Unlock the White House Watch newsletter for free

Your guide to what the 2024 US election means for Washington and the world

Good morning. The vaccine manufacturers Moderna and Novavax fell 5.6 per cent and 7 per cent, respectively, yesterday on the news that prominent anti-vaxxer Robert F Kennedy Jr is Donald Trump’s pick to head the US Department of Health and Human Services. If Kennedy gets confirmed by the Senate — or is a recess appointment — what is the next trade? Sell fluoride producers? Buy a dairy farm? Email us: [email protected] and [email protected].

Small-caps

In the run-up to the US election and in the days since, a dormant market narrative awoke. Small-caps, which had a lively but shortlived rally back in July, have surged since mid-October, outperforming the mid- and large-caps over the past month:

When we wrote about small-caps this summer, we argued that a true small-cap renaissance may never come. The performance gap (on metrics such as return on equity) between big-cap and small-cap indices has widened as the Magnificent Seven have prospered. And one standard argument for why small-caps fare better in a low-rate environment — that they are more leveraged, often with floating rate debt, and are thus poised to do well as rates fall — turns out to be badly overplayed. Small-caps’ debt burdens actually fell as rates rose in the past few years.

But there are several other good reasons that the relative performance of small-caps might improve under the Trump administration. The market consensus is the president-elect’s fiscal policies will boost growth. Smaller companies tend to be more economically sensitive than larger companies, as they have less ability to manage their cost bases. Small changes in revenue mean larger changes in profit. This may be especially true now. Surveys from last year and labour data suggest that there has been “labour hoarding” among smaller companies, which drives up fixed costs and increases operating leverage.

A corporate tax cut would also help small companies more than big ones, given that they tend to generate more of their revenue and profits domestically. Furthermore, “large and to some degree mid-cap companies have already optimised their tax situation relatively well” since they employ more tax professionals, said our pal Dec Mullarkey at SLC Management. Here is a chart from Goldman Sachs, showing that stocks in the Russell 2000 are highly sensitive to changes in the tax rate:

The Trump administration is also expected to loosen the guardrails on mergers: many bite-sized companies may be gobbled up at a premium. Mergers aside, regulatory easing may be more helpful to small companies than to big ones. Rob Arnott of Research Affiliates suggested to us that for big companies, regulations are as much a barrier to competition from pesky smaller groups (for whom the cost of regulation is relatively heavier) as they are a drag on profit. And small-cap indices have a high exposure to industries expected to do well under the Trump regulatory regime, such as energy, banks and industrials. Small-cap industrials in particular may benefit more from Trump’s policies than their mid-cap and large-cap counterparts — small-cap manufacturers are often domestically focused, so they could theoretically benefit if he erects higher trade barriers.

There are — as with every aspect of the Trump trade — a lot of uncertainties here that will have to be resolved. The growth effects of his immigration and tariff policies might well be negative. Domestic manufacturers will certainly face higher input costs, for example, so their domestic advantage may be limited. The next administration also may not be as anti-antitrust as the market currently expects. Vice-president-elect JD Vance has praised current Federal Trade Commission chair Lina Khan in the past, and Trump’s recently announced attorney-general pick Matt Gaetz has been all-in on big tech break-ups in the past.

Might the small-cap rally be a bit overdone, then, or at least exhausted for now? It is interesting in this context to look at the mid-cap indices, which have a certain goldilocks quality: the S&P MidCap 400 index has higher quality companies than the S&P SmallCap 600, but has a similar sectoral mix, including a lot of regional banks and energy companies. Yet small-caps have outpaced mid-caps this month. The small-cap index’s forward price/earnings valuation even briefly passed the mid-cap index’s this week:

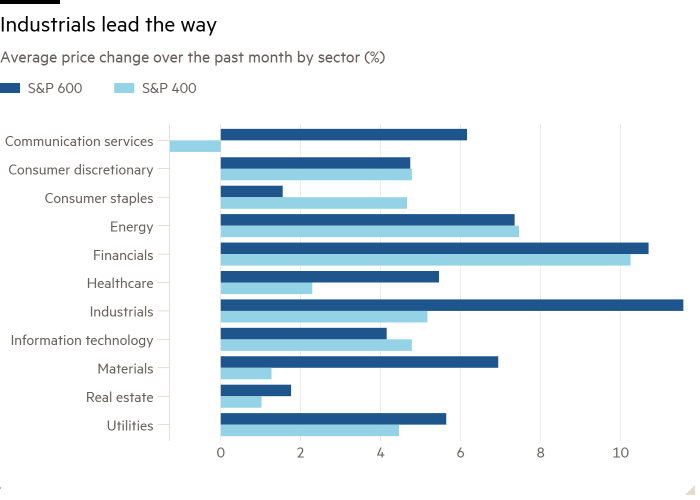

Consider industrial stocks — an area where Trump-trade excitement has been particularly high — in the two indices. Both the S&P 600 and the S&P 400 are about one-fifth industrial stocks by market cap. Over the past month, industrials in the S&P 600 have had an average price increase of 12 per cent; those in the S&P 400, 5 per cent. Industrials are not alone; materials have had a smaller, but similar gap. Greater leverage to economic growth or domestic customer bases might explain some of the difference, but probably not all of it. (Communications companies in the small-cap index are vastly outperforming those in the mid-cap index, too, but the industry is under-represented in the mid-cap index.)

We think that this might be a good moment to own either group. Both indices’ valuations are near their long-term historical averages, whereas the big cap S&P 500 is at a 30 per cent premium to history. But, at a moment when economic uncertainty is high, mid-caps look more appealing to us.

(Reiter and Armstrong)

One good read

The answer is usually a bigger pile of money.