Stay informed with free updates

Simply sign up to the EU energy myFT Digest — delivered directly to your inbox.

Europe has survived two consecutive winters since Russia invaded Ukraine and weaponised gas supplies. Yet as the region heads into the colder months, traders and analysts are concerned about the region coming out of this winter as smoothly.

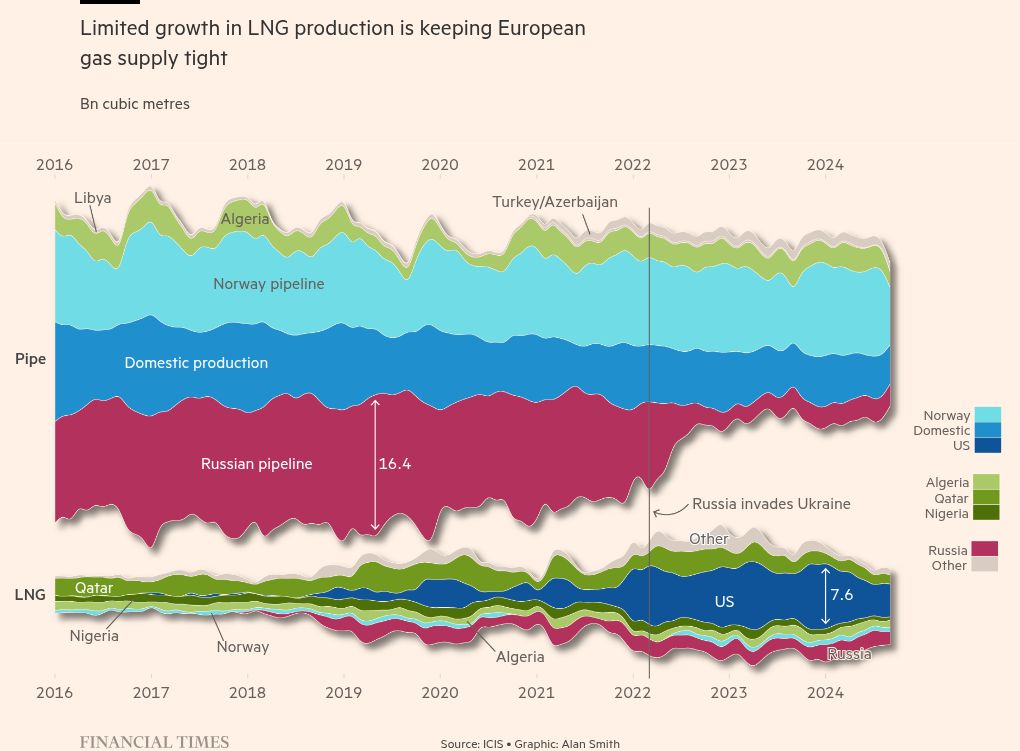

One fundamental problem is that the European gas market is now connected to the volatile global energy markets more than ever, as a result of its forced diversification from Russian pipeline gas to liquefied natural gas.

“As it stands, Europe’s gas storages are full and the winter gas balance looks OK,” one trader said. “But anything can happen. You just need a few supply disruptions and things could go horribly wrong.”

LNG is a global commodity, often being shipped to buyers who pay the highest. Global supply is tight, meaning Europe needs to compete with Asia when demand is high. That necessitates higher gas prices to incentivise traders to send the specialised vessels to European shores.

In 2021, the super-chilled fuel only accounted for about 20 per cent of wider Europe’s overall gas supplies. Russian gas accounted for 30 per cent. LNG now makes up 34 per cent of wider Europe’s gas supplies.

