Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Billionaires (sometimes) do not let billionaires go bankrupt. For a price, at least.

For a year, some Wall Street vultures dreamt that EchoStar — the satellite TV and telecoms empire assembled by Charlie Ergen — would fall into Chapter 11.

That would have handed control to its creditors, owning more than $20bn of EchoStar debt.

But on Monday, David Bonderman decided to play white knight. The private equity firm he co-founded, TPG Capital, said it would lead a rescue transaction that keeps Ergen’s EchoStar equity afloat.

TPG’s satellite TV provider, DirecTV, will acquire its arch-rival Dish Network from EchoStar. The official purchase price is $1, along with assuming billions in Dish’s currently distressed debt.

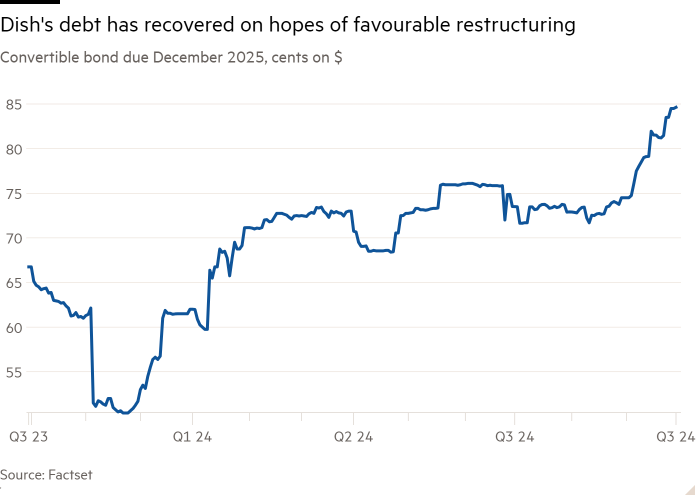

TPG, however, will not make those bondholders whole, conditioning the DirecTV/Dish merger on $11.7bn of bond debt taking a $1.6bn haircut. Those bondholders can decline if they like.

But the bet by Ergen and TPG is that those creditors can live with a modest discount to avoid having to run a complicated business that is in decline. As it happens, the hand of those main bondholders had already been forced.

Nearly all holders of convertible bonds, who are owed around $5bn in principal due soon, agreed to swap their debt at a small discount in exchange for a better coupon, enhanced collateral and the chance to reinvest in EchoStar.

TPG’s bargain contains its own risks. It is providing $2.5bn in the form of debt to solve pending maturities at Dish. It also said on Monday that it would pay $7.6bn over the next several years to buy out AT&T from the 70 per cent of DirecTV still owned by its telecoms partner.

The combined company will have 18mn pay-TV subscribers, a deterioration of several million in the past decade. But private equity firms care more about cash flow than revenue growth.

The combined company retains almost $10bn of annual ebitda, according to researcher CreditSights, setting its likely enterprise value between $30bn and $40bn. TPG’s risk is largely mitigated by investing at a cheap valuation, and the cash it has and will continue to extract.

Ergen will now concentrate on the EchoStar stub, which is a portfolio of spectrum and a play on building a new mobile phone network.

Its shares fell by more than a tenth on Wednesday, a personal loss for Ergen of a few hundred million dollars. But it could have been far worse, if not for the intervention of Bonderman & Co.