Blackstone Group has become one of the biggest buyers of a type of bank loan that has become a lifeline for the private-equity industry, exposing the company to risks generated by its own business.

The world’s largest buyout group, which manages more than $1tn in assets, has in the past year emerged as a big investor in risk transfer products that are underpinned by short-term loans used by private equity fund managers to close deals as they wait to receive cash from their backers.

Because of its sheer size, Blackstone has assumed risk on credit lines attached to its own buyout funds, though the firm said they only constitute “a single-digit percentage” of the portfolios on which it has exposure.

Such transactions magnify the private equity behemoth’s exposure if an investor were unable or unwilling to fund their commitment.

“The unusual thing about Blackstone is that it is a bit circular,” said one large SRT investor. “They are providing protection on themselves.”

The dealmaking underscores how intricate and interconnected the private capital industry has become and how new pockets of risk can build up within less regulated corners of the financial system.

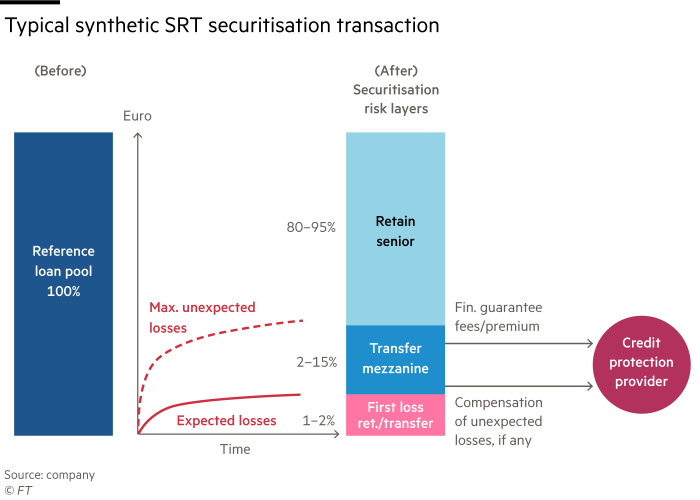

Banks in Europe and the US have been finding investors willing to assume some of the default risk on their loan portfolio in so-called significant risk transfer transactions (SRTs).

Such risk-transfer deals allow lenders to reduce the amount of capital they are required by regulators to hold and thereby boost returns.

Blackstone has recently become a large investor in SRTs underpinned by subscription lines, which are short-term loans used by private equity funds to close deals in advance of receiving cash from their backers.

For some years private equity firms have funded their corporate buyouts with debt provided by their own credit funds. The recent SRT transactions, which can themselves be part funded with bank debt, come at a time of growing concern for regulators over lack of transparency in private markets.

Jonathan Gray, president of Blackstone, told investors in an April earnings call that the group was a “market leader” in SRTs. He highlighted subscription lines as an area of particular interest because they are considered to be safe assets.

“The most active area has been subscription lines to date, which . . . have had virtually no defaults over the last 30, 40 years. So we like that area,” he said.

Blackstone disputed the circular nature of the risk, saying its investors were “the ultimate risk counterparty the lender is exposed to”. It noted that its investors had never missed a capital call in its 40-year existence.

The group added that its funds made up “a single-digit percentage of the portfolios on which we have provided SRTs” and that all their subscription line SRTs “have been in highly diversified portfolios”.

The Wall Street-listed group had been buying the assets through its Blackstone Multi-Asset investment unit, which manages hedge fund-type investment strategies, according to people briefed on the matter.

Banks typically use SRTs to buy protection against default on a pool of loans. This can either be done through a traditional cash transaction where assets are moved to a special-purpose investment vehicle that issues bonds, or through a derivative product while the lender keeps the assets on its balance sheet.

Asset managers and hedge funds, including $244bn Dutch pension fund PGGM and New York-based firm DE Shaw, have also been among the largest buyers.

The market for these products first developed in Europe following the 2008 financial crisis as lenders were requested to meet more stringent regulatory capital requirements. US banks became more active last year, after the Federal Reserve gave a blanket green light to the capital relief deals.

The International Association of Credit Portfolio Managers estimates that there were 89 SRT transactions globally last year for loans worth a total of €207bn. Approximately 80 per cent of them were corporate loans, with the rest comprised of debt such as subscription lines, car loans and trade finance loans.

While credit facilities to private equity form a small part of the SRT market, they have grown popular because they are considered relatively safe.

“The thing with subscription lines is that it’s an asset class that has no loss historically,” said Frank Benhamou, risk transfer portfolio manager at Cheyne Capital. “They tend to be tightly priced, so investors who engage in this trade often use a bit of leverage to enhance returns.”

Through SRTs, Blackstone is exposed to the risk that large investors such as pensions and sovereign wealth funds refuse to meet the capital calls when the loans mature, typically within a year. An investor could run low on cash, or face complications such as sanctions or fraud.

While no limited partners have ever defaulted on their obligations, including during the 2008 financial crisis, potential buyers have baulked at the lower diversification of subscription lines, compared with corporate loans.

“Though we accept that the credit risk is low for subscription lines, there’s a risk we can’t quantify and price,” said one investor who has been in the SRT market for more than a decade.

The pool of loans for subscription lines is smaller than more traditional asset classes so the “idiosyncratic risk is the sensitivity of your return to one party . . . and there’s higher risk of fraud which is difficult to price”, they added, referring to the limited number of private equity funds that they would be exposed to.

Another SRT investor pointed out that in a typical subscription line transaction there are somewhere between 10 to 30 funds, which creates more concentrated risks.

The rise of these debt products has also revived fears of unforeseen chains of events, with bank analysts and some policymakers debating whether the banks selling the SRTs have fully protected themselves. In the April earnings call, Evercore ISI analyst Glenn Schorr asked Blackstone’s Gray whether the explosion of SRTs carried hidden risks, like during the global financial crisis.

This type of deal “gives us shivers, reminds us about 16 years ago”, said Schorr, referring to off-balance sheet entities banks used in the crisis era to relieve their overburdened balance sheets. Gray said the firm was doing the transactions in a “responsible way”.