In Changsha, the capital city of Hunan province, Yang has just finished his morning flute practice by the lake next to his apartment. Over his seven decades he has lived in five different housing compounds, but says this one, with its greenery and nearby high-speed rail, is the best.

Yang, who declined to provide his full name, bought into the Changsha Evergrande Oasis, one of many developments in the region, for Rmb615,000 ($85,000) in 2009. A year later, after his apartment was finished, he and his son’s family moved in.

Although the name has since become synonymous with the rise and fall of Chinese real estate, at that time he knew “nothing about Evergrande” or “where its money came from”.

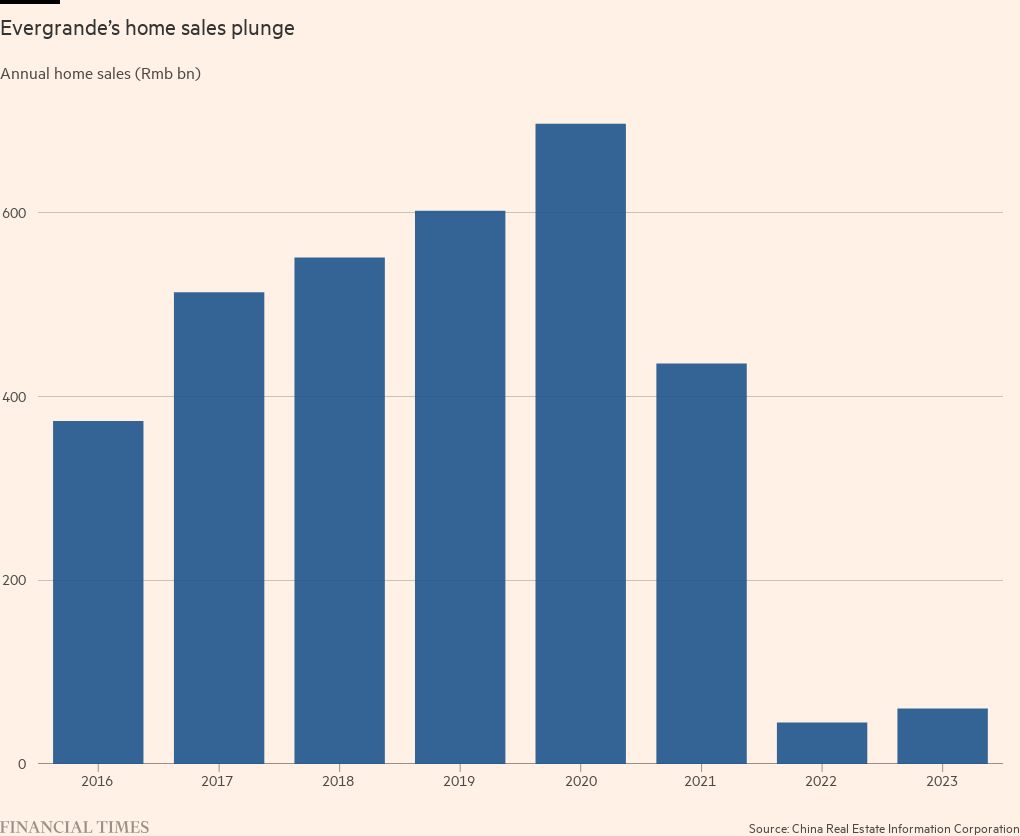

The company was by then expanding rapidly. The year Yang moved in, Changsha Oasis brought in Rmb1.7bn ($230mn) in sales. In 2011, when Evergrande issued over $1bn of bonds settled in dollars to overseas investors, its offer document mentioned the project nine times.

The document, which offers the most comprehensive insights into Evergrande’s funding mechanisms, bore the logos of western investment banking giants such as Bank of America, Deutsche Bank and Citi alongside that of state-owned Bank of China International. More pertinently, they promised coupons of up to 9.25 per cent — a highly attractive return in a post-crisis world of near-zero interest rates.

