The CRE non-crisis rolls on

This article is an onsite version of our Unhedged newsletter. Premium subscribers can sign up here to get the newsletter delivered every weekday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Good morning. The latest in a series of weak Treasury bond auctions seems to have been the cause of rising bond yields and falling stock prices yesterday. The gloomy mood was broken by Chewy, which sells pet food online. Its shares rose 27 per cent on strong earnings. Good boy! Email me a picture of your dog: [email protected].

Bank OZK and the continuing CRE non-crisis

Bank OZK is a regional bank with $36bn in assets, known for its high exposure to commercial real estate. Yesterday, the shares fell 14 per cent after a Citigroup’s regional bank analyst, Benjamin Gerlinger, downgraded the stock to sell.

After a 500 basis point increase in interest rates, we are doomed to endure a drip-drip of bad news from the highly leveraged real estate sector, whether it be analyst downgrades or news of defaults and fire sales. With each drip, the question will continue to be asked: is the long-awaited and much-delayed CRE crisis finally here? Barring another leg up in interest rates, the answer will continue to be no. There are several reasons for this. The worst of the problems are confined to multi-tenant office buildings in large cities; most banks have moderate exposure to the worst of CRE, and have taken reserves for it; there are plenty of lenders out there willing to help owners in trouble, in creative ways.

Here is the summary paragraph of the Citi note:

We have newfound, but substantial concerns with what we believe to be OZK’s largest individual loan (totalling $915mn), a multi-use project in Atlanta (“Echo Street West”; $135mn loan), and Life Science construction lending in general (which is largely idiosyncratic to OZK vs peer banks). Together these two loans account for 3.8 per cent of non-purchased loans; 8.1x larger than the entire [allowance for credit losses] for construction loans.

The largest loan is to a 5-building, 1.7mn square foot, $1.5bn commercial development in San Diego, designed for the life-sciences industry. Citi believes that, after four years of development, none of the space has been leased. The space is simply too big, and both the region and industry are oversupplied, the bank thinks.

I have absolutely no idea if Citi is right about OZK’s big loan, but the picture it paints is consistent with other cases of perceived and real bank distress. Higher rates have made life hard for banks with concentrated loans into areas that are also under stress for reasons other than rates. The obvious analogous case is New York Community Bankcorp’s concentrated exposure to rent-controlled residential real estate in New York City. But there is still little evidence of a waterfall of loan distress in CRE in general.

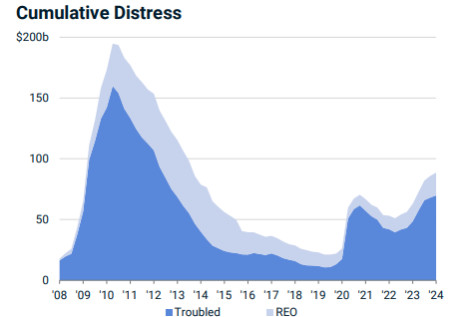

The aggregate delinquency rate on US banks’ CRE loans remains below 1.2 per cent as of the first quarter, according to the Federal Reserve. A chart from MSCI Mortgage Debt Intelligence sums up the situation well. It shows the total value of commercial real estate loans MSCI classifies as “troubled” — either in default or bankruptcy or with some other publicly reported issue. “REO” indicates that the banks have ended up owning the underlying property:

In addition to the $88bn in troubled properties, MSCI thinks there are another $205bn in loans in “potential distress” because of “events such as delinquent loan payments, forbearance and slow lease up/sell out”. Yes, the trend does not look great, but the $293bn combined total compares to almost $3tn of total CRE loans held by US banks, again according to the Fed, and of course many CRE loans are not held by banks. Look at it this way: if all of those troubled and potentially troubled loans were held by banks, and there were all to default, with a recovery rate of just 50 per cent, that would only destroy about 6 per cent of US banks’ equity capital.

Individual banks will suffer, or course, as they already have, and the suffering will go on for years if rates do not come down from here. As Jim Costello of MSCI pointed out to me, there are plenty of large city office buildings that have seen their values cut by half. This means meaty losses for banks even in cases where loan-to-value ratios were reasonable.

