Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

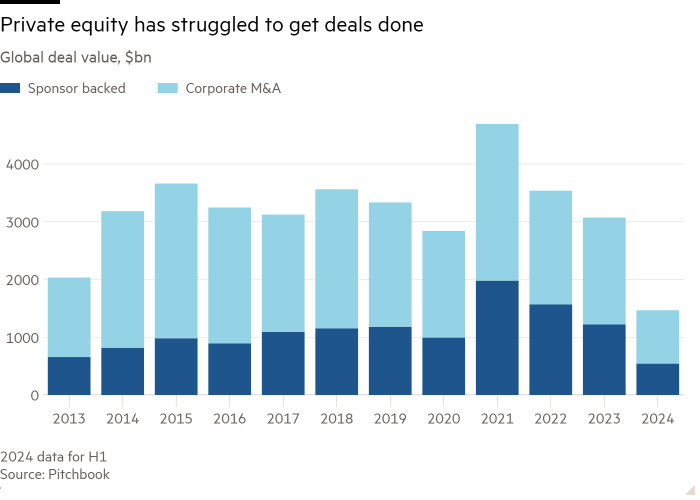

The success of a leveraged buyout strategy depends, in large part, on the availability of leverage. When debt is scarce and costly, it is hard for private equity investors to make deals stack up. That has been one reason for the recent paucity of LBOs. That trend is now inverting. Sponsors are putting the “L” back in LBO.

Take a look at the separation of Sanofi’s consumer health business, Opella, valued at perhaps €15bn. The French pharma group is running a twin-track approach. It is considering a potential spin-off, but has also tested appetite for a sale of about half the business to private equity. It has reportedly received bids from Clayton, Dubilier & Rice and PAI Partners, highlighting the renewed ebullience of debt financiers.

Lex understands that more than 20 banks showed interest in financing a deal. Between banks and private credit lenders, bidders have amassed total debt packages equivalent to 7 times this year’s expected ebitda of perhaps €1.15bn. The lion’s share of this, €8bn or so, is senior debt. The junior debt tranche — about €1bn — includes a payment-in-kind option.

That is a hefty financing package. In part, it reflects the fact that Opella is a blockbuster deal coming after a dry-ish spell, so lenders are jockeying for position. But leverage is starting to rise more broadly. In Europe, the percentage of transactions completed between 6 and 7 times ebitda has risen to more than 20 per cent this year, on PitchBook LCD data, a near-doubling from 2022 levels.

This reflects increasingly favourable conditions for borrowers. Interest rates have dropped. There is a lot of pent-up demand for high-yielding debt, from CLO funds and private credit investors. Banks have been competing to regain market share from private credit lenders. Overall, since the end of 2023, funding costs have declined by about 1 percentage point for the average European LBO borrower, according to PitchBook LCD.

Alongside rate cuts, looser purse strings bode well for a reprise in private equity activity. But it is not a slam dunk. Valuations for sponsor-led transactions are also rising, meaning that despite the availability of debt, bidders may need to stump up big slugs of equity to get deals done.

Bids for Opella, for instance, have reportedly come in at about €15bn. That is not nosebleed territory, implying a 16 per cent valuation discount to larger listed rival Haleon. But at these levels, and despite lashings of debt, about €7bn of the transaction would need to be financed with equity. The fact that Sanofi aims to retain about half of the business makes the outlay more manageable, in this case. Those running their slide rules on other targets may find the task remains daunting.