Wall Street bankers are eagerly anticipating that a rebound in dealmaking activity will raise bonuses and morale after more than a year in the doldrums, but fear that a return to the industry’s 2021 peak remains a long way off.

Even for a business such as investment banking marked by feast-to-famine swings, the past four years have been extreme.

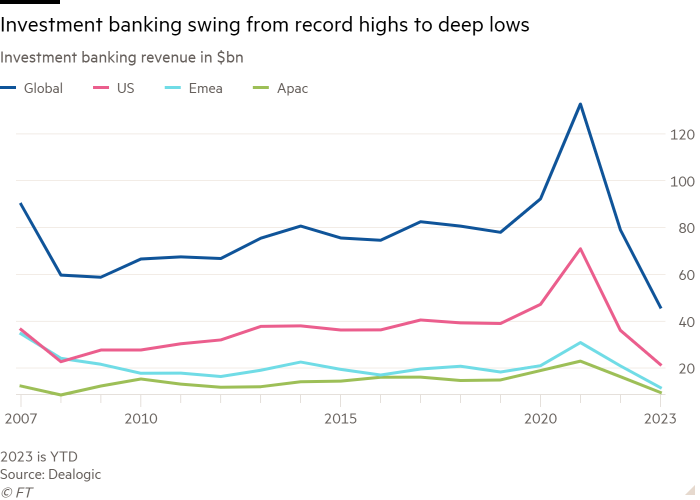

Fees at the likes of Goldman Sachs, JPMorgan Chase and Morgan Stanley on corporate mergers, equity raises and debt underwriting surged in 2020 during the coronavirus pandemic and hit record highs in 2021. But investment banking activity plummeted in 2022 when central banks began aggressive campaigns to raise interest rates.

“People are trying to just get a handle on what a fee pool could look like,” said Glenn Schorr, banking analyst at Evercore.

After Wall Street paid record year-end bonuses in 2021, data from the New York state comptroller showed payouts last year fell at the sharpest rate since the financial crisis on the back of a 95 per cent drop in the amount raised in US initial public offerings and a 40 per cent decline in the value of US deals.

That slide has continued into 2023, with investment banking fees falling to their lowest in more than a decade.

A string of recent deals is feeding optimism that 2024 will be a turning point for the industry, with idle bankers put back to work again. In September, Arm’s blockbuster Nasdaq listing marked a $105mn payday for the chip designer’s underwriters, while Cisco’s $28bn acquisition of software maker Splunk should also prove lucrative for the companies’ advisers.

The new normal is unlikely to look like the extreme boom-and-bust cycle of the past four years, according to executives. Instead, they point to the period immediately before Covid-19 hit as the reference point for budget and staff levels.

“For the foreseeable future, 2021 is probably not the near-term [model],” said Dan Dees, co-head of global banking and markets at Goldman. “The new normal is at a premium to 2018, 2019 level. It is correlated to market [capitalisation] and GDP, and those are all at higher levels.”

The last time the industry faced a similar whipsaw in activity was during 2007 to 2009. It took more than a decade for investment banking revenues to return to their pre-financial crisis high-water mark.

Like the reshaping of the industry that occurred in 2008 with the collapse of Bear Stearns and Lehman Brothers, this year has brought significant upheaval in the sector with the sale of Credit Suisse to rival UBS and new leadership at Barclays prompting a number of exits from the British bank.

Some banks are taking that as an opportunity to seek a greater foothold in the industry.

On Wednesday, New York-based Jefferies said it was aiming to expand its ranks of managing directors from just over 200 in 2020 to more than 360 by 2024, despite investment banking revenues for the three months to the end of August falling 2 per cent from a year earlier.

“It’s primarily a bet on our ability to win market share,” said Brian Friedman, president of Jefferies.

The bank’s larger rivals Goldman, Morgan Stanley and JPMorgan all report third-quarter results in October, when analysts will be watching for signs of activity picking up.

Bankers expect the typical pattern where fees — usually calculated as a percentage of deal price — increase gradually in line with the economy and companies’ market capitalisations to resume.

“We expect the global investment banking wallet to normalise in the $80bn-$90bn range, a little bit above 2019,” said Fernando Rivas, who retired in September as JPMorgan’s head of North American investment banking after three years.

Companies seeking to bulk up and newer businesses in artificial intelligence, healthcare and software that need to go public could drive a recovery in fees.

A further spur would be a rebound in activity by big private equity groups — a large source of investment banking fees since the financial crisis, but which have largely kept their powder dry in the past 12 months due to rising interest rates and an uncertain economic outlook.

“Sponsors have been a little quieter recently because of the macro uncertainty but they’ll come back,” Rivas said.

Still, some fear that recent action by central banks to aggressively lift the cost of borrowing risks dampening merger activity and preventing a return to the dealmaking boom of the past 15 years.

“We have had 10, 15 years of very low interest rates,” said Christian Bolu, banking analyst at Autonomous Research. “You could buy anything with cheap debt and make it accretive. It makes sense that there’s going to be some sort of negative impact from [higher rates].”

With the US making up about 50 per cent of global investment banking fees, according to Dealogic data, the muscular antitrust approach from the Biden administration and the Federal Trade Commission under Lina Khan is a source of further worry for dealmakers.

Although Khan, chair of the FTC, has lost several high-profile antitrust cases since taking the job in 2021, bankers fear her broader resistance to mergers risks having a chilling effect. Last week, the FTC brought its first antitrust lawsuit under Khan challenging roll-up acquisitions by private equity groups.

But even with that, bankers are predicting there will be enough deals to go around to make for a rosier 2024.

“Antitrust is probably the biggest dampener [on M&A],” said Jefferies’ Friedman, “and that is only applicable to a small number of categories. The positive forces overwhelm that.”

Additional reporting by Laura Noonan