Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

There are a few sages who predicted all along that 2025 — not 2024 — would be the year to watch for IPOs. More have joined them as deal flow remained depressingly soggy. Will 2025 really be any better? Companies going public like certainty. There is not much of that in prospect.

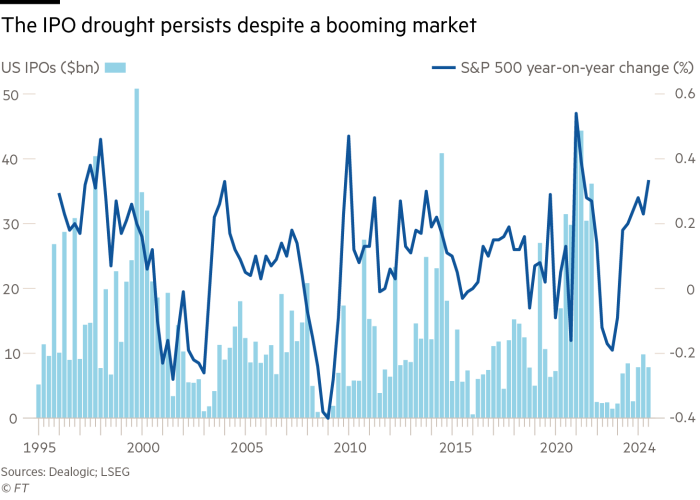

The looming US election makes the September quarter-end a good point to call time on the IPO class of 2024. Few executives will be prepared to risk the choppier markets that usually surround November votes. So far this year companies have raised some $26bn by going public in New York including social media group Reddit and cruise operator Viking. That beats $20bn raised in all of last year and positively sparkles compared with $8bn in 2022. But it is still the sort of amount that was being raised every six months in the years before the 2020-21 boom.

The argument for 2025 is that companies have still spent this year dealing with the fallout from that period. Valuations needed to deflate. Executives had to flip from talking up top line growth and start discussing plans for net profitability. If 2022, when the S&P tumbled 19 per cent, was the stuff of start-up nightmares then 2023’s 24 per cent rally despite fears of a recession (still yet to materialise), plainly caught them off-guard.

That left 2024, curtailed by the November election, to prepare for a listing. There is probably a handful of companies that rue not being ready sooner: strong markets between March and June this year could probably have supported more deals than landed.

The IPO market is a lumpy way to make a living. Take 2014 where Alibaba’s bumper $25bn float skews the numbers. In 1999, when BlackRock and Goldman floated alongside dotcom stars, those names were dwarfed by UPS’s $5.5bn deal — then a record.

Still, the last couple of years have been quiet by any measure. This time, an IPO recovery is more reliant on some predictability, rather than a roaring market. As August’s rout showed, it doesn’t take more than a couple of economic releases to trigger wild moves. The Fed this month made clear that it, too, will react to future data. That leaves listings wannabes attempting to plan for IPOs to fall neatly between mood-altering monthly jobs reports.

Forget about 2024. But the IPO recovery is coming — just perhaps not as quickly as some hope.