One thing to start: today is Judgment Day for the UK defined benefit pensions industry, as the gilt market reacts to the withdrawal of the Bank of England’s emergency bond-buying programme and the government U-turn on Friday. Last week pension managers shared horror stories over cocktails at the Pensions and Lifetime Savings Association Conference in Liverpool.

Welcome to FT Asset Management, our weekly newsletter on the movers and shakers behind a multitrillion-dollar global industry. This article is an on-site version of the newsletter. Sign up here to get it sent straight to your inbox every Monday.

Does the format, content and tone work for you? Let me know: [email protected]

Price pressures in commercial property

Earlier this month, thousands of European property investors arrived in Munich hoping to strike deals and share gossip over German lager, writes George Hammond in London.

But the mood at the Expo Real trade fair was “sombre”, according to Lisa Attenborough, head of the debt advisory team at estate agency Knight Frank, who attended.

While there is now near-consensus in commercial real estate crowds that property prices must come down, no one is sure how far they should fall. This has meant stasis in the market and frustration for professionals who earn their fees on transactional activity.

A sharp increase in borrowing costs — made sharper still in the UK by September’s “mini” Budget — has made it hard for valuers to price property and for banks to lend against it, said Attenborough.

Analysts at Goldman Sachs forecast that UK commercial property prices could fall by up to 20 per cent by the end of 2024. Rising interest rates have increased costs for owners of offices, shops and warehouses, just as they have homeowners looking to secure mortgages.

While there is less leverage in the market than there was before the financial crisis, big rises in borrowing costs will make it impossible for some owners to refinance when existing loans mature, forcing them to sell.

In a tumultuous market, with buyers chipping away at asking prices, landlords who can sit tight rather than sell are choosing to do so. But not everyone has that luxury.

And recent turmoil in the gilt markets is compounding the problem. It’s putting pressure on property funds to shift assets as investors accelerate their retreat from the vehicles to meet their own cash calls. The spike in gilt yields has forced pension funds running liability-driven investment strategies to sell off assets, including property fund holdings, in order to meet collateral calls.

A rush to the exits has forced fund managers, including Schroders, BlackRock and Columbia Threadneedle to suspend or delay redemptions from institutional real estate funds, at least until they can free up cash by selling property. And real estate investors are preparing for discount deals as property funds are pressed to sell off offices and warehouses.

But these sales could take months, and property funds will be hawking assets into a stuttering market. This is bad news for their investors and potentially a trigger for a marketwide doom loop of down-valuations.

“Buildings will trade, but at a lower price,” said one seasoned property investor. “The clearing price will have to be 30-35 per cent lower than in June this year.”

