Stay informed with free updates

Simply sign up to the Financial services myFT Digest — delivered directly to your inbox.

Earlier this week MainFT reported that hedge funds are griping that their fundraising efforts have been hurt by how much money investors have locked up in private capital funds — that aren’t distributing any returns.

As Michael Monforth, global head of capital advisory at JPMorgan Chase told our colleagues:

The lower rate of distributions from private equity, [private] debt and venture funds is having a knock-on effect, leading some allocators to pause on new investments into illiquid funds and reduce new investments in more liquid hedge funds.

This made FT Alphaville curious though: just how big is the gap between the money called up by private capital firms, and the realised returns they’ve actually recycled back to investors? So we asked Preqin for the data, and, friends, it is absolutely massive.

Private capital firms have taken more money from investors than they’ve distributed back to them in gains for six straight years, for a total gap of $1.56tn over that period.

And this isn’t just about the recent glut of capital raised, lagged returns and private equity exit blockages either. Even if you include the big returns of 2013-2017, private capital funds have now called $821bn more than they’ve returned over the 14 years that Preqin’s data series stretches over.

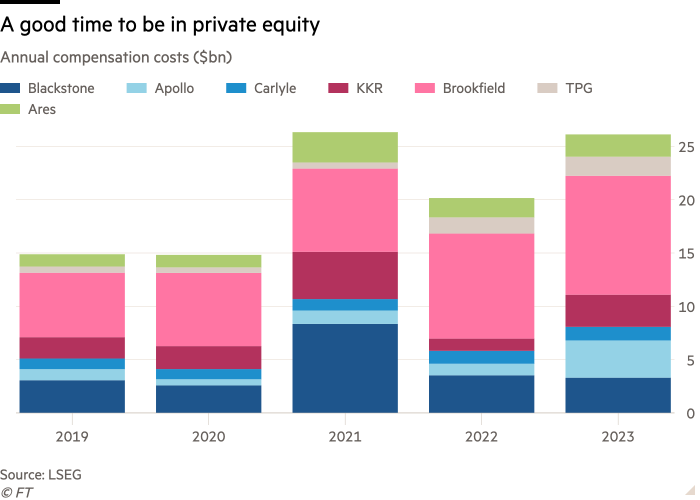

You might think that in a ruthless, meritocratic industry like private capital, this might have had an impact on compensation? Ahahaha no, of course not you sweet child.

FTAV looked up the labour and stock-based compensation costs of the of the largest listed North American private capital players, and they’ve totalled over $100bn over the past five years.

There’s a reason why Oxford finance professor Ludovic Phalippou referred to the industry as a “billionaire factory” in a prominent 2020 paper examining the returns of private equity.

American PE funds raised $1.7 trillion between 2006 and 2015, generated $230 billion of carried interest, and delivered to investors an overall net performance equal to that of stock indices and small-cap mutual funds). Most of this money goes to the largest PE firms and within the largest PE firms most of the money goes to a few partners, often the founders. At least, this was the model until a few years ago. First, the largest four PE firms went public in the late 2000s. Since then, the Carry they earn (as well as other fees) has been distributed to their shareholders (including the founders). Next, over the last few years, some PE funds have bought stakes in privately held PE firms and thereby paid the existing shareholders (mainly the founders of these firms) a large amount of money in order to gain access to a share of their future stream of fees and Carry. These transactions resulted in many PE firm founders becoming multi-billionaires. Many founders who did not sell part of their PE firms are also probably multi-billionaires as well but have not realized that value and are therefore not showing up in multi-billionaires rankings.

Of course, these things do move in cycles. There are naturally years where more money will be raised than returned. And perhaps the trillions raised over the past 4-5 years will eventually gush back manyfold to investors over the next decade.

But the fact that private equity alone is sitting on a record backlog of 28,000 companies worth an estimated $3tn at a time when most equity markets are at or near record highs doesn’t fill one with confidence. There’s a reason why PE and VC fund stakes are being sold at often steep discounts.

There just seems to be too big a mismatch between what private equity and venture capital have paid for a lot of assets, the returns their investors expect, and what public markets or other potential buyers are willing to pay.

And as long as that remains true, there’s going to be a long and hard case of investor indigestion to deal with. NAV loans can only take you so far, after all.

Further reading:

— Is private equity actually worth it? (FTAV)

— Revisiting private equity valuations (FTAV)

— The private capital industry’s ‘dry powder’ has hit $4tn (FTAV)