Receive free Cryptocurrencies updates

We’ll send you a myFT Daily Digest email rounding up the latest Cryptocurrencies news every morning.

Hello and welcome to the latest edition of the FT Cryptofinance newsletter. This week, we’re taking a look at Coinbase’s other regulatory troubles.

Coinbase is in a legal quagmire.

This week it filed its response to the Securities and Exchange Commission, which this month alleged the US-listed group had been running an unregistered securities exchange and offering unlisted securities. It’s a case that promises to define the American crypto industry. It’s a hefty 177-page read.

But another serious legal issue got lost amid the SEC headlines at the start of the month. Alabama state securities regulators also filed an order that gave Coinbase just 28 days to prove it isn’t selling unregistered securities in its state. After that it faces a cease-and-desist order.

It was filed on June 6 and was the result of a multi-state task force that comprised California, Illinois, Kentucky, Maryland, New Jersey, South Carolina, Vermont, Washington and Wisconsin. Come July 4, time is up.

Collectively, the states have locked on to Coinbase’s staking rewards programme, a common way to offer investors a return on their assets. Users lock their crypto in their wallet — on an exchange such as Coinbase — for a set period but give permission for that third party to stake their crypto on other crypto projects that offer interest or a yield.

One of the most popular ways is to put the staked asset to work helping to secure a large public blockchain, such as ethereum. The barriers to staking blockchains are quite high and users normally need to hold a lot of a particular cryptocurrency first. A pooled stake is one way to do it.

Depending on the coin and the risk involved, staking can earn an annual yield of between 4 and 17 per cent. The problem is that Alabama and others regard staking as an unregistered security.

Coinbase disagrees. It “firmly believes that our staking services in no way constitute securities under any state or federal law, and we intend to defend this important part of the cryptoeconomy”.

Coinbase has to fight each case state by state. It is in active discussions with five states that issued cease and desist orders, adding that extensions have been given to the company, according to a person familiar with the matter.

Other states that have started proceedings have only set Coinbase deadlines to show cause as to why its staking services are not securities and no one state is moving to enforcement next week, the person added.

But it underscores that there’s a lot at stake for Coinbase with staking. There are more than 3.5mn US Coinbase customers with a staking reward programme account. In the first quarter, turnover from the service was $74mn, about 10 per cent of total group revenue.

It also forms part of the company’s broader “subscription and services” revenue, which chief executive Brian Armstrong sees as a steady stream of income to guard against the unreliability of fees from trading volumes.

“In a world where Coinbase doesn’t offer staking, it will not be competitive against those who do,” said Ilan Solot, co-head of digital assets at London-based financial services group Marex.

But this issue goes beyond only a problem for Coinbase.

Staking customers’ tokens is at the heart of the security of networks such as ethereum. The blockchain is verified by so-called validators chosen at random. These validators — either individuals or companies such as Coinbase — stake tokens as a form of collateral against bad actors and are paid for it.

If one of the bigger, more reliable and transparent validators runs into trouble with its staking product and has to withdraw, that would change the balance of economic power.

It could concentrate the system in favour of fewer richer participants because the more coins a miner owns, the more mining power it has. Or the gap can be filled by bad actors, potentially corrupting it.

“Every centralised entity that runs into trouble with their staking programme is potentially chipping away at the security of the network . . . it can become less centralised,” Solot added.

What’s your take on Coinbase’s run-in with American state regulators? As always, email me your thoughts at [email protected].

Visit the FT Wilshire Digital Asset Index for round-the-clock updates on the crypto market, featuring data on price, circulating value and other key market metrics impacting industry’s most widely traded coins, including bitcoin and ether.

Weekly highlights:

-

While on the subject of state regulators, Nevada asked a court to appoint a receiver for Prime Trust, one of the few “crypto-friendly” US financial institutions with some regulatory approvals to operate in the traditional US banking and payments system. The state alleges that the custodian used customer funds to buy cryptocurrencies after losing access to digital wallets containing tens of millions of dollars in assets.

-

The National Bureau for Counter Terror Financing of Israel announced this week it thwarted an operation involving digital assets used to finance terror, headed by Hizbollah and the Iranian Quds Force. “This is not an easy task, which becomes even more complex when digital currencies are involved,” said Israel’s defence minister Yoav Gallant.

-

In the latest blow to Binance’s banking woes, Reuters reported that online payments service provider Paysafe said it would cease offering support to Binance customers across the European Economic Area. The platform is now working with Binance to “terminate this service over the next few months”. Earlier this year Paysafe said it would wind down services to Binance’s UK customers.

Soundbite of the week: Coinbase hits back at the SEC

As mentioned, Coinbase’s response to the SEC was hefty and sets up a head-on legal clash between it and the main US markets regulator. One notable point is that Coinbase is arguing it violates the US Constitution. It’s going to run and run.

“Even were the SEC correct that the assets and services it identifies are within the scope of its existing regulatory authority, this action must be dismissed on the independent grounds that it violates Coinbase’s due process rights and constitutes an extraordinary abuse of process.”

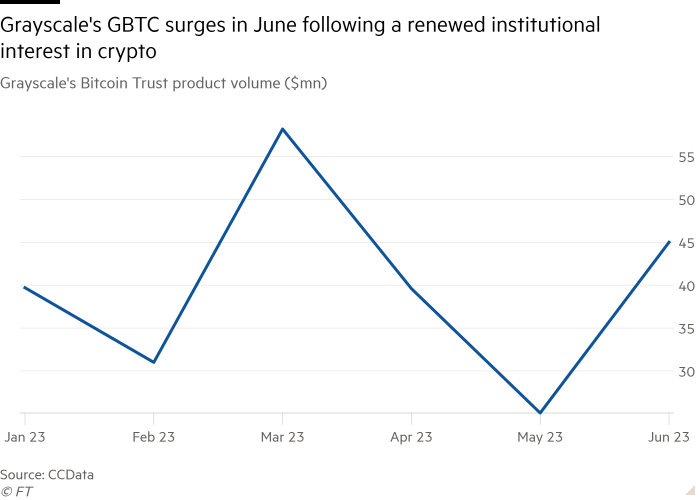

Data mining: Grayscale surges amid institutional excitement

Grayscale, manager of the world’s largest crypto fund, has had a good month.

The discount of the $13.5bn Grayscale Bitcoin Trust (GBTC) to its net asset value has narrowed sharply to a nine-month low of 29 per cent after BlackRock filed to list a crypto ETF. The market price is now $19.55 versus an NAV of $27.65, according to Bloomberg data.

If the world’s largest asset manager succeeds, it could open the door to a flood of publicly traded spot bitcoin ETFs in the world’s largest investment market.

Grayscale is suing the SEC for its refusal to allow it to convert GBTC into an ETF. If that changed the discount would probably disappear. Amid the excitement volume in GBTC has surged almost 80 per cent in June.

Cryptofinance is edited by Philip Stafford. Please send any thoughts and feedback to [email protected].