into play for potential consolidation.”

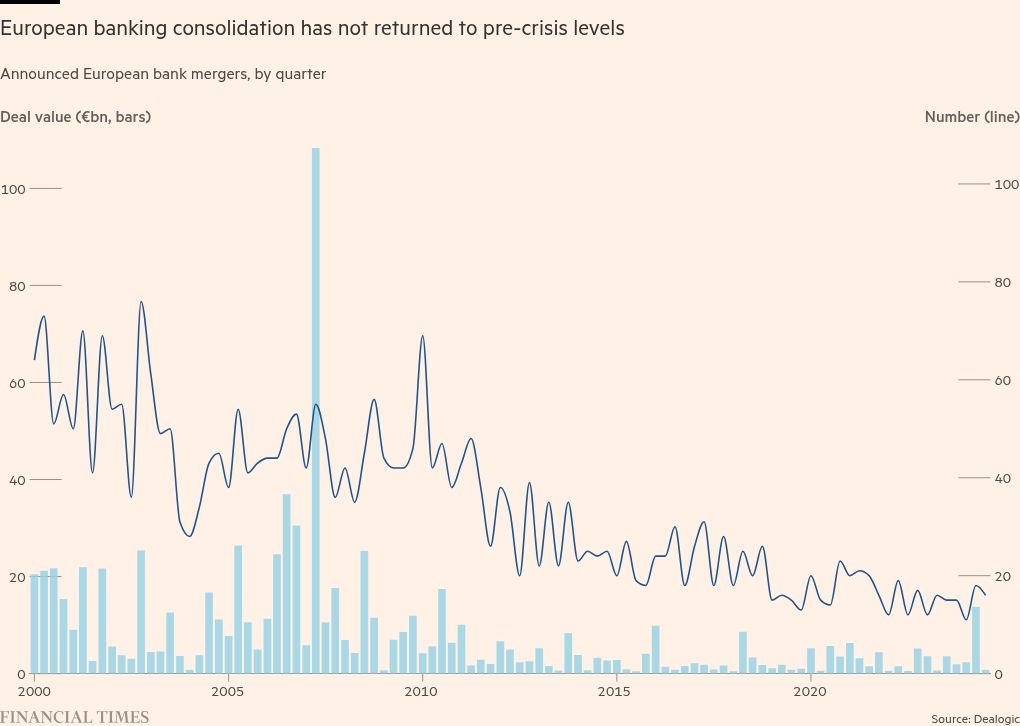

The value of mergers announced between European banks hit €13.8bn in the second quarter of this year, the highest figure since the third quarter of 2010, according to data compiled by Dealogic.

Notable deals over the past 18 months include the state-orchestrated rescue of Credit Suisse by UBS and the hostile pursuit of Sabadell by larger Spanish rival BBVA, a deal that if consummated would create Europe’s seventh-largest bank with a market value of €63bn.

Many of these transactions have been attempts at domestic consolidation, but there is enthusiasm in some quarters that they could herald a broader wave of cross-border dealmaking.

FT Edit

This article was featured in FT Edit, a daily selection of eight stories, handpicked by editors to inform, inspire and delight. Explore FT Edit here ➼

But cross-border bank mergers remain difficult to execute in practice because of national political opposition and the fragmented nature of Europe’s banking market.

The quarterly average number of deals since 2008 has been 27, with an average total value of just €4.2bn, according to Dealogic data — far below the 50 deals worth €16.4bn averaged in each quarter between 2000 and 2008.

And at present share prices, even a UniCredit-Commerzbank tie-up would be worth less than the €108bn of mergers in the second quarter of 2007, when the ABN Amro takeover was announced.

The global financial crisis of 2008-2010 marked the start of a long winter in European bank M&A.

“If you go back to the pre-financial crisis, banks were in an M&A growth mindset, fuelled by cheap money and a lack of appreciation for the risks involved,” says Justin Bisseker, banks analyst at fund manager Schroders, who has covered the sector for 27 years.

“Now everything is more regulated. There is a realisation that banks are international in life but national in death. That mindset has made cross-border deals much harder to execute.”

Lorenzo Bini Smaghi, chair of France’s Société Générale and a former executive board member of the ECB, agrees that national regulators and supervisors have played a significant role, by maintaining or even raising the barriers for cross-border activity.

