Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Not for the first time, Springer Nature is testing choppy waters. The private equity-backed publisher of journals such as Nature and Scientific American called off flotations in 2018 and 2020. But the Berlin-based company is now confident enough to plan Europe’s first big IPO of the second half of the year. It should fare better.

Market volatility was not the only reason that previous attempts stalled. In 2018, the only time it got as far as publishing a prospectus, investors balked at the high debt and price expectations, amid concerns about the sustainability of the business model. The 2018 prospectus suggested Springer Nature’s market capitalisation would be about €3.6bn.

This time round, the owners — BC Partners with a 47 per cent stake and Holtzbrinck Publishing Group, a privately owned company that has the remainder — may value the equity at least a quarter more highly. The group could fetch an enterprise value of about €6.5bn-€7.5bn. That estimate assumes a 10-20 per cent IPO discount to an EV/ebitda multiple of 11 times, based on analysts’ assessment of peers such as Relx’s Elsevier and Informa’s Taylor & Francis.

Springer Nature is a more attractive proposition than in 2018. Then, its post-transaction leverage was 3.5 times 2017 adjusted ebitda. This time, its debt-to-ebitda ratio would be about 2.4 times if the expected €200mn gross proceeds from the Frankfurt listing is put towards debt reduction.

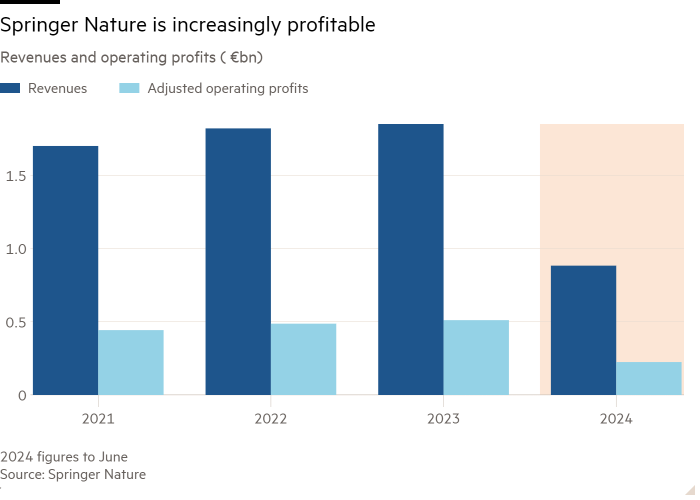

It has also increasingly switched from a pay-to-read to pay-to-publish model. This year, the number of “open access” articles is expected to rise from 44 per cent last year to half. The shift has not harmed its profitability. In the four years to 2023, the adjusted operating profit margin grew by an average of 0.9 per cent a year.

Its margins of 28 per cent are only three-quarters those of Relx’s Elsevier, the market leader (which also has data analytics). Even so, they are a cause of resentment by cash-strapped universities and funders. Some of the latter are stopping paying publication fees, amid calls for a reform of grant criteria to reward publication in less expensive journals.

But predicting the demise of academic publishers’ high profit margins is a tradition nearly as old as the internet. So far at least it has been greatly exaggerated.

The prestige of Springer Nature’s top journals gives it leverage. As one of the largest academic publishers, it has the advantage of scale when it comes to spreading technology and marketing costs. With the global research publishing market expanding at just over 3 per cent a year, Springer Nature should be capable of steady, if not spectacular, growth.