Reckitt is the consumer giant known for making everything from Dettol to Durex. But on Wednesday, the FTSE 100 group unveiled plans for a more streamlined company by selling off a part of its homecare business and its troubled infant-formula business in order to focus on its best-performing “power brands”.

The announcement mirrored one by rival Unilever last October when the UK-listed group said attention on a few big brands would help turn around years of disappointing performance. A few months later, the company that makes Marmite and Dove soap announced it was selling a bundle of slow-growing beauty brands, and in May, its entire ice cream division.

It is not just brands Unilever is cutting: about a third of office jobs in Europe are to be slashed by the end of 2025, the Financial Times reported this month.

The British giants are not alone in reconsidering their diverse business model. From Procter & Gamble to Danone, the overwhelming mantra among consumer-goods companies around the world is that a leaner portfolio is better than the multi-category heft the sector was once known for.

“Today the staple markets are way more mature. There is hardly any growth,” said Bernstein analyst Bruno Monteyne. “Everyone is super efficient, but when things are more efficient it becomes more important to be the best at what you do.”

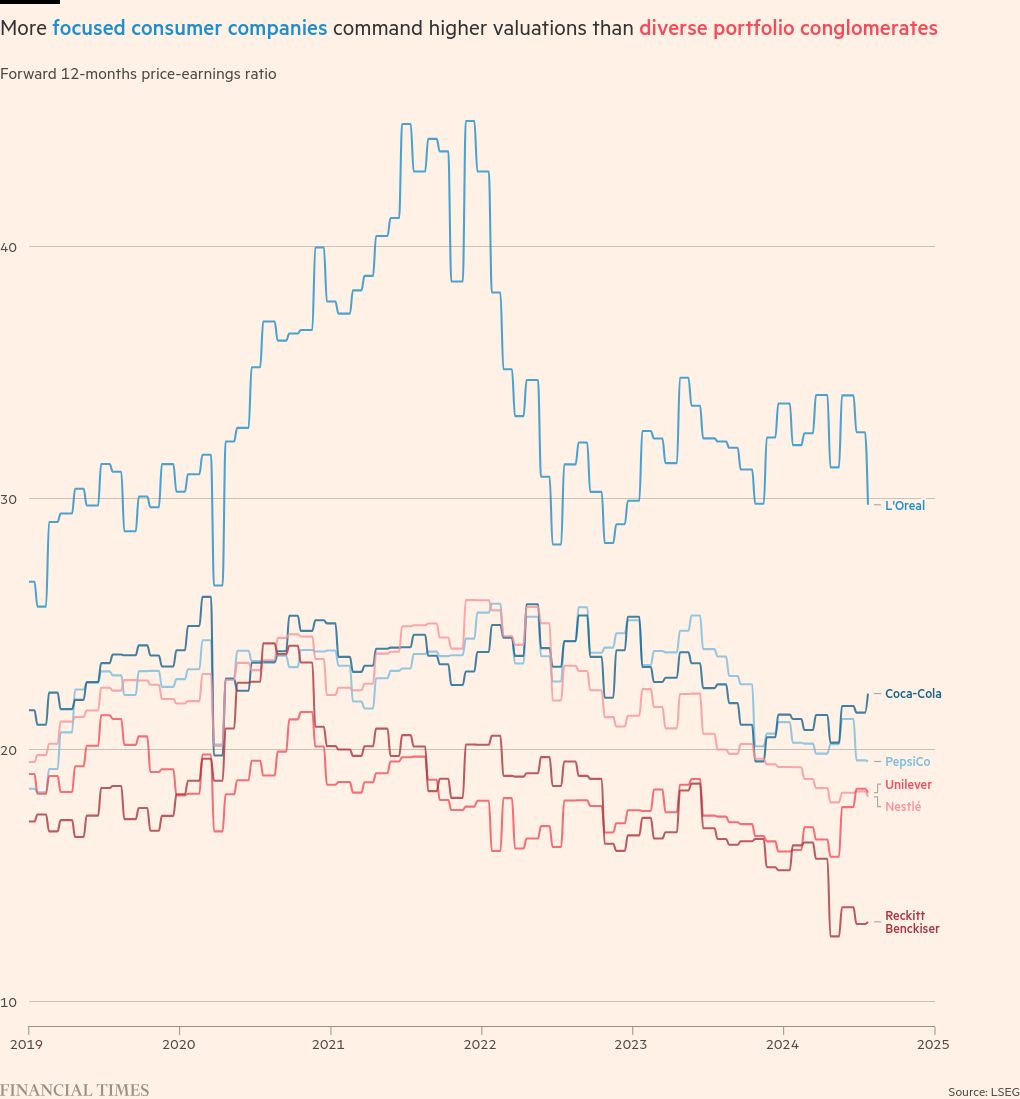

Conglomerates such as Unilever have often been unfavourably compared by investors to more focused businesses including L’Oréal, which concentrates exclusively on beauty, and Danone, whose portfolio is dominated by “healthy” brands in water, yoghurt and infant formula.