It was part of a wave of bond issuance that funnelled tens of billions of dollars from western financial institutions, and the savers ultimately behind them, into China’s real estate boom.

Endorsed by Wall Street’s finest and often issued via Hong Kong, with its westernised legal system and investor protections, they represented a financial bridge between China and the wider world. But they offered none of the security usually associated with debt instruments when boom turned to bust.

The 2011 bonds fully matured in 2016, but many more recent issues with similar characteristics are now close to worthless. They are being fought over by lawyers and restructuring experts, and picked over by speculators hoping to salvage some returns via a Hong Kong insolvency process.

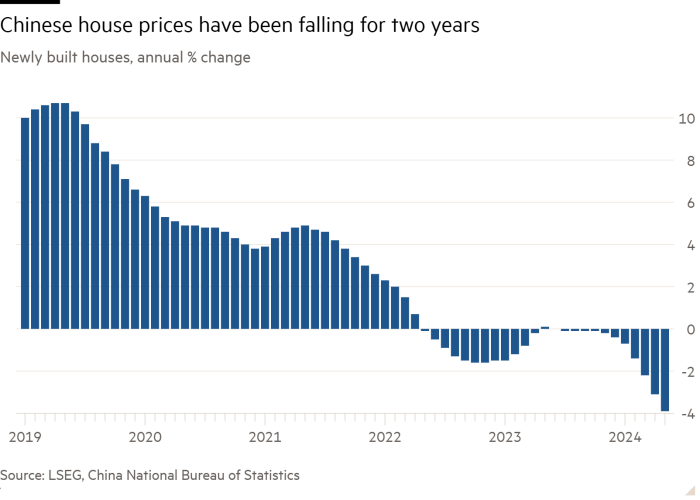

Almost three years after Evergrande first missed payments to offshore investors, China’s real estate industry is still struggling. Beijing has refused an overt bailout but has permitted local authorities to buy unsold housing. Many of the projects launched by mainland developers are unfinished, and in some cases under the control of provincial bureaucrats rather than the overseas investors who helped to fund them. In Hunan, local government late last year identified 45 unfinished Evergrande projects alone.

Dozens of investors in Evergrande bonds, the structure of which is rarely discussed outside specialist circles, declined to comment to the FT, as did the banks.

Their rise and fall sheds light on the profound differences between mainland China’s financial, legal and political systems and those of the wider world, and raises questions over how capital will flow between the two in future.

“The international investing community wanted to be part of the great real estate boom in China, and the Chinese real estate companies recognised this was an avenue to generate liquidity . . . in some senses it was a match made in heaven,” says one restructuring specialist.

“Everything was premised on the assumption that the real estate market would continue to rise.”

Before Evergrande listed its shares in Hong Kong in 2009, it was already drawing on money from outside China. One former investor, who spoke on condition of anonymity, participated in a private debt placement that raised over $500mn in the mid-2000s.

At a creditors’ meeting, he recalls discussing one of the projects that had been earmarked for the funds. It was supposed to be completed in three to five years, but someone had visited the construction sites and found there was “nothing going on”. Money, however, “was flowing out of the account”.

The investors’ money was released from a mainland bank account after the company provided invoices stamped with an official seal. But “you couldn’t find who had signed it off,” the investor says. “They might say, you know, five tons of steel, but five tons of steel for what? It doesn’t matter, it’s five tons of steel.

“What became evident was [the money] was raised against certain projects, but wasn’t necessarily spent on those projects,” he concludes.

In Hong Kong, the perils of trying to account for mainland assets and liabilities were well known after a wave of often speculative state-owned companies listed there in the 1990s.

“They were effectively towns,” says one person involved in some of the earliest listings, referring to the range of municipal assets such entities often controlled. “As much as possible, we tried to get them into the international model.”

A private property market had essentially been recreated in the same decade in China, and by the 2000s it was a leading driver of economic growth. But, wary of the risks of an overheating property sector, Beijing was already starting to rein it in.

