Oussama Nasr is a former derivatives banker who lives in Beirut.

You might have seen headlines on Lebanon’s massive pile of long-defaulted international bonds rallying on Israel’s invasion. Here’s why that isn’t quite as mad as it might initially seem.

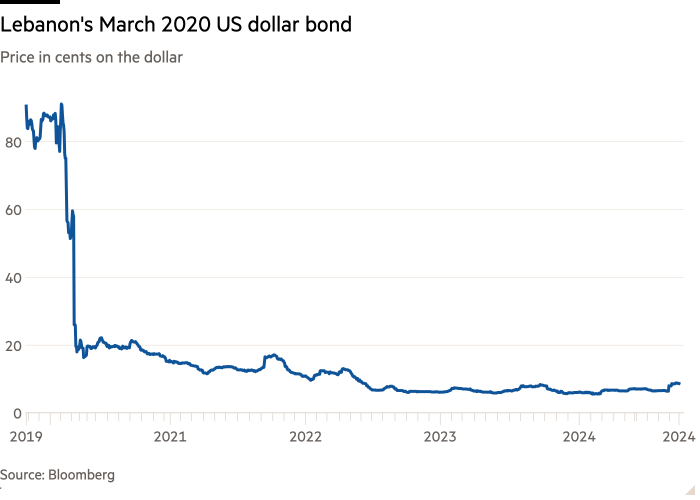

But first we probably need to explain exactly how Lebanon’s eurobonds with a face value north of $30bn came to trade at 6 cents on the dollar.

Chronicle of a default foretold

After a brutal 15-year civil war that ended in 1990, Lebanon undertook a vast reconstruction program funded largely by the issuance of bonds denominated in US dollars. These bonds were always rated below investment grade, and gradually nearer and nearer to very-junky triple-C levels, as the country’s debt stock mushroomed, its political stability evaporated, its attraction as a tourism destination waned, and its tax collection practices remained close to non-existent.

Offsetting these catastrophic conditions were two factors that helped keep the country going financially:

(i) the availability of support from a number of friendly countries in Europe and the Gulf.

(ii) the presence of a huge, industrious expatriate community who would remit — come rain or shine — about a half-billion US dollars monthly to their relatives in the old country.

However, as the financial situation kept deteriorating and credit rating agency downgrade followed downgrade, the bonds naturally traded at gradually wider spreads.

By early 2020 the country could no longer take the pressure of servicing its debt, and defaulted simultaneously on all its outstanding international bonds worth about $31bn in aggregate. At this point the bonds began trading on a price basis, gradually declining from 40 cents on the dollar or so to just below 6c in recent months.

They have bounced back in the past month to almost 9c, after Israel began its massive campaign against Hizbollah, the dominant militia in the country and its most powerful political party.

Given the scale of the collapse since 2020 this may seem minuscule, but it’s a notable and interesting jump.

(It needs to be stressed that trading volumes are extremely low, and that the ability to liquidate a meaningful block of bonds at this new price is questionable. We’ll nonetheless assume that the price of 9c is “correct”.)

The country’s endemic corruption, lack of governance, ongoing political instability, and continuing absence of any tax base to speak of, ensured that few savvy international investors were interest in Lebanon’s eurobonds at virtually any price.

As a result, Lebanese banks continue to hold a substantial chunk of the total debt stock, and only a few specialised money managers and hedge funds have the enthusiasm to gamble on the potentially mouthwatering returns that could follow an eventual restructuring.

Why 6? Why 9? Why not zero?

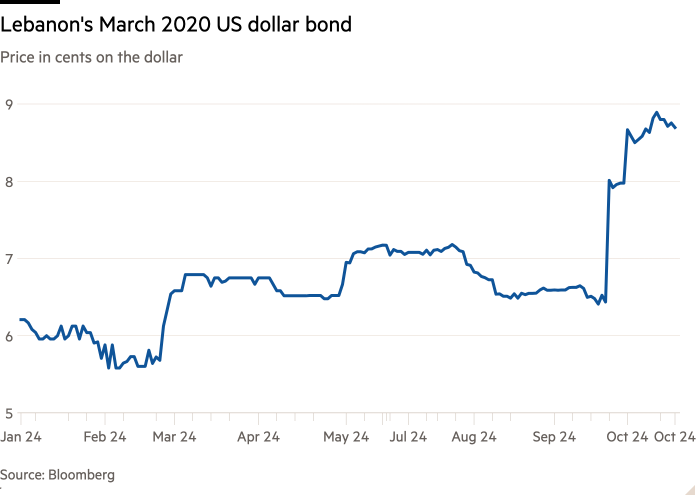

So what does a price of 6c — or alternatively 9c — actually mean for a defaulted sovereign bond?

It should be noted that only countries such as Cuba, Sudan, North Korea and Vietnam (before its reforms) have seen their debts traded at comparable prices. Lebanon, even in the midst of a devastating economic collapse, total political paralysis and an actual war boasts meaningfully higher living standards than those countries, particularly when its gigantic unofficial economy, and the unregistered portion of overseas remittances, are properly accounted for.

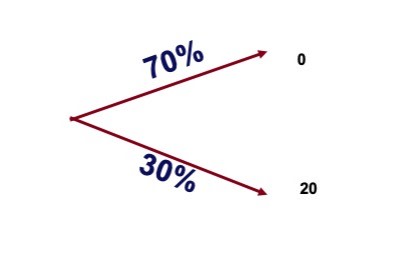

Simplifying enormously, you can think of