London has fallen behind New York, Toronto and Sydney as a global venue for mining company listings, and investors warn it is in danger of being “sidelined” by a sector it once dominated if a few major groups head overseas.

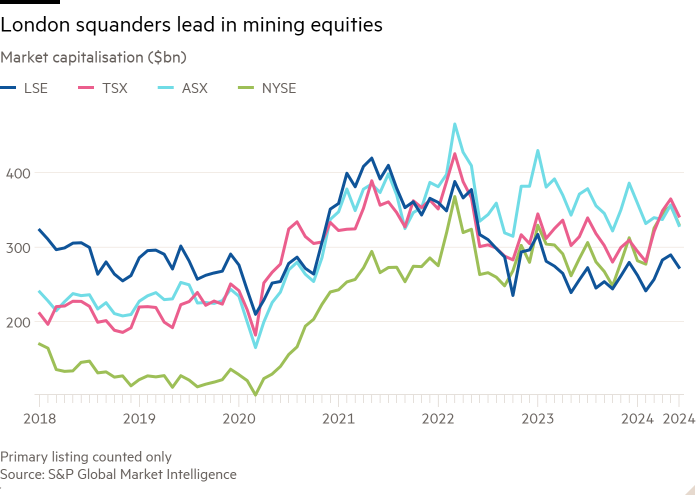

The market capitalisation of London-listed mining stocks has shrunk to $272bn this year from $322bn in 2018, while rival bourses in Australia, Canada and the US have all overtaken it and now each have mining sectors worth more than $325bn, according to data compiled by S&P Global Market Intelligence.

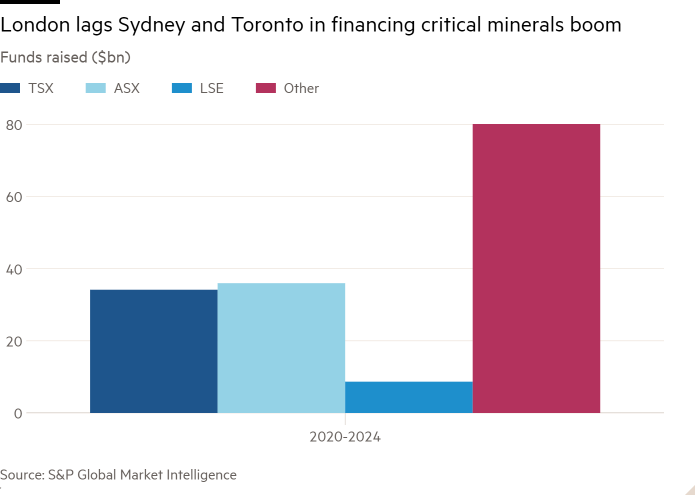

More money is also being raised abroad than in the UK: London Stock Exchange-listed miners have raised just $8bn since 2020, less than a quarter of the amounts raised in Sydney and Toronto.

The data highlights how, while London unsuccessfully chases after high-growth technology company flotations, it risks losing its historic edge in a global resources sector for which it has been the natural listing venue since the days of the British empire. The mining sector has been taking on new importance in recent years as it provides critical minerals for the transition to cleaner energy.

“The market is focused on the tech sector,” said Robert Crayfourd, portfolio manager at asset manager CQS. “But it is important that London, which has been historically an innovative and supportive centre for mining stocks and mining finance, does not pull back further, otherwise companies will look to other centres, leaving London sidelined.”

From the late 19th century onwards, London attracted large mining companies that operated in parts of the British empire, such as South Africa and Australia, before it played a central role in another boom for Australian mining stocks in the late 1960s.

There are 171 metals and mining companies on the LSE, accounting for 17 per cent of the world’s market capitalisation for the sector. Yet of those, most of the value resides in a handful of large companies such as Glencore, Rio Tinto and Anglo American. More than 100 of them have a market capitalisation of less than £100mn.

London suffered a double blow in 2022, as Russian gold producers delisted from the LSE following the invasion of Ukraine, and BHP moved its primary listing to Australia as it unified its dual corporate structure. Rio Tinto has come under pressure from activist investors to follow suit, while Glencore is considering spinning off its coal division to be listed in New York, and Anglo American is selling assets after coming close to being bought by BHP.

Losing Anglo or Glencore is a “huge risk for the London market”, said Hayden Bairstow, a Perth-based analyst at financial advisory firm Argonaut, who worked in London in the early 2000s when the mining sector was thriving.

The shift away from London has been driven by higher valuations and deeper liquidity in the US, which has now become an attractive destination for larger Canadian-listed groups to move to. Companies can often find investors outside of Europe less demanding on environmental, social and governance measures.

The popularity of diversified miners in London producing iron ore, coal and diamonds has waned in recent years, as the broad-based commodity boom driven by China’s rise has given way to an investor preference for companies just producing higher growth metals such as copper for the green transition.

The top five miners in London have an enterprise value, which includes debt, of 5.2 times their core earnings, compared with 9.4 times in Canada and 6.8 in the US, according to Financial Times analysis. The drag of China’s property market slump on iron ore has pushed Australia’s top five miners down to trade at 4.9 times core earnings.

Canada and Australia have also been helped by their own thriving domestic mining sectors that pension funds, particularly in Australia, invest in to boost the local economy and jobs. African mining, traditionally a focus for London, has more recently been dominated by Chinese companies, which, if they list, are more likely to do so in China or Hong Kong.

More broadly, the mining industry is suffering from the amount of capital being sucked in to megacap tech stocks. Many in the industry believe that, despite being central to the green energy revolution by supplying the basic ingredients of wind turbines and electric vehicles, the sector has become all but irrelevant for investors, with many stocks too small for institutional funds to bother with.

The MSCI Mining and Metals index of the sector’s 46 biggest companies globally is, at $855bn, one-third of the size of US chipmaker Nvidia.

The lack of liquidity in London has been acute for miners, said CQS’s Crayfourd, citing low levels of retail investor participation, increasing liquidity requirements at UK wealth managers and ESG, which is leading many investors to shun the sector.

“Fundamentally” the LSE needs to get more capital into the market, said Tom Attenborough, the exchange’s head of international business development, at the London Indaba industry conference last month.

He added that it would address the “hollowing out” of medium-sized miners worth between £200mn and £5bn in London — shrinking from 60 to 20 groups since 2010.

“There was a deep bench [in London in the 2000s] but it’s not any more,” said Argonaut’s Bairstow. By contrast, for individual Australian investors, backing mining stocks is “part of our investor psyche”, he added.

Mining stocks used to be seen as a high-risk, high-reward trade for retail investors but they have fallen out of favour during previous commodity price downturns, and have also been overshadowed by the cryptocurrency boom.

“Why is it that you can be standing in a street corner with your mobile phone and with a couple of clicks buy crypto in a completely unregulated market but struggle to participate in an initial public offering in a very regulated market with a prospectus? That’s nuts,” said Attenborough.

Jim Rutherford, chair of London-listed gold miner Centamin and a former Anglo American board member, said at the conference that London suffers from “regulatory overkill”, citing how hard financing is to raise quickly and “onerous” responsibilities on board members.

However, for Dean McPherson, head of global mining for TMX, which owns the Toronto Stock Exchange, the focus is on getting Glencore, Rio Tinto and Hochschild to move over from London.

“The data speaks for itself,” he said. “Those companies should give good thought to Toronto.”