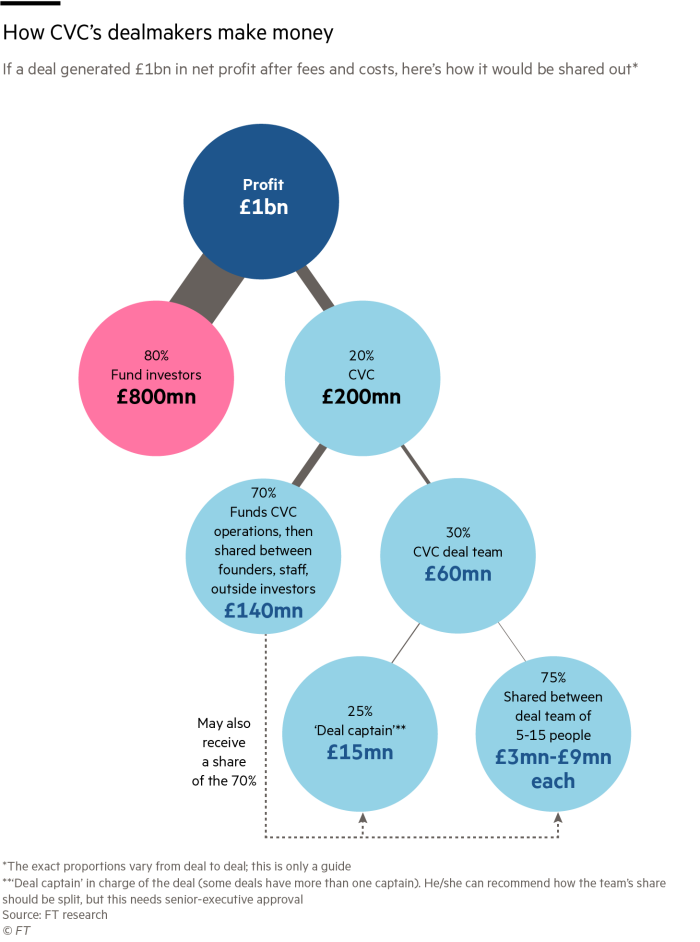

CVC’s biggest bet yet

When plans for a money-spinning “Super League” of Europe’s top football clubs collapsed in a furious outcry last year, billionaire tycoons were forced into grovelling public apologies. But behind closed doors, Europe’s largest private equity firm had long since walked away, write Kaye Wiggins and Arash Massoudi.

CVC Capital Partners abandoned the project after early-stage talks about a possible investment. Then, after its collapse, the buyout firm stepped up to buy a stake in La Liga, Spain’s football league, for €2.1bn, giving it a share of broadcasting and commercial revenues for up to half a century.

If those revenues keep growing at present rates, CVC could treble or even quadruple its money in the next decade. Since the league is not on the hook for clubs’ costs, the vast majority of CVC’s revenue is profit.

“It’s the best deal in the history of private equity”, a rival football dealmaker says. “They are not going to lose money here.”

CVC has made tens of billions of euros buying stakes in household-name brands from Debenhams to Formula One to the maker of PG Tips tea, all while remaining largely hidden from public view.

Now, almost three decades since it spun out of Citibank’s London office, the 700-person firm with €133bn in assets is at a crossroads. By the beginning of this year, its top executives had finally decided to take the firm public.

That would bring it into line with its larger rivals, such as Blackstone, KKR, and Carlyle; allow it to stay ahead of European competitors like EQT, which has grown rapidly since listing in 2019; and permit the founders who still oversee the firm to eventually cash in their stakes.

But it would also attract a level of scrutiny that it is not used to, and risks watering down the high-risk, high-reward model that is fundamental to CVC’s culture — reducing its rainmaker executives to a smaller part of a sprawling institution.

CVC’s listing will test whether one of Europe’s oldest buyout groups can modernise. Don’t miss don’t this in-depth account of the company at a pivotal moment in the history of both it and the private equity industry.

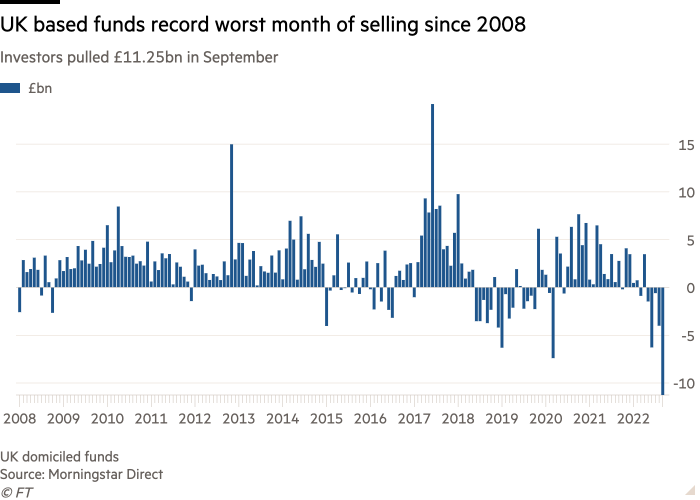

Chart of the week

The market chaos touched off by chancellor Kwasi Kwarteng’s fiscal plans has dealt a heavy blow to UK mutual funds, which suffered their largest monthly outflows in September since at least 2008. UK-based funds haemorrhaged £11.25bn last month, according to data from Morningstar Direct, far surpassing the previous worst bout of outflows at the peak of the Covid-19 crisis in March 2020, when funds lost £7.4bn.

