Where the crunch on property funds could be felt in Europe

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Property investor Sam Zell once said that there is no value without liquidity. A growing queue of US investors are waking up to that reality in commercial real estate. Unlisted Starwood Real Estate Income Trust, with $10bn of assets, was forced to limit redemptions during the first quarter.

On the other side of the Atlantic, hard-learned lessons offer some comfort if the turmoil travels.

Illiquid property assets in liquid fund structures seem a fine idea while prices are stable or rising. Cash from new investors means plenty is available for anyone who wants out. When markets sour that equilibrium evaporates. Buildings can take years to sell while investors can ask for cash on demand. Funds in that situation have three unpalatable choices: sell assets quickly into falling markets, raise debt or halt redemptions.

After multiple UK property funds were forced to stop withdrawals following the 2016 Brexit vote and in the pandemic, the open-ended sector is much diminished. Assets under management have fallen by around half to €13bn today, according to Morningstar.

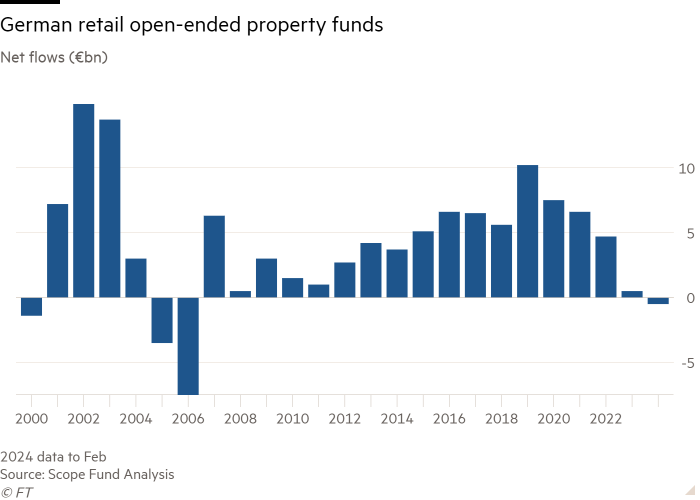

That figure is dwarfed by the sums sitting in open-ended funds in Germany — where property markets are among the most troubled in Europe. About €120bn of retail property investment sits in similar open-ended fund structures in the country. Some €0.5bn of money on a net basis was pulled in the first two months of this year, according to Scope Fund Analysis. With the sector experiencing its first meaningful net withdrawals since 2006, protections put in place back in 2014 may be tested.

Those regulations meant that new investors had a 24-month holding period. Funds also have a 12-month grace period to meet redemptions from those investing since 2014. One disincentive to withdrawing money is that valuations are taken at the redemption date, not when it is requested. This is supposed to make liquidity management easier. Nonetheless, outflows are expected to rise, peaking in the third quarter of this year, thinks Scope’s Sonja Knorr.

Liquidity remains robust with €17.3bn or 14 per cent on aggregate — well above the 5 per cent minimum. Average loan to value of 16 per cent is also half regulatory requirements.

Open-ended property funds for institutional investors could pose a greater risk. They are less regulated, more opaque and contain €180bn of property assets owned by German pension and insurance assets. Redemptions are rising too. Liquidity and LTVs are largely undisclosed but exposure to offices is substantial.

This is a waiting game. Investors who are short of cash are holding out for interest rate cuts. But sharp declines are not a given. The selling pressure could intensify this year.