When Wall Street scrambled to launch bitcoin funds earlier this year, there was just one trading company named in regulatory filings as an anchor market-maker for every single one: Jane Street.

The move underscored how a quirky and opaque New York firm has used its dominance in exchange traded funds and embrace of more finicky financial securities as a springboard to become the most profitable of all the trading firms that are now a significant force in markets.

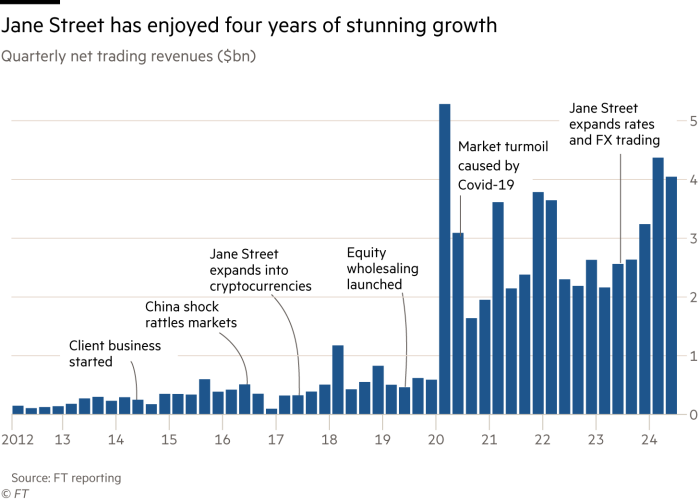

Last year was the fourth straight year that Jane Street generated net trading revenues of more than $10bn, according to investor documents seen by the Financial Times. Its gross trading revenues of $21.9bn were equivalent to roughly one-seventh of the combined equity, bond, currency and commodity trading revenues of all the dozen major global investment banks last year, according to Coalition Greenwich data.

“The amount of money they make is almost obscene. And that comes from handling instruments that many other people don’t want to touch,” said Larry Tabb, a longtime analyst of the industry who now works at Bloomberg Intelligence. “That’s where the greatest profits are, but also the greatest risks.”

There are no signs of Jane Street slowing down. In the first six months of 2024 net trading revenues rose another 78 per cent year-on-year to hit $8.4bn, according to people familiar with the matter. If it can match those revenues in the second half of 2024, it would mean Jane Street bringing more trading revenues than the vastly larger Goldman Sachs did last year.

If the 70 per cent profit margin disclosed in documents to investors is also maintained, it would mean Jane Street comfortably out-earning the likes of Blackstone or BlackRock this year, according to analyst forecasts collected by LSEG.

Jane Street’s prowess is particularly noticeable in the bond market, where it has rapidly muscled its way into a world long-dominated by banks and considered impossible for standalone trading firms to crack.

“You can think of the history of Jane Street as automating so that we can move on to the next task that’s somewhat more complex, and then trying to automate that somewhat more complex task, and then moving on to the next one,” Matt Berger, the head of fixed income at Jane Street, told the FT. “That’s been the constant evolution throughout our business.”

Nonetheless, Jane Street faces myriad challenges, both external and internal.

A trading company that long cherished its obscurity has now emerged as one of the industry’s most followed players, an uncomfortable position for many Jane Streeters. Rapid growth is testing what was once a flat, collegiate organisation. Rivals are trying to poach its stars. Some investors wonder whether its pivotal role as an intermediary in the rapidly-expanding universe of bond ETFs make it systemically important.

At the same time, rivals are fighting back, with banks keen on stemming its inroads into fixed income and Citadel Securities eyeing Jane Street’s corporate bond bonanza.

“It’s the classic innovator’s dilemma,” said one former Jane Streeter. “When they were the underdog they were moving really quickly and doing innovative things that no one else could. Now they’re the big gorilla. Of course people could catch up.”

Jane Street was founded by a handful of traders from Susquehanna and a former IBM developer in 2000. For most of its first two decades of life it happily stayed in the shadows of older, more prominent trading firms such as Virtu Financial and Citadel Securities.

It initially started trading American depositary receipts — US-traded stocks of companies listed overseas — on the now-defunct American Stock Exchange, out of a small windowless office. But it quickly branched out into options and ETFs, which the Amex had helped pioneer a few years earlier.