“In Europe it’s more of a cultural issue,” he says. “Financial institutions are seen as a source of risk, and [the view is that] if you minimise this risk, financing will come somehow. So the objective of regulations is not competitiveness, it’s just stability, stability, stability.”

Analysis by the ECB shows that the sizes of acquired banks in deals after the financial crisis are much smaller than before, while there is a higher failure rate for attempted mergers in the years since 2008. UniCredit and Commerzbank have previously made overtures to each other over a deal, while Deutsche Bank abandoned talks to merge with its German rival in 2019.

The ECB analysis found that about four in every five completed deals in the Eurozone were domestic. The few cross-border bank deals since the financial crisis have tended to be between institutions in neighbouring countries linked by common language or trade, such as Spain’s CaixaBank buying Portugal’s Banco BPI in 2017 or various smaller deals such as those involving Belgian, French and Dutch banks or the continuing pursuit of Austria’s Addiko by Serbian lender Alta Pay.

Partly as a result, European banks have fallen far behind their US and Asian counterparts since the financial crisis. While European lenders were focused on cleaning up their balance sheets and building up capital levels, their Wall Street rivals got bigger at home and increased their presence overseas, especially in areas such as investment banking and trading.

“Today, you can’t do a large financial transaction — M&A or infrastructure financing — without American financial institutions,” says Bini Smaghi. “European banks are too fragmented and don’t have the balance sheets. That is a fragility for Europe.”

The world’s 10 biggest banks by assets include just three European lenders — and one of them, HSBC, is headquartered outside the EU. The list is dominated by Chinese and US financial institutions, with France’s BNP Paribas, Crédit Agricole and Société Générale — along with Spain’s Santander — the only Eurozone banks to make the top 20.

By comparison, a similar ranking from 2008 featured eight European lenders in the top 10, with no Chinese banks and only two US ones.

The decline of European banks on the global stage is keenly felt by policymakers, not only as a sign of the continent’s waning international heft but also for its inability to finance important changes in its economy.

The main reason for the increased talk of dealmaking is banks’ improved financial health over the past few years, which has put buyers in stronger positions and is making targets more attractive.

After a wave of bank bailouts following the financial crisis — where lenders that had been on aggressive acquisition sprees or loaded up with toxic debt needed to be rescued — regulators imposed more stringent capital requirements. This led to a decade of pain, but Europe’s banks are now among the best capitalised in the world.

The speed with which central banks have raised interest rates since 2022 has been a boon for commercial banks, which typically generate most of their profits from the difference between the interest they receive on lending and what they pay out on deposits.

The fattening of the so-called net interest margin as rates rose led to a €100bn windfall for European banks over the past two years. This has generated excess capital above regulatory requirements, which some bank executives have considered spending on acquisitions.

But with few obvious targets available, many banks have increased their dividend payments and — for the first time — begun buying back their own shares. European banks have pledged to return more than €120bn to shareholders this year, with €47bn from share repurchases.

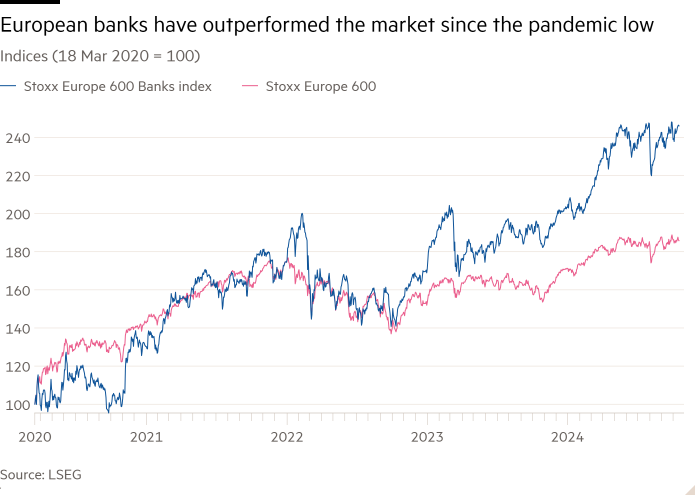

These promised returns have increased interest in a sector long-neglected by international investors. The Euro Stoxx Banks Index, which tracks Europe’s biggest listed banks, has risen more than 75 per cent over the past two years.

Bank executives have been cleaning up their institutions’ balance sheets through a series of deals known as significant risk transfers. Such transactions, where banks offload risk from their balance sheet to third-party investors, hit total notional values of €163bn in 2022 and €154bn last year, up from around €80bn in 2020, according to the ECB.