A 2007 circular issued by the People’s Bank of China prohibited commercial banks from lending to any developers “found to be hoarding land”, Evergrande said in its bond documents. In the same year, Safe, part of a regulatory apparatus controlling capital flows in and out of China, said it would no longer process foreign debt registration for real estate purposes.

As a result, Evergrande relied on a structure common across many other emerging markets. Bonds were sold to international investors by a specially created vehicle outside of China, often in the British Virgin Islands. That entity sent the money it raised into China mostly in the form of equity investments in subsidiaries — and relied on the equity dividends from those subsidiaries to meet obligations to its own investors.

Lawrence Lu, a director at S&P in Hong Kong, says the rating agency has referred to this phenomenon as “structural subordination”, a term also used in developed markets when holding companies issue debt that may have limited claims on the assets of its subsidiaries in the event of default.

“Even in western markets, once you raise money, money is fungible,” he says. “Once they raise the money, they use [it] as equity to project companies. Where the money goes, it’s outside of our expertise.”

Offshore instruments of this kind helped to fund companies such as Changsha Tianxi Real Estate Property Co, the developer of Changsha Evergrande Oasis. A chart in Evergrande’s documents shows dozens of subsidiaries, with a dividing line separating those within mainland China from those outside.

The foreign flows were not Evergrande’s only source of financing, but they helped to kick-start presales payments from homebuyers like Yang, which could then be invested elsewhere. On its opening day, the Changsha Evergrande Oasis brought in over half a billion renminbi in such downpayments. Across 62 Evergrande projects in total in that year, a total of Rmb50bn was brought in.

The investor in the private placement says that similar transactions were typically arranged by investment banks ahead of equity IPOs, which in turn were priced based on the value of the developer’s land holdings. That gave banks “an incentive to encourage developers who wanted to list to grow their land bank and show they could sell projects”.

It was a “fee machine”, the investor adds; fees from the pre-IPO bonds, the IPO itself, and then high-yield bond issues after that. The developer’s presence in Hong Kong, meanwhile, “gave it the veneer of ‘you’re covered by Hong Kong law and it looks like a normal bond’.”

But in his view, that was “an illusion”. He adds: “They were always going to be the part that didn’t get paid.”

When Evergrande stopped making interest payments to overseas investors in late 2021, it was the first clear sign that something was seriously awry with China’s property model. But since then, the fate of its bonds has faded from public discussion.

A two-year restructuring negotiation, led by lawyers at Kirkland & Ellis and investment bank Moelis in Hong Kong and largely focused on its listed subsidiaries outside China, produced no deal with creditors. Moelis declined to comment. Kirkland & Ellis did not respond to a request for comment.

A court in the city issued a winding up order for Evergrande’s Hong Kong entity but it has limited legal significance unless it is recognised by courts in mainland China. Even then, the investors’ ultimate claims are typically equity stakes in projects in China owned through a web of subsidiaries.

Evergrande also did not respond to a request for comment.

When it defaulted, Evergrande had over $20bn of offshore bond debt in issue, held by investors such as BlackRock, HSBC and emerging market specialist Ashmore. Those that still had some exposure this year, according to Bloomberg terminal data, included UK insurer Legal & General and US hedge fund Saba. All declined to comment for this article.

Some investors spoke on condition of anonymity, including one investor at a major international firm. “It will be a very, very low price, like 0.0 something, depending on the market price of that day,” the investor says of the firm’s “legacy exposure” to Evergrande. “Over the past two years we have de-risked the sector significantly, but of course we cannot 100 per cent exit.”

The person adds that the investor community was “fully aware of the structure” and that there had been “long discussions” about the bonds in the past. But there was never “clarity” on exactly how cash moved from individual projects in China to the offshore vehicles that paid bondholders and the matter of legal obligations was “overlooked”.

