In the wake of crises past, the Federal Reserve set up a series of US dollar swaps with its main central bank counterparties around the world, so that they had access to greenbacks just in case.

The swap lines used to be set up on an ad-hoc basis, but have since 2013 been an established part of the global financial architecture, albeit a rarefied one. Only the Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank and the Swiss National Bank have access to the standing swap lines. (Others can typically get temporary ones amid major crises, like in March 2020.)

It’s a smart idea, and can be used to support a major local financial institution that urgently needs access to dollars and prevent big financial mishaps. (In theory they work both ways, but really, if we’re being honest, the Fed doesn’t really need Canadian dollars much. It’s all about giving other legit major central banks access to US dollars.)

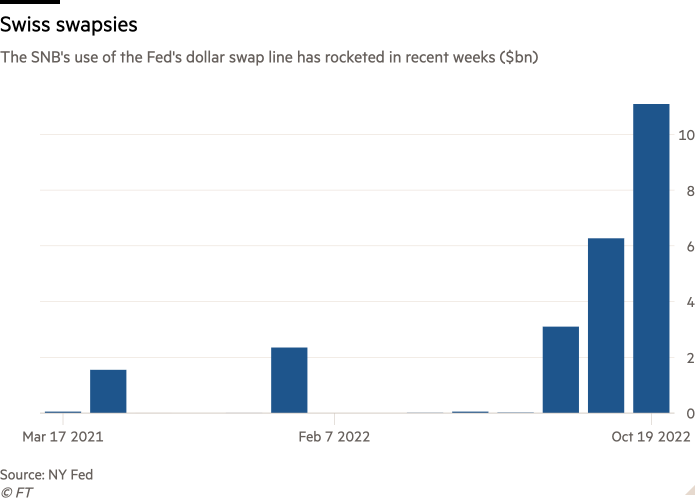

Outside of crises the swap lines tend not to be used much, aside from occasional small exercises to check their operational readiness and routine stuff. But look at what the Switzerland’s central bank has been doing lately:

For annoying, tedious technical reasons we couldn’t make a chart that goes back further than the start of 2021, but the $11.09bn seven-day swap it took down this week is by far the most the SNB has tapped the swap line for.

It nearly five times the peak amount it took at the depths of the market slump in 2020 ($2.34bn in early April that year), and the NY Fed’s data indicates that usage throughout the eurozone crisis never went above $400mn.

For comparison, the ECB’s this week only tapped the swap line for $210mn, and the Bank of Japan for $1mn. So this is not a broader issue. As JPMorgan strategist Nikolaos Panigirtzoglou said in a note last week: “There is little sign thus far of an increase in the use of the Fed’s US dollar liquidity swap lines despite the volatility in the 3-month cross-currency basis.”

And unlike, say, rumours that the Bank of Korea might seek to resurrect its Fed swap line to help stem the won’s slide versus the dollar, this cannot be about buttressing the Swiss franc. So what’s up?

The WSJ suggested last week that it may simply be that Swiss banks now have a profitable arbitrage opportunity.

Banks can borrow dollars for a week from the SNB (via the swap line). It then swaps those dollars for Swiss francs, but only has to pay around 0.20%. It can then give those francs to the SNB through a one-week repurchase auction, which pays the banks 0.45%. The bank pockets the difference between the two, around 0.25 percentage point.

Some domestic banks can make even more if they have capacity to park the extra francs overnight at the SNB, where the policy rate recently went positive, to 0.5%.

This seems possible. But we cannot imagine that the New York Federal Reserve — which oversees the swap lines — would be happy about a bunch of Swiss banks using a crisis-mitigation tool as a way to squeeze money out of various central bank facilities.

Perhaps we’re naive, but it would also seem unlikely that the SNB would be happy to facilitate this as well, given the stigma that using the swap lines heavily could entail (and articles like this)? The usual shitposters are out in force, after all.

So in conclusion this is probably one of those “probably nothing, but worth keeping an eye on” situations.