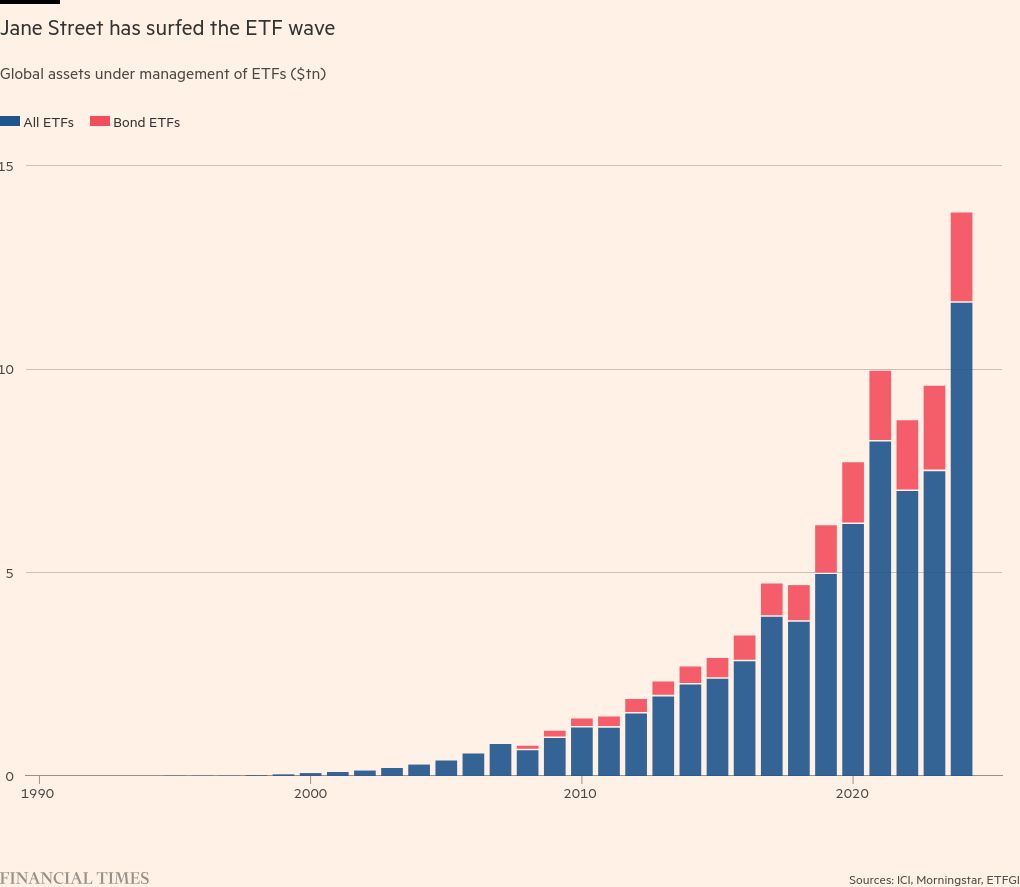

ETFs were a niche business at the time, with only about $70bn of assets when Jane Street started trading them. Still, ETFs quickly became its main focus, and over time it emerged as a significant “authorised participant” — a market-maker allowed to create and redeem shares in ETFs, in addition to trading them.

Jane Street is particularly strong in less mainstream ETFs. Former and current executives say the company’s love of puzzles — an integral part of its convoluted interview process — reflects and feeds a willingness to tackle knottier trading challenges, such as how to handle ETFs in less liquid markets such as corporate bonds, Chinese equities or exotic derivatives.

This means that speed is not nearly as important at Jane Street as it is for the likes of Jump Trading, Citadel Securities, Virtu or Hudson River Trading, even if the firm is often grouped with them as a high-frequency trader.

On a simplified spectrum ranging from more instinctual traders of pre-2008 investment bank “prop desks” to pure technologists like Citadel Securities or Jump Trading, Jane Street sits closer to the middle than many of the other companies it competes with, according to insiders and rivals. It will also hold positions for days, and sometimes weeks.

“It’s an interesting mix of technology and street savvy,” said Gregory Peters, co-chief investment officer of PGIM Fixed Income.

The bet on ETFs proved a smart one, thanks to the industry’s long boom. Assets are now approaching $14tn, according to data provider ETGI. Gradually and quietly, Jane Street developed a reputation as a place for wildly smart people who wanted to make wild amounts of money — one of the main aspects that drew a young MIT graduate named Sam Bankman-Fried to the firm in 2013.

But even inside its own industry it was mostly known for its eccentric embrace of OCaml, an exotic programming language, to build almost all its systems. For outsiders it remained a cipher (aptly, Jane Street has an original Enigma machine at its New York headquarters).

