Hello and welcome to the latest edition of the FT’s Cryptofinance newsletter. Scott’s away this week so you’ve got me, and I’m taking a look at the crypto-laden tension between the UK’s banks and its politicians.

One thought to start: everyone in crypto is waiting to see if and when the SEC will approve a spot bitcoin ETF. Decisions are due by mid-October but the threat of a US government shutdown looms. If SEC staff are furloughed for a long period then decision deadlines, including on BlackRock’s landmark ETF, may get pushed back again. What do you think? Email me at [email protected]

If you live in the UK and want to trade crypto, which bank do you use to transfer money to your preferred exchange?

Definitely not JPMorgan’s Chase UK. The British arm of the Wall Street bank this week made it clear that it would ban customers from buying and selling crypto from mid-October, becoming the latest lender operating in the UK to restrict its customers’ crypto activities.

Its name can be added to a list that includes TSB and Starling, which have long banned crypto transactions. Other lenders, such as high-street names Santander, Nationwide and HSBC, have daily and monthly limits on how much a customer can spend at a crypto exchange, in an attempt to curb traders punting all of their money (in one go).

Chase UK pointed to crypto-related fraud losses behind its decision. Still, its move highlights the precarious path that companies around the world are treading as they try to navigate their way through crypto.

On one hand, the UK is one of the world’s biggest financial centres and prime minister Rishi Sunak has been a leading proponent of making Britain a global “crypto hub”. To that end, the government has been trying to cultivate an “open for new business” image.

On the other, Chase is a private company that can make its own decisions about the business it accepts — or rejects. Plus, it must comply with a tower of banking regulation.

Preventing fraud is one of those regulations. According to reporting agency Action Fraud, crypto-related fraud losses jumped more than 40 per cent in the year to March 2023 and crossed the £300mn mark for the first time. That total includes not only cyber crime but also the collapse of FTX, which triggered a wave of losses among retail investors.

Chase UK openly said that “declining these [crypto] payments is one of the ways we’re helping keep you and your money safe”.

Still, that disconnect matters. Chase UK’s outright crypto outlawing drew the ire of none other than Brian Armstrong who called it “totally inappropriate behaviour”. The Coinbase chief executive called out Sunak and City minister Andrew Griffith, saying: “It appears @Chase UK does not respect your policy goals — thoughts?”

Totally inappropriate behavior from @Chase UK (this is their UK bank only is my understanding)@RishiSunak @griffitha It appears @Chase UK does not respect your policy goals – thoughts?

UK crypto holders should close their @Chase accounts if this is how they’re going to be… https://t.co/n8OBxhtpcg

— Brian Armstrong 🛡️ (@brian_armstrong) September 26, 2023

The head of one large crypto investment firm echoed that view, telling me: “If I’m the UK [government], I’m not really thrilled with this.” They added: “I have awesome conversations in the UK with senior policy officials. I have less awesome conversations with the FCA . . . there’s probably a schism of sorts between the FCA and the policymakers.”

While Chase UK’s move has brought my small island nation into sharp focus, the predicament is the same for all the big financial centres of the world, through which real institutional money flows. That’s places like the US, Hong Kong, Singapore and the EU.

Politicians are keen to open up their countries to new technologies, appeal to entrepreneurs and appear forward-thinking, but those breezy slogans are undermined by regulated institutions — and existing regulations.

For example, Revolut remains a major player allowing crypto transactions in the UK, but is having problems filing accounts and securing a banking licence.

Regulators and reputation-conscious CEOs aren’t too pleased with the crypto industry and the vast fraud that so far has come with it, and are ultimately preventing the full-scale crypto adoption that many desire.

Here in the UK things are about to get a bit tougher. In just over a week, new rules come into force that clamp down on freewheeling crypto marketing and ban “refer a friend”-type promotions, among other things. Bybit, the crypto exchange, has blamed the change for its decision to pull out of the UK.

All of this highlights the difficulty that Westminster politicians face in building London into a free-spirited crypto hub, as they are walled in by highly regulated banks and financial regulators.

Further underscoring the difficulties this situation presents, Charles Randell, former chair of the Financial Conduct Authority, told a recent conference that Westminster had exerted pressure on the regulator to burst open its doors to crypto firms, the Guardian reported.

“In the context of crypto, in my experience as FCA chair . . . there was a lot of political pressure to welcome firms, some of which are now under criminal investigation by the US Department of Justice,” he said, adding that “all the evidence that we had at the FCA was that wasn’t a very good idea”.

On the eve of the trial of FTX’s Sam Bankman-Fried, it’s understandable why cautious regulators might feel vindicated.

But this issue isn’t going away. Until eager politicians can put their enthusiasm for crypto into rules, private companies will continue to do it instead.

Weekly highlights

-

Binance sold its Russia business to a one-day-old crypto exchange called CommEx. As the FT’s Moscow bureau chief wrote, seems legit.

-

Also on Binance, the WSJ took a look at the meltdown at the world’s biggest crypto exchange, which is encircled by US regulators, losing market share and senior employees.

-

Hong Kong’s desire to attract crypto companies has come into sharp focus amid the alleged fraud at exchange JPEX and the arrest of some staff. The city’s crypto-friendly plans are being put to the test.

-

Kraken is planning to offer trading in US-listed stocks and ETFs, stepping beyond pure crypto trading, as per Bloomberg.

Soundbite of the week:

“If I were to purchase a Pokémon card, is that a security transaction?”

That’s what Ritchie Torres, a congressional representative for New York, asked Gary Gensler, head of the SEC, this week. Gensler was on the Hill for a meeting of the US House committee on financial services, which assesses the oversight of the agency and grills its leader.

The answer, in case you’re wondering, is no — but Gensler admitted that the purchase of a tokenised Pokémon card might be classed as a security.

(And if you’re thinking of making a Pokémon investment, here’s a fun deep dive into the economics behind the franchise.)

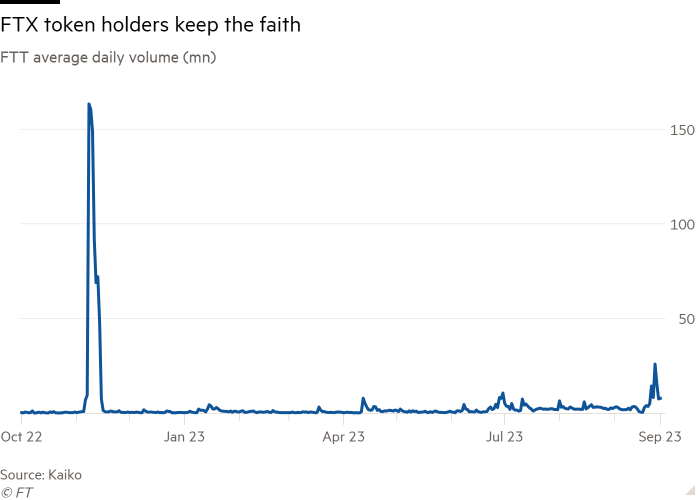

Data mining: The part of FTX that lives on

After countless confusing explanations and apologies, court filings, family profiles and an incarceration for alleged witness tampering, it’s finally here: Sam Bankman-Fried’s trial to answer seven criminal charges, including alleged fraud and conspiracy, starts on Monday in New York.

And yet, part of FTX still lives! Some traders are still buying and selling FTX’s token FTT, potentially hopeful that the administrators, led by John Ray, will resurrect the exchange from the wreckage.

As for the trial, expect it to last at least six weeks. Whatever the outcome, it will probably serve as a warning to others.