But anyone waiting for the situation to blossom from a painful grind into a contagious crisis should probably stop waiting. Brian Foran of Autonomous Research pointed out that, for example, Wells Fargo’s commercial banking division has taken reserves against its CRE portfolio equivalent to 11 per cent of its total loans. That means that it has made provision for a situation where 20 per cent of its loans default, and the recovery rate on those loans is just 50 per cent. Is every bank as well reserved as Wells? Surely not. But the system as a whole looks like it can handle the pain that is coming.

ROE and the new economy

In yesterday’s newsletter I discussed one theory about why valuation multiples on US stocks have risen over the past three decades. It is due to a change in the structure of the corporate economy, shifting to more technology- and service-based business models that are less cyclical and less capital intensive. The result is higher returns on investment, which justify higher multiples.

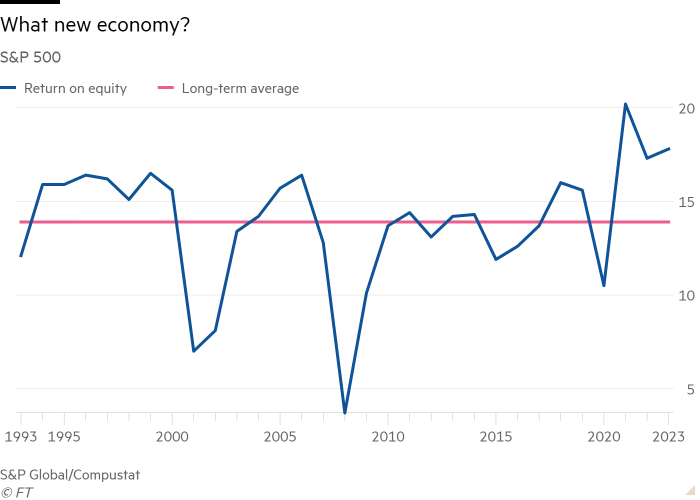

The argument is coherent, but is it empirically true? One slightly confounding fact is that return on equity for the S&P 500 does not seem to have been on a rising trend over the past 30 years. Chris Mowbray from S&P Global Market Intelligence sent me the data below. He calculates ROE as income available to common shareholders divided by common equity:

There appears to be a post-pandemic leap in profitability, but no long-term upward trend here that would explain the long-term rise in valuations. Perhaps looking at return on invested capital, a broader measure, would help? Here ROIC is defined as income available to common shareholders divided into the sum of debt, preferred stock, non-controlling interests and common equity. The story is the same as for ROE:

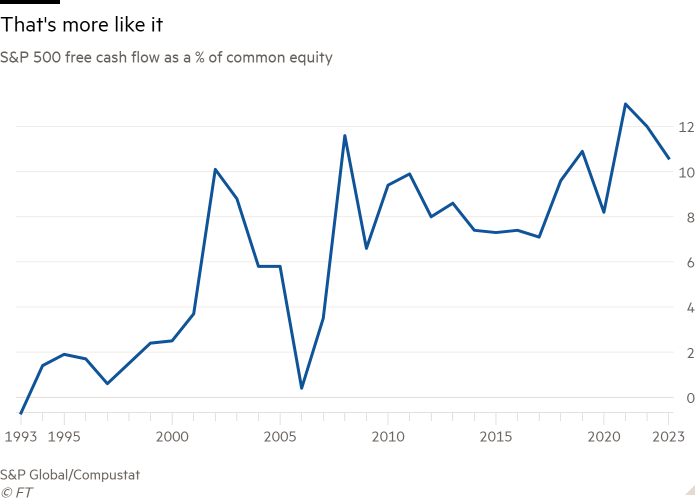

This does not mean the “new economy” theory of higher US valuation multiples has been disproved. It does however mean that the theory’s fans have some explaining to do. There may be a better way to cut the data, for example. Here’s an evocative series: free cash flow as a percentage of equity, a sort of rough free cash return on equity. It does look like there is an upward trend, so maybe the smoothing adjustments that go into calculating net income are obscuring something that is visible in cash flow:

This is suggestive, but the basic challenge remains. Those who justify paying twice as much for stocks on the basis of a transformed economy must show compelling evidence that the corporate economy — not just a handful of companies — has been transformed.

One good read

The baby bust.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Recommended newsletters for you

Swamp Notes — Expert insight on the intersection of money and power in US politics. Sign up here

Chris Giles on Central Banks — Vital news and views on what central banks are thinking, inflation, interest rates and money. Sign up here