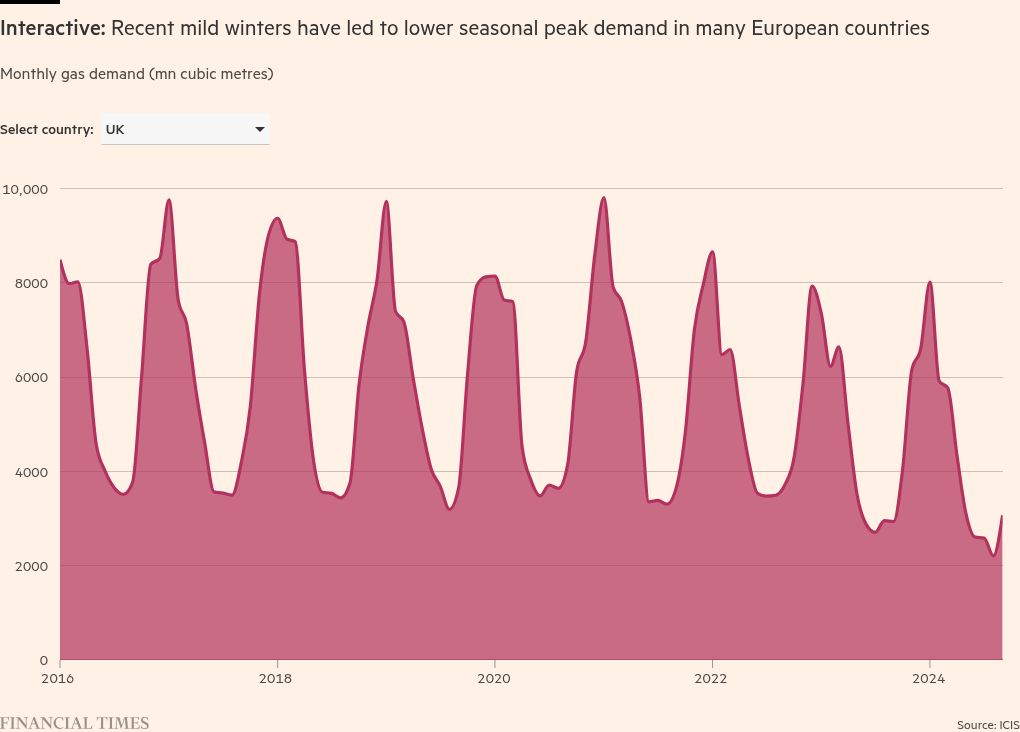

The Europe-Asia tug of war for the seaborne fuel is at its most intense during the cold months, when heating demand increases. The past two winters have been mild, however, allowing Europe to reduce its gas and LNG demand. Mild temperatures also allowed the region to end winter with record levels of gas left in storage.

But the market is “taking into account that this winter would be normal”, said Sindre Knutsson, partner at Rystad Energy. That alone would increase gas demand compared with previous winters.

The additional complication this year is the looming expiry of the gas transit contract between Ukraine and Russia, one of only two routes via which Russian pipeline gas still flows to Europe. The deal that facilitates the flow of about 5 per cent of the EU’s annual gas imports comes to an end on December 31, just as the need for heating nears its peak, although negotiations to keep gas flowing through Ukraine are ongoing.

European countries may also need to export gas to help Ukraine during the winter, as it endures Russian attacks on energy infrastructure.

“If we suddenly get a very cold winter at the same time as we lose the Russian gas flows, that will just be very bullish for gas prices,” said Florence Schmit, energy strategist at Rabobank. “And I don’t think there’s going to be any big alternative supplies via [other] pipelines. I think most of it will need to be replaced by LNG.”

Due to delays in start-ups of new export facilities, LNG supply growth will remain limited this winter, restraining the pool of LNG Europe can call upon. Commodity data firm Kpler estimates that only 2.5mn tonnes of LNG will be added to the market this winter, about a quarter of the new additions during last winter.

There are also concerns over tensions in the Middle East; should any escalation lead to the closure of the Strait of Hormuz, it would jeopardise 20 per cent of the global LNG supply.