Meanwhile assets under management in UK-domiciled funds have dropped a fifth from the peak in December, as funds withered in the market downturn and investors pulled nearly £20bn. “There is a lot of pessimism around . . . Every asset class saw net outflows for the first time,” said Jonathan Miller, analyst at Morningstar.

10 unmissable stories this week

Sterling money market funds have gathered £53bn in just a fortnight as UK pension schemes rushed to build defences against market volatility before the end of the Bank of England’s emergency bond-buying programme on October 14. UK pensions funds called on the BoE to extend it beyond the deadline on concerns trustees do not have sufficient time to shore up their portfolios against further shocks.

Northern Trust was overwhelmed by a slew of margin calls during the UK government bond market turmoil, hampering the ability of pension funds to raise cash. The large US custody bank acts as a depository for two of the biggest liability-driven investment managers caught up by the gilt sell-off, Legal & General Investment Management and Insight Investment.

The liquidity crisis engulfing the gilts markets has put at risk a government initiative to use pension funds to drive economic growth and the transition to a low-carbon economy, executives have warned.

BlackRock reported a drop in assets under management and profits and announced it would cut spending and pause discretionary hiring as the world’s largest money manager was buffeted by falling markets. The group has lost more than $1bn in asset management business in US Republican states upset with the company’s green investing policies, withdrawals that have become a political problem but have not dented the company’s revenues.

Brevan Howard and Aspect Capital are among the hedge funds betting that the dollar still has further to rise after big gains this year, propelled by the US Federal Reserve’s determination to curb inflation with tighter monetary policy.

Billionaire trader Chris Rokos has been among the major hedge fund managers who have profited during the crisis gripping UK financial markets, running a bet that UK borrowing costs will have to rise.

The managers of Harvard University’s $51bn endowment have warned of substantial markdowns to come in its private equity and venture capital portfolio, predicting heavy losses for institutional investors.

The plummeting value of sterling means that “everything in the UK is on sale”, according to Blair Jacobson, co-head of European credit at Ares Management, a pioneer in private lending. Merger arbitrage funds are also sensing an opportunity from an expected pick-up in UK mergers and acquisitions.

Is one of Britain’s biggest asset managers past repair? Abrdn is a victim of more than sectoral decline, writes columnist Cat Rutter Pooley. There’s investment performance. Outflows. An expensive acquisition. A much-mocked rebrand. Shares that have slipped so much that five years after an £11bn merger, the company fails to make the FTSE 100 any more. And a chief executive, Stephen Bird, who seems to have alienated investors.

Insurers expect more UK companies to offload their pension schemes to them after surging government bond yields increased the appeal of such deals and the market turmoil underlined the risks in managing retirement plans.

And finally

Summer is well and truly over and the nights are drawing in. Time to hunker down on one of the velvet banquettes at Otto’s on Grays Inn Road. This cosy restaurant is the epitome of old school French fine dining. All the classics are on the menu: doubled baked cheese soufflé, steak tartar, tarte Tatin etc. But Otto’s, said to be the only restaurant in the UK that owns a duck press, is most famous for its Canard à la Presse, in my mind the most spectacular recipe In the classical French repertoire. Spread out over three courses: Challans duck Liver, morel mushrooms on seared calf’s sweetbread; then Challans duck breast, pommes soufflées, Otto’s pressed duck sauce; and finally semi-confit and roasted duck leg, seared foie gras and black truffle sauce. I defy you to think of anything more decadent. Canard à la presse comes from Rouen in Normandy and it’s also a speciality of the Tour d’Argent restaurant in Paris.

Thanks for reading. If you have friends or colleagues who might enjoy this newsletter, please forward it to them. Sign up here

We would love to hear your feedback and comments about this newsletter. Email me at [email protected]

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

The Week Ahead — Start every week with a preview of what’s on the agenda. Sign up here