As interest rates start to fall, potentially eroding banks’ hard-won profitability, investors expect more interest in mergers. “If we see more revenue pressure in the sector — which I think is possible in the euro area if interest rates fall below 2 per cent again — I would bet that we get quite a lot of M&A to improve profitability,” says Schroders’ Bisseker.

For policymakers, the transitions to greener energy and a more digital economy and the need for remilitarisation following Russia’s invasion of Ukraine all point to a need for more lending capacity.

Cash-strapped governments are increasingly reliant on the private sector to provide this financing. Banks with bigger balance sheets and a greater appetite for risk are able to diversify where they lend and invest, and do so with larger commitments.

“Cross-border mergers have many advantages if they result in larger, more agile, more comprehensive and deeper institutions,” said ECB president Christine Lagarde last month.

“Banks that can actually compete at a scale, at a depth and at range with other institutions around the world — including the American banks and the Chinese banks — are in my opinion desirable,” she added.

But while policymakers are keen to stress the need for European super banks that can go toe to toe with their Wall Street counterparts, completing deals can still be fiendishly difficult and time-consuming.

BBVA’s €10bn approach to Sabadell has met with opposition from Spain’s Socialist-led government, which is wary of job cuts and branch closures — the traditional route to reducing operating costs following a merger.

Stefan Wittmann, a senior official at Germany’s services sector union and a member of Commerzbank’s supervisory board, last month pledged to fight a UniCredit takeover “tooth and nail”.

So-called “revenue synergies” between businesses can also be hard to achieve in practice, as it is often difficult to sell the same products in countries with different regulatory regimes or consumer preferences. Cost savings are also difficult, especially when expensive, risky and time-consuming IT integration projects are involved.

“All in all, the rationale for cross-border synergies on costs or revenues is very weak,” said Jean-Pierre Mustier, a previous chief executive of UniCredit, who drew up his own plan to acquire Commerzbank in 2017.

“We are very, very far from having truly efficient pan-European banking groups, as Europe is de facto fragmented.”

One sticking point is the lack of a set of Europe-wide bank rules that would allow lenders to operate in different countries seamlessly. Since the Eurozone crisis in 2009, policymakers have been pushing for a European banking union to provide a common financial regulatory framework.

Troiano, at Scope Ratings, says the lack of progress on a Europe-wide deposit insurance scheme to protect customers’ savings if a bank fails was a significant reason for the dearth of cross-border deals.

“If you have one or two cross-border deals happening, that could act as a catalyst and increase the sense of urgency for politicians to legislate what is needed,” he says.

“But it’s a matter of, do you put the cart before the horses or the other way round? The banks will not move unless there is complete banking union in place.”

Kian Abouhossein, a banks analyst at JPMorgan, adds that bigger banks are likely to be pushed by regulators into holding more capital, as UBS is finding in Switzerland following its takeover of Zurich rival Credit Suisse.

“The combination of regulatory demands for more capital for larger institutions, plus deposits not moving freely between countries, makes large transactions very difficult,” he says.

While investors tend to support bank mergers in principle, such obstacles have made them sceptical of cross-border deals in practice.

“We’ve shied away from European banks that have gone through empire-building,” says Brian Kersmanc, a portfolio manager at US fund group GQG Partners, a big investor in European banks and a top-10 shareholder in Commerzbank.

“It’s less of a positive if you are going cross-market. There can be cultural differences going into new markets and these are landmines that can trip you up.”

And for all the high-level enthusiasm for European financial champions, foreign takeovers of large financial institutions are highly controversial. National concerns and political considerations often override any desire to establish a new cohort of European super banks that can compete on the global stage.

Germany’s chancellor, Olaf Scholz, who has called for greater financial integration across Europe, responded to news of UniCredit’s stakebuilding in Commerzbank by saying that “unfriendly attacks [and] hostile takeovers are not a good thing for banks, and that is why the German government has clearly positioned itself”.

Asked by Bloomberg whether he would be prepared to allow a takeover of SocGen by a foreign rival in the name of greater financial integration across Europe, France’s president, Emmanuel Macron, replied simply: “Yes, for sure.”

But few believe that the one-time Rothschild banker — or any other national leader — would be so obliging if an offer were actually on the table.

Additional reporting by Harriet Agnew