Such was its anonymity that three of the four co-founders quietly retired over the years without anyone outside of Jane Street making note of it, leaving the last, Rob Granieri, as what insiders describe as a first among equals. But Jane Street has no CEO, and in loan documents shared with investors, the company calls itself “a functionally-organised structure consisting of various management and risk committees”.

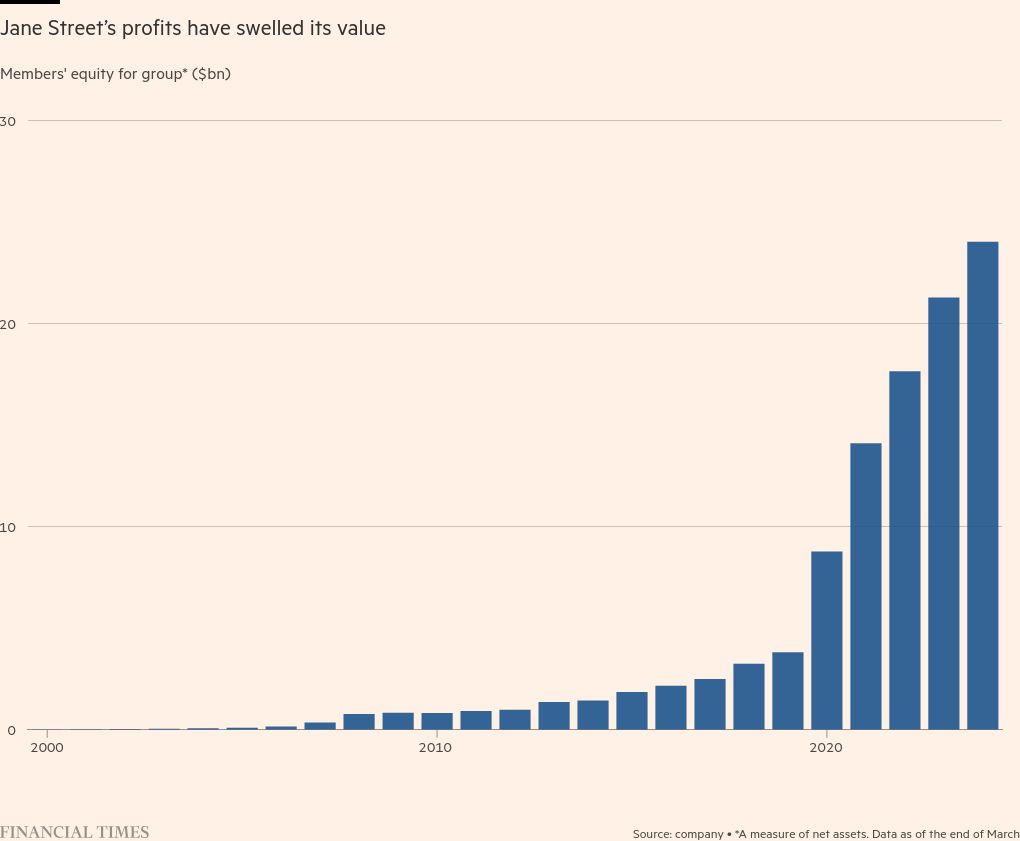

Every trading desk and business unit is run by one of 40 equity holders, who together own $24bn worth of Jane Street’s equity. Outsiders believe Granieri — who resembles a softly-spoken, lanky-haired extra from Silicon Valley more than a billionaire trading magnate — is the biggest of these, but Jane Streeters say big decisions are taken by the broader collective leadership group, which it argues fosters collaboration and minimises hierarchy.

This is reflected in its compensation structure — Jane Street eschews tying pay to personal trading profits, or even the earnings of a Jane Streeter’s desk — and its long avoidance of formal titles, even if this could cause confusion outside of the company.

“Back in the early days when you got these guys in a room they wouldn’t give you a card, they’d all be dressed in shorts and T-shirts and you’d have no idea who you were talking to,” Bloomberg’s Tabb recalls.

New titans of Wall Street — an FT series

This is the second in a series on the secretive trading giants that now dominate a key part of Wall Street.

The first instalment told the story of how the big banks, hamstrung by regulation, lost a technology arms race — and their trading superiority.

The other parts, outlined below, will be published in the coming weeks.

How Russian-born mathematician Alex Gerko has minted a £12bn fortune since founding London-based XTX Markets less than a decade ago.

