Cyprus has attracted a different sort of visitor recently. US buyout group Lone Star has taken an interest in Bank of Cyprus, the island nation’s largest lender. It has made three unsolicited offers and says it is pondering a fourth. The latest values the bank at almost €700mn. But an attractive price alone may not win Lone Star the prize it craves.

Cyprus has done well to clean up its financial mess of a decade ago. The bank then chose to bail-in bank depositors during the European debt crisis. A 50 per cent haircut for savers with more than €100,000, mostly foreigners and including many Russians, helped finance the recovery. It has since disposed of many of its non-performing loans, as Cyprus’s economy rebounded after the crisis.

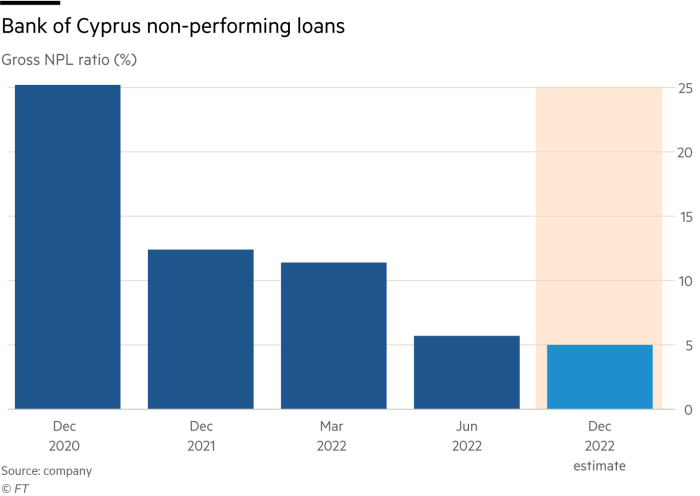

No doubt Lone Star had noted Cyprus has stabilised. System-wide bad loans have fallen 78 per cent, about €7bn lower, in the past five years. As a share of gross loans, NPLs stood at 11 per cent systemwide. Bank of Cyprus, with 40 per cent of the loan market, has done better getting its ratio closer to 6 per cent at the end of June.

A rebound in economic growth should mean real GDP expands by 4.5 per cent this year. While some links with Russian businesses linger, these now only account for about 2 per cent of outstanding loans.

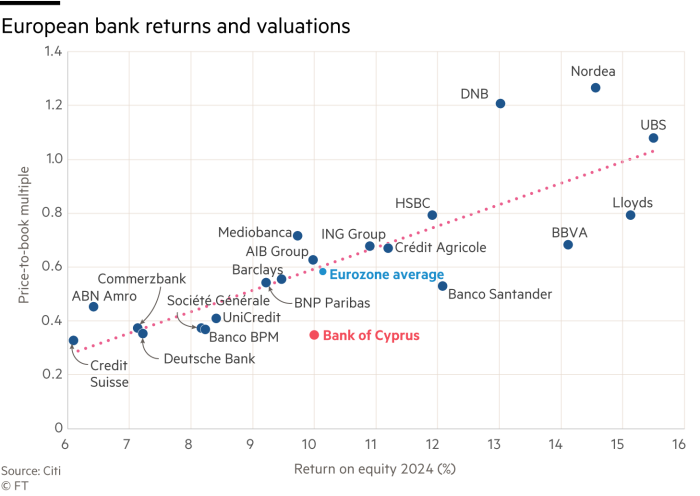

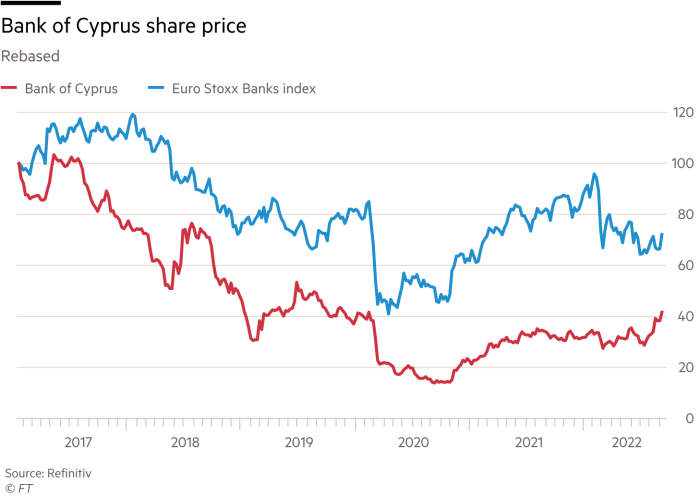

Bank of Cyprus has returned to profit and expects to earn a return on tangible equity of 10 per cent in 2024. This turnround and the bid interest have helped the London-listed share price rally 36 per cent this year, a far better return than the MSCI Europe banks index.

On this profitability, a simple regression of returns at European banks suggests it merits a valuation almost twice the 0.35 times tangible book value of Lone Star’s latest offer. Even with a sizeable discount for past transgressions, the bank’s shareholders deserve a higher price.

Not only shareholders but local regulators will need convincing. They will fear short-term capital gaining control of a bank only recently nursed back to health. Watchdogs are rushing to enact blocking legislation. Even a higher offer may not win the deal for Lone Star.