Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

By most measures, Pfizer looks like the ideal target for some activist treatment.

The US pharmaceutical company enjoyed outsized gains during the pandemic thanks to its Covid-19 vaccine developed with BioNTech. Sales topped $100bn in 2022.

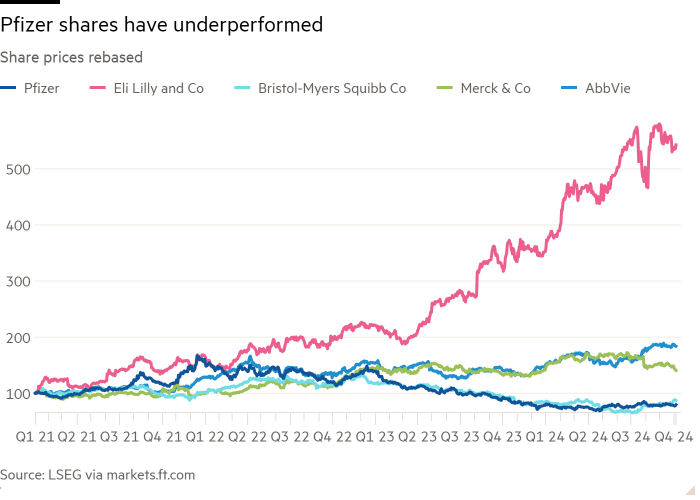

But as demand for the shot waned, so did sales. Attempts to develop an obesity drug have been a flop. Pfizer’s shares have fallen more than 50 per cent from their peak in late 2021, representing a loss of $177bn in market value.

The company is worth less now than before the pandemic. That is despite splashing out more than $60bn on a series of acquisitions over the past two years.

Small wonder then that Starboard Value has moved in. The activist investor has amassed a $1bn position in Pfizer. It has approached Pfizer’s former boss Ian Read and former finance chief Frank D’Amelio to help. But it has yet to reveal its plans.

The trouble is there are no quick solutions to Pfizer’s woes. The pandemic provided a once-in-a-lifetime windfall. Sales more than doubled and net income tripled between 2020 and 2022.

That success set a high bar that Pfizer could not meet. Its valuation at 11 times forward earnings is in line with its 10-year historical average. However, it is a fraction of Eli Lilly’s 42 times. That gap reflects Pfizer’s failure so far to find an anti-obesity treatment for its portfolio.

Albert Bourla, who was handpicked by Read to be his successor and took over in 2019, has binged on overpriced deals. These include Seagen, the lossmaking cancer biotech bought last year for $43bn, including debt. Pfizer expects Seagen drugs to generate $10bn in annual sales by 2030. That compares with the $58.5bn Pfizer pulled in last year.

Bourla’s big bet on cancer drugs could still pay off. But investor patience is in short supply, especially after Pfizer abruptly withdrew Oxbryta, a sickle cell disease treatment, from the market last month. The drug was the centrepiece in Pfizer’s $5.4bn acquisition of Global Blood Therapeutics in 2022.

Pfizer’s return on capital has fallen from more than 19 per cent in 2022 to 2.2 per cent last year, according to figures from S&P Global Market Intelligence. In response, Boula has announced big cost cuts — $4bn this year and another $1.5bn between 2025 and 2027.

Activist involvement could usefully impose more discipline. But swearing off portfolio development is not an option in innovative pharmaceuticals. Pfizer has already streamlined its business, shedding consumer health and its off-patent drugs unit. Sometimes it is easier to identify the symptoms of an ailment than prescribe an effective cure.