The International Energy Agency warned in its latest report on global gas markets that the global gas balance “remains fragile as limited growth in LNG production is keeping supply tight” and that “markets remain sensitive to unexpected supply or demand side movements”.

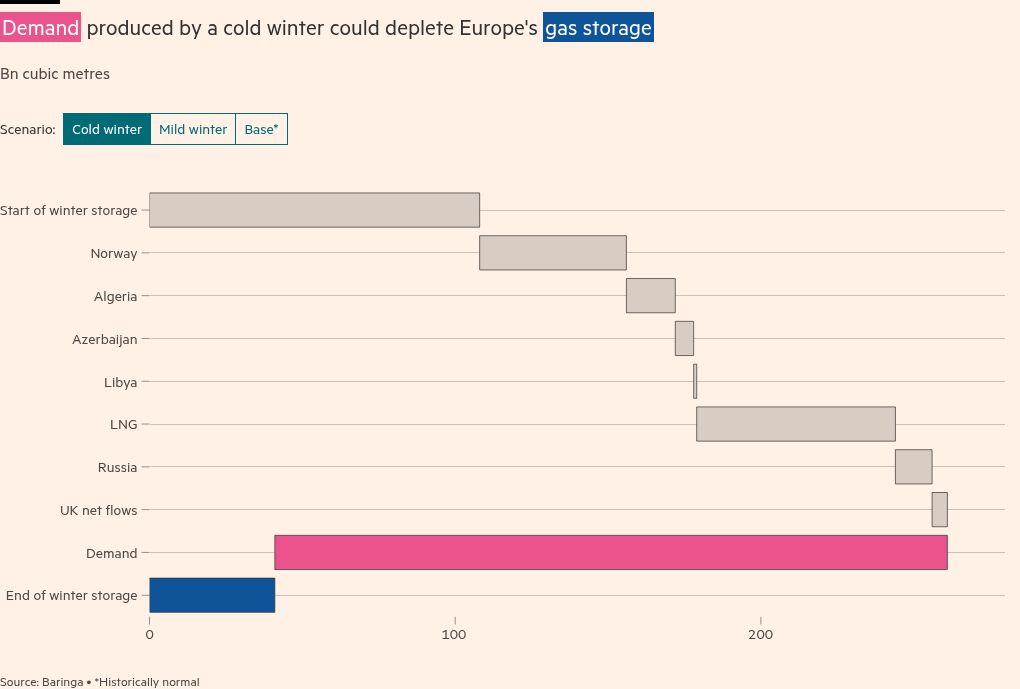

In a base case scenario, which assumes historically normal temperatures, analysts and traders expect Europe to end the winter with gas storages about 45 to 55 per cent full. That is less than in the previous two mild winters, when Europe ended winter with storages about 60 per cent full. Should Europe experience a much colder winter, storage levels could drop to about 35 per cent, analysts said.

Storage levels at the end of the winter determine how much gas is needed to fill it back up during the next six months. The lower the level at the end of winter, the more LNG would need to be imported, which could potentially lead to higher gas prices even during summer months when demand drops.

Acer, the EU’s energy watchdog, warned in a recent report: “If gas withdrawals this winter significantly exceed those of the past two, EU buyers may need to increase their competitiveness in LNG markets to replenish stocks in 2025, potentially driving up wholesale gas prices.”

“In the end I think it’s less a volumetric risk — as in the lights might go out because we don’t have enough gas — and more a price risk,” said Peter Thompson, director at consultancy Baringa. “It’s ‘how much might we have to pay for that LNG?’”

At the height of the energy gas crisis in 2022, European gas prices surged, at one point rising above €300 per megawatt hour for the first time ever. That allowed the continent to lure LNG, at the expense of developing nations who needed it, but were priced out.

“The risk is we don’t run out of gas this winter, but it gets a lot more difficult to fill to a comfortable level ahead of next winter,” said a gas trader. “You’ll always have gas. The question is what price you get that gas in.”