Unlock the US Election Countdown newsletter for free

The stories that matter on money and politics in the race for the White House

This article is an on-site version of our Unhedged newsletter. Premium subscribers can sign up here to get the newsletter delivered every weekday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Good morning. Homebuilder DR Horton’s stock fell more than 7 per cent yesterday after a disappointing earnings report. Homebuyers are waiting for mortgages to get cheaper (they may be waiting a while; see below). It seems that high rates have finally caught up with the homebuilders — only two years, and a huge rally, after Unhedged thought they would.

Other news yesterday made Unhedged feel slightly less stupid. Alphabet, Unhedged’s favourite member of the Magnificent Seven, reported strong results, driven by cloud computing. The stock popped in late trading. The market is counting on the good news from Big Tech continuing this afternoon, with reports from Microsoft and Meta. Email us: [email protected] and [email protected].

Trump, Treasury yields and the dollar

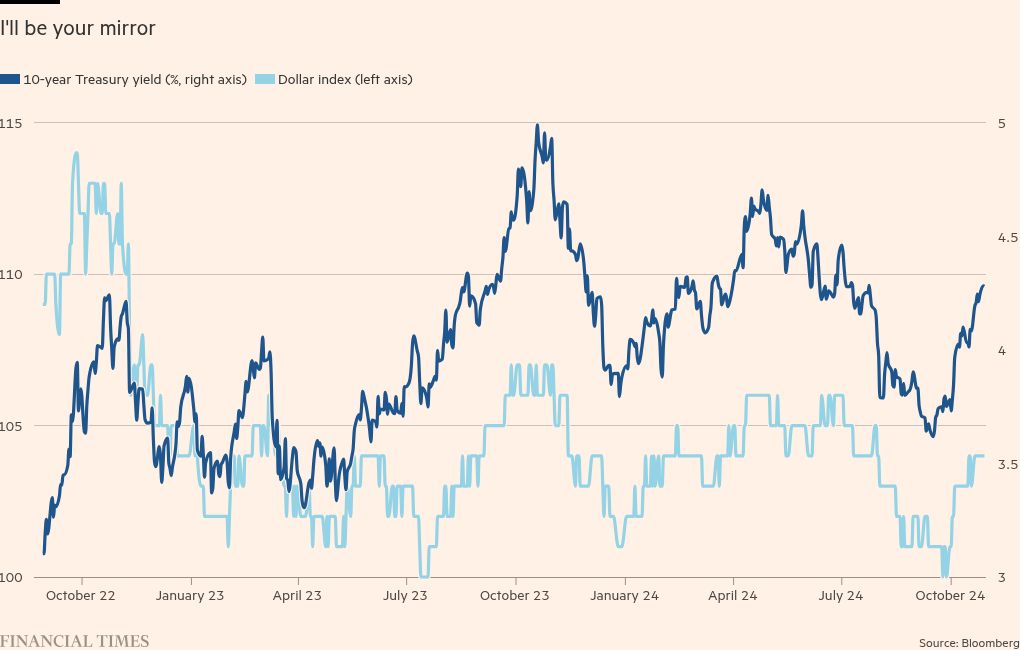

The 10-year US Treasury yield has been moving more or less hand in hand with prediction market odds of Donald Trump retaking the oval office. What links the two is the idea that a Trump victory will bring larger fiscal deficits than a Kamala Harris. Bigger deficits mean hotter growth and tighter monetary policy. There is also the notion that Trump’s proposed immigration crackdowns and tariffs will be inflationary.

Charts like this one have appeared in a lot of research reports lately:

A few provisos. As we have written, prediction markets have a mixed record in elections and their participants may be a bad sample of the electorate. And if you look at the same two series over a longer period, you see that they only started to travel together consistently when Harris entered the race in July:

A lot of the recent Trump/rates correlation could be happenstance. A pattern of stronger economic data in the past month or so, which has encouraged the bond sell-off, just happened to coincide with the end of the Harris Honeymoon in the polls. When looking at market trends, however, logic only gets you so far. The “Trump is the candidate of fiscal expansion and maybe inflation” narrative has taken hold, and will persist until it is dislodged by a more compelling story.

The correlation between Trump’s increasing odds of victory and a stronger dollar has received less attention. This may be because the connection between higher rates and a stronger dollar is so obvious. As US rates rise relative to those in the rest of the world, a strong dollar follows almost mechanically.

So to the degree that Trump’s ascent explains higher rates, it explains the stronger dollar, too. There is an irony here. Trump doesn’t like the strong dollar. He says that other countries have manipulated their currencies to weaken them relative to the dollar, “a tremendous burden on our companies.” He has threatened to respond with tariffs. Unhedged has argued that weakening the dollar against other key currencies would be hard. And while some potential Trump economic officials, such as Robert Lighthizer, are weak-dollar fans, others, such as Scott Bessent, say Trump is secretly a strong-dollar guy who is only using tariff threats as a negotiating tactic.

Whatever Trump’s real position on the dollar is, that the US currency strengthens in anticipation of its fiscal position getting worse is a neat demonstration of the America’s peculiar position in the global economy.

A stronger dollar does create some drags on the US economy, for example by making its exports more expensive. But it hurts the rest of the world more — making the dollar stronger still. Joseph Wang, in a recent post on his blog, sums up the situation with characteristic pithiness:

The increasing probability of higher fiscal deficits appears to be pushing Treasury yields higher, which in turn is increasing the attractiveness of the dollar. Higher Treasury yields are also dragging foreign yields higher despite [other countries’] weaker economic circumstances. The combination of higher global yields and a stronger dollar amount to a global tightening in financial conditions that may prompt other central banks into more rate cuts that further strengthens the dollar.

This somewhat paradoxical and self-reinforcing situation can persist until, as Wang puts it, “the bottom falls out” — when the world loses its willingness to finance US deficits in return for modest yields. This is what briefly happened to the UK in 2022. No one has any idea when it will happen to the US. Our only reassurance is the fact that it hasn’t happened yet. Until it does, Wang concludes, “big deficits will be risk positive”, just as they have been for the past five years.

Deficits are not the only reason the dollar is strengthening. As Tyler Cowen pointed out in a Bloomberg column yesterday, a strong US economy with high investment requirements supports the dollar, as does the lack of an alternative debt asset that is safe, liquid and issued by an open economy. That said, investors need to accept that the relationship between the United States’ currency and its fiscal policy will remain paradoxical.

One good read

Well, this explains a lot.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

Chris Giles on Central Banks — Vital news and views on what central banks are thinking, inflation, interest rates and money. Sign up here