Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Beauty products are touted as virtually recession-proof. When times are good, consumers slather on the anti-ageing, plumping and illuminating serums. When times are bad, the so-called “lipstick effect” kicks in. With so much crimping and saving going on, a smallish splurge on a beauty product gives shoppers that much-needed pick me up.

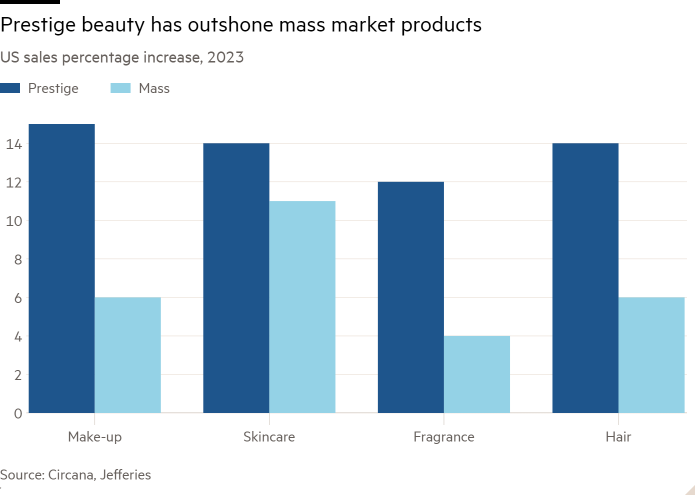

Yet here, too, there are signs that consumer weakness is starting to bite. “Mass” beauty in the US has shown softish sales for some time. Now that weakness appears to be creeping up the ladder to “premium” beauty — which has been the hottest area in the sector given that those tiny bottles of expensive lotion have staggering gross margins.

Unilever’s results last week referenced a slowdown in its prestige beauty division, where it holds brands such as Dermalogica and REN. Beauty retailer Sephora, owned by LVMH, last week missed analyst estimates, albeit with a reasonable-looking 5 per cent growth rate in the second quarter. Evidence of a slowdown is still patchy, however. Switzerland’s Galderma, maker of neuromodulator injectables (better known as Botox to the rest of us), has continued showing strong sales. Industry bellwether L’Oréal — reporting on Tuesday this week — will be closely watched.

Signs of a slowdown in the prestige beauty sector would chime with recent evidence that consumer weakness has become broad based and that even those with higher disposable incomes are starting to feel the pinch. Even at France’s Hermes, positioned at the very highest end of luxury, sales of aspirational products such as silk scarves fell 5.6 per cent in the second quarter of this year.

If the gloss is coming off premium beauty, that would be bad news for the many acquisitions which have been completed in the sector in recent years. Those were priced for a blemish-free performance. Think for instance of L’Oréal’s acquisition of Aesop at 24 times ebitda. Elsewhere, Unilever bought Paula’s Choice for 20 times ebitda, reckons Jefferies, and Colgate went even higher upmarket with Filorga at 30 times ebitda.

There are ways to apply balm to any potential rough patch in high-end skincare. One option is to stretch brands downmarket, rather than up. Estee Lauder, for instance, is selling its Clinique brand through Target stores in the US.

Another is to have a stable of brands at different price points, which can pick up cyclical slack from one another. L’Oréal here is a prime example. Its CeraVe dermatological brand is lauded by skincare influencers and — at an average price of about $20 — costs a fraction of ritzier potions. It should be well positioned to freshen up the temporarily straitened high-end consumer.