Until a decade ago, consumer goods conglomerates grew consistently, thanks to a scaled business model, which allowed them to buy up brands and plug them into sophisticated marketing and distribution systems to export around the world.

Now companies are fast approaching an efficiency ceiling, which has left them vulnerable to more specialised competition, and in turn to activist investors looking to shake things up for better shareholder returns — veteran activist Nelson Peltz at Unilever key among them. The companies’ solution is to divest lower growth or margin businesses in a bid to make the remaining portfolio more attractive.

“These companies were created a while ago, they have decades of experience,” said François Faelli, a partner at Bain, the consultancy. “If they can’t achieve growth of between 5-7 per cent, maybe they are the wrong owners.”

Even before Peltz targeted Unilever, eventually joining its board, the company had been selling off large chunks of assets, including its spreads business in 2017 and its tea business in 2022.

French food group Danone previously fell prey to activist call to sell off slow-growing brands. Shareholder Artisan urged the company to separate its medical nutrition and infant formula units, and sell brands that did not fit with the rest of the portfolio.

“Activists can accelerate the process,” said Monteyne at Bernstein. “Companies have a lot of inertia, while activists have no history and they can help to put on some pressure.”

Analysts say the model for the success of a more focused portfolio is US giant P&G, which has outperformed the rest of the sector since it sold its beauty business to Coty, split off battery business Duracell as well as disposing of food brands to focus on home and personal care.

Bain’s Faelli said the shift from scale to focus demanded by shareholders was ultimately the result of macroeconomic factors, including GDP pressures, slowing population growth and inflation.

While the Covid pandemic gave certain categories such as household cleaning and beauty a boost as consumers splurged at home during lockdowns, the overwhelming trend has been for consumers to buy cheaper supermarket own-brand goods, amid heightened competition as a result of high inflation and the ensuing cost of living crisis.

“The relative attractiveness of the consumer sector for shareholders has degraded compared to tech,” said Faelli. “It doesn’t mean you don’t still have spectacular companies, but the tolerance for mediocre performance is very low today.”

Two top-10 shareholders in Reckitt, Flossbach von Storch and Causeway Capital, told the FT ahead of the company’s announcement this week that they had called on it to sell Mead Johnson, the infant-formula business that has been a thorn in the side of Reckitt since it acquired it for $17bn in 2017. Its troubles culminated in March, when a decision by an Illinois court to award $60mn in damages to a mother whose child died after consuming a Mead Johnson formula wiped £5bn off Reckitt’s market value.

In 2020 Reckitt announced a $5bn writedown on the Mead Johnson acquisition, blaming falling birth rates and local competition in China. The following year Reckitt sold its Chinese arm to local private equity group Primavera and then tried to offload the US business without success.

Barclays now estimates Mead Johnson’s value to be around £5bn, excluding the discount a buyer might demand to factor in the litigation risk.

Activist Bluebell, which holds a small stake in Reckitt, went much further and called for a split of the company’s hygiene and health divisions so that it would be better placed to take part in the anticipated consolidation of various consumer healthcare spin-offs from pharmaceutical companies GSK, Johnson & Johnson and Sanofi.

Reckitt chief executive Kris Licht told the FT that he rejected the need for a further separation of the businesses into hygiene and health — an idea first tabled by former CEO Rakesh Kapoor in 2018 — arguing that there were plenty of “synergies” between the two businesses.

“P&G operates in many different segments. That doesn’t preclude them from driving good performance,” he argued. “I think the problem with conglomerates is a real problem, but we’re not a conglomerate. We’re in very synergistic businesses.”

A 2023 Bain analysis of spin-offs found that after three years, shareholder returns from the spin-off and its parent company combined increased 5 per cent on average.

In the short term, carve-outs added complexity, cost and confusion internally, said Monteyne. But if the separated business became better run, the execution should give a future uplift, he added.

David Hayes, analyst at Jefferies, said he was pleased to see after Reckitt’s news that investors were questioning the value creation from the sale of an asset over and above its intrinsic value.

Reckitt said this week that it expected the reorganisation and cost-saving programme to incur a one-off cost of £1bn.

“You’re never going to get more than your intrinsic value as a seller,” said Hayes. “And therefore I have to believe that you are going to get that core focus benefit, and I need to see that first.”