No full list of bondholders is publicly available. But Evergrande “was in the portfolio of ‘tourist investors’,” says one person involved in the fallout, referring to those who would not normally invest in the region but made an exception for Evergrande because it was a well-known name.

Some hedge funds “decided, without knowing much, to pile in” when signs of distress emerged, expecting to be able to negotiate a profitable restructuring deal through a legalistic, US-style approach, the person adds.

Those investors have now “discovered what the lawyers already knew, that . . . it wasn’t going to be easy to enforce and it would be time-consuming and expensive, with a limited prospect of recovery.”

Claims against those who underwrote the bonds are complicated by international norms, which see fixed-income instruments as much safer than equity. Guiping Lu, a lawyer at Mayer Brown specialising in capital markets, says investors in the US seeking redress need to prove that private bond underwriters ignored clear red flags rather than simply provided inaccurate information. That is a higher burden of proof than in more regulated equity issuance. “If you want to sue the [debt] underwriters, you need a legal basis,” he says. “What is the legal basis?”

“We have been holding the view [that] it’s not worthwhile to get involved in the recovery process,” says another investor. “Bankers and lawyers need to sit down and come up with a better structure [for future issues],” he adds.

Such discussions may have to wait until conditions in the real estate sector improve, he predicts. “The market, in the form of what we had in the past almost twenty years . . . it’s gone.”

Online searches suggest that all 76 of the real estate projects mentioned in Evergrande’s 2011 bond documents have been completed.

But at a former Evergrande scheme a few miles away from Yang’s morning flute recital, construction has been suspended for three or four years and a crane is about to be removed. “The money has not arrived,” says one employee of a state-owned company that has taken over.

At another development, a member of staff has just completed sales of all of the apartments in the block. He used to work for Evergrande, attracted by the prestige of the company and the staff discounts, but now his wages are paid by the government.

At a third, closer to the city centre, a woman holding a baby is anxiously checking in on an unfinished project launched by Evergrande but since taken over by a state-owned developer.

For Beijing, homeowners like these who have not yet received their properties are the priority. Their downpayments acted as lending to the system and their claims are part of a wider social contract.

Evergrande’s accounting for its revenues inflated them during 2019-2020, according to China’s financial regulator, which in May imposed a Rmb4.2bn fine on the group’s mainland entity and accused it of fraudulent bond issuance, over debt issued within the country rather than offshore. Evergrande’s auditor, PwC, has also come under scrutiny. PwC declined to comment.

But individual projects were often audited at a local level: the subsidiary behind Changsha Evergrande Oasis was audited by the Hunan Yuancheng United Certified Public Accountants Office, and 2011 documents list dozens of other similar local accountants.

Compared to the 2011 bonds, future debt issues leading up to Evergrande’s collapse provided less detail as to where a growing pool of money sourced from outside China was going. Meanwhile, dozens of Chinese developers listed in Hong Kong have defaulted on their debts, though some have shown signs of being able to restructure outside of China.

“I don’t think any of us thought it would be a Chapter 11-style process,” says one investor in the bonds of several mainland property developers, referring to the established US insolvency mechanism. “But we thought there was a capital structure in China.” He describes his holdings, which he hopes to negotiate some recovery on, as “subordinated equity”, a far more junior entity than a bond secured on real assets.

Evergrande’s financial instruments were shaped by a system that retained strict capital controls to obstruct overseas investment, but which was at the same time hosting the biggest property boom in history.

Future foreign investment into China, whatever its structure, will have to assess the unfolding realities of a property bust that has, according to Goldman Sachs estimates, left China with Rmb30tn of unsold housing.

On the edge of Changsha, in the vast ruins of an unfinished theme park that was once part of Evergrande’s empire, there is only one person on site. He is taking a break from a separate project nearby to fish in what remains of a boating lake.

“There are enough houses for four billion people in China nowadays . . . I read that number online,” he says with a grin, as he throws a fish into a nearby bucket. But, like many of those left holding Evergrande’s bonds, “we’re not really all that clear”.