How quantitative trading firm Susquehanna International Group cornered the market for options trading.

How Ken Griffin’s Citadel Securities manoeuvred to handle one out of four stock trades in the US while pilfering talent from large banks.

How Chicago pit trader Don Wilson built derivatives and cryptocurrency trading giant DRW

However, Jane Street’s low-key profile started to slip in 2020 when the enormous profits it racked up from trading through Covid-rattled markets made headlines.

Comfortably out-earning even Ken Griffin’s Citadel Securities made people take notice, and whispers of enormous pay packets sparked envy across Wall Street. Underlining its arrival on the biggest stage, in September 2020 the Federal Reserve added Jane Street to its list of acceptable counterparties for its crisis-fighting measures, alongside Wall Street stalwarts such as JPMorgan.

It then received a flood of attention as the company where Bankman-Fried started his trading career before founding now-failed cryptocurrency exchange FTX. The publicity made many at Jane Street viscerally uncomfortable, not least because the cavalier approach to risk and compliance that landed Bankman-Fried in jail was seen by many insiders and outsiders as the antithesis of Jane Street’s obsessively paranoid approach.

In addition to a 14-person central risk hub that constantly monitors all of Jane Street’s fluctuating exposures, the firm says it maintains an extra “liquidity buffer” of about 15 per cent of its trading capital. This is held outside of the prime brokerages through which it does most of its business.

The war chest is meant to ensure that Jane Street can hang on to positions even when markets are chaotic. On top of this, the firm is a heavy user of derivatives to insure against both smaller idiosyncratic shocks that might rattle an individual desk, and broad financial earthquakes that might shake the entire company.

Jane Street attracted more unwelcome headlines earlier this year, when it sued a pair of former traders that in February defected to work for hedge fund Millennium Management. Jane Street indicated in court documents that the subsequent deterioration of an Indian options strategy the traders allegedly took with them was costing it more than $10mn a day. Since then the two companies have been fighting a legal battle over who has to hand over which documents.

The hoopla does not seem to have slowed Jane Street down, however. The speed at which its trading revenues continue to grow underscores how its market footprint keeps swelling in stocks and options. Over the next year it wants to expand further in trading government bonds and currencies, and was “expanding significantly in the scope and ambition of our machine learning work”, according to Berger, in terms of people, infrastructure and computing power.

But its core remains ETFs, a sector in which it accounted for 14 per cent of all US trading last year, and 20 per cent of European trading, according to documents Jane Street shared with lenders. In bond ETFs, Jane Street estimates that it accounted for 41 per cent of all creation and redemption transactions last year.

That dominance has allowed Jane Street to expand into trading the underlying bond markets as well, a realm where banks have historically ruled supreme, and a big point of differentiation with peers.

“The firms that are technologically inclined, who can see that and price that in real time, will make more money,” said Alexander Morris, chief investment officer of F/m Investments, which uses Jane Street as a market-maker for its bond ETFs.

“Because they’ll be faster, but also offer fairer prices, because their goal is to sell the shares and execute that trade and move on to the next. They don’t get paid anything extra from taking more time on the trade.”

However, after several bountiful years there are hints that Jane Street is coming under more pressure.

Many banks have been investing aggressively in technology and retooling their trading teams to counter threats from the likes of Jane Street, both in equities and bonds. These efforts are now beginning to bear fruit. “They’ve closed the gap a lot,” said Adam Gould, global head of equities at Tradeweb.

At the same time, Citadel Securities — already a major player in government bond markets — has pushed into corporate debt too. “There’s definitely increased competition, and I think it’s good for the overall ecosystem and good for investors,” said Berger.

However, Jane Street’s biggest challenge may be internal. Maintaining a collaborative, no-hierarchy culture is easier when everyone can fit into one floor in New York. But at the end of last year there were 2,631 full-time employees, of which nearly half worked in outposts from Singapore to Amsterdam.

That is one of the reasons why Millennium’s poaching made waves. A larger, less cohesive Jane Street could start to lose more staff and more strategies could leak, increasing the pressure on a company that has until now enjoyed a golden touch.

“Even in the bad years, Jane Street could still pay people very well. But that was when they had 100-200 people. You now have almost 3,000 mouths to feed,” observes one former Jane Streeter.

“If Jane Street has a less than stellar year it will really be felt. If they have just one year where they’re just flat-ish then they’re in very big trouble. And that’s a precarious position to be in.”