Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

There are 23 pairs of human chromosomes. Decoding them might only be worth 40 cents per share. 23andMe was once a high-flying consumer healthcare start-up, with admirable DNA itself. The founder, Anne Wojcicki, is part of a prominent Silicon Valley family and herself is a longtime healthcare investor. The company’s backers include Wojcicki’s former husband, Sergey Brin, the Google co-founder. Other large investors are Richard Branson and GSK.

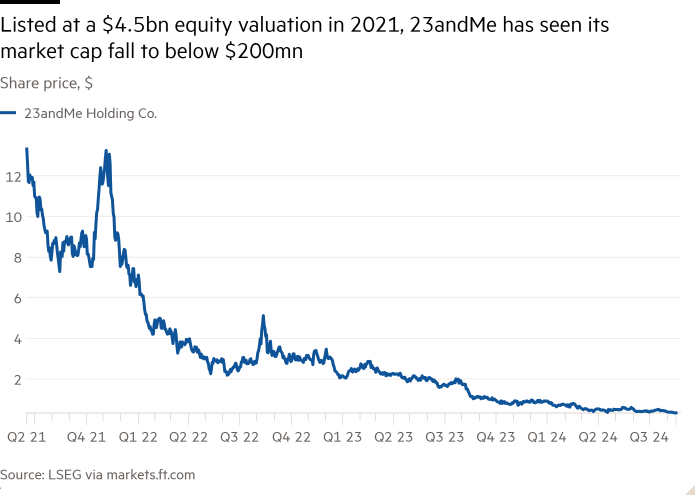

But after listing its shares at a $4.5bn equity valuation, through Branson’s Spac, its market capitalisation is now below $180mn. Wojcicki is attempting to take 23andMe private at just 40 cents per share. It is an extraordinary achievement that a simple saliva sample returned by post can now be transformed into a detailed genetic test. But the barrier still to be broken is that of a viable business.

23andMe has various segments. The first is the consumer testing business, where for as little as $99 customers can get their DNA and ancestry analysed. Another involves selling the data that the company collects to researchers. Its drug development business is, however, being wound down while the company recently said it would offer weight-loss services to members of its subscription service.

For now, virtually all of 23andMe’s revenue comes from the consumer business. And it’s not a great business. In its recently completed fiscal year, it generated just $220mn in total revenue. When it listed its shares in 2021, it forecast almost twice that figure. Moreover, customer acquisition costs are elevated and its ebitda loss for fiscal 2024 was $176mn.

Wojcicki wishes to buy the 80 per cent of the company that she does not own. The Spac deal left nearly $1bn of cash on the 23andMe balance sheet. That figure was down to just $170mn at the end of June. Directors criticised the bid as lacking details around the financing secured by Wojcicki, along with a price that offers no premium to the trading price.

What has become clear is that merely interesting technology was enough to get a public listing in a more lenient era. The commercial aspects were undeveloped. 23andMe might get the space to figure out those elements away from public markets and may even be better off within a larger corporation. As for the remaining shareholders, they may not be getting a superior bid than 40 cents as the company is burning cash. The hope is to avoid a takeover price set at 23 cents or less.