Hedge fund Alameda Research stepped in to shelter FTX from a loss of up to $1bn after a customer trade on the crypto platform blew up last year, highlighting the deep and longstanding links between Sam Bankman-Fried’s digital asset companies.

Alameda in early 2021 shouldered FTX’s burden when a client’s leveraged bet on an obscure token tore through buffers designed to shield the exchange from sustaining losses when a trade goes bad, according to people with knowledge of the matter.

The incident, which has not been previously reported and came more than a year before FTX collapsed into bankruptcy, shows how when one pillar of Bankman-Fried’s crypto conglomerate came under stress, he would shift the weight to another, treating the businesses that were portrayed publicly as separate as if they were one group.

It also shows how the ties between Bankman-Fried’s proprietary trading company and his FTX crypto exchange acted as a ballast long before this year’s digital asset market turmoil, when Alameda itself was bailed out with billions of dollars of loans from FTX as its other lenders retreated.

The deep relationship between FTX and Alameda, highlighted by these mutual bailouts, lies at the heart of a corporate disaster that has left potentially millions of creditors out of pocket, destroyed a business once valued at $32bn and triggered multiple investigations spanning the world just as Bankman-Fried’s crypto empire once did.

FTX lent to traders so they could make big bets on crypto with just a small initial outlay, known as trading on margin. If the traders made losses, FTX would automatically sell the cash or margin they had put up, thereby protecting the exchange.

Bankman-Fried had touted FTX’s “unique” liquidation engine, which he argued was a safer way for exchanges to manage risk. The 30-year-old had pushed legislators in the US to adopt FTX’s system, potentially opening it out to non-crypto markets.

The system included a fail-safe: it incentivised large trading groups to take over trades where the initial margin was almost wiped out. But on the riskiest, most thinly traded tokens, only Alameda was willing to serve as that last line of defence.

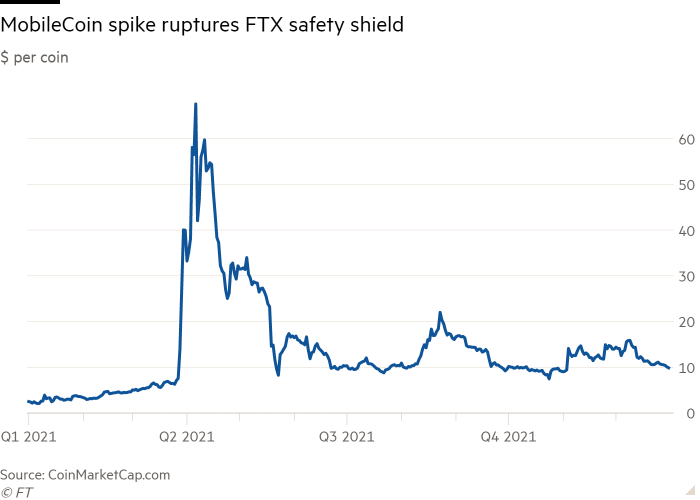

In April 2021, a crypto token called MobileCoin — used for payments in the privacy-focused messaging app Signal — suddenly spiked in price from about $6 to almost $70, before crashing back down again almost as quickly.

The wild moves came after a trader on FTX had built an unusually large position in the little-known token. Two people familiar with the matter said that when the price rose, the trader used the position to borrow against it on FTX, potentially a scheme to extract dollars from the exchange.

Alameda was forced to step in and assume the trader’s position to protect FTX. The trading company’s loss on this deal was at least in the hundreds of millions of dollars, the people said, and as high as $1bn, according to one of the people, wiping out a large share of Alameda’s 2021 trading profits.

The trading group’s role as a backstop to FTX on bad trades was reversed roughly a year later when Alameda faced trouble with its borrowing from crypto lenders.

In June, the crypto sector suffered a cascading credit crisis sparked by the failure of the stablecoin TerraUSD.

As other lenders pulled back, FTX stepped in to lend billions of dollars to Alameda, leaving the exchange dangerously exposed to the trading company, according to a letter from Bankman-Fried to former employees and a financial statement he prepared.

In the letter, Bankman-Fried said Alameda’s liabilities to FTX increased by billions of dollars last spring as “most of the credit in the [crypto] industry [was] drying up at once”.

An Alameda financial statement that Bankman-Fried drafted alongside the letter puts the trading group’s total liabilities to FTX at $10bn by the time his companies collapsed into bankruptcy.

Analysis of blockchain transactions by research company Nansen provides additional evidence that FTX acted as a lender of last resort for Alameda.

Alameda held a large stock of FTT, a crypto token issued by FTX itself, which it had used as collateral for loans. Nansen’s analysis showed large transfers of FTT from several crypto lenders throughout June, which appeared to be the return of collateral as lenders retreated from Alameda.

From mid-June into July, the Nansen analysis identified $4bn of FTT transferred from Alameda to FTX, which analysts wrote could have “been the provision of parts of the collateral that was used to secure loans”.

The heavy lending from FTX to Alameda, and their reliance on the exchange’s own FTT token, proved to be a fatal weakness for Bankman-Fried’s empire. In early November, a report from crypto news website CoinDesk revealed the large FTT position on Alameda’s balance sheet, prompting rival exchange Binance to announce plans to sell roughly $600mn of the token, knocking the token’s price.

At the same time, concerns about the company’s financial health sent FTX clients rushing for the exits, demanding billions of dollars in deposits back from the exchange.

The crisis surrounding the exchange hammered the price of FTT and two other tokens with close links to Bankman-Fried, Solana and Serum, wiping $9.5bn off Alameda’s balance sheet, and forcing the two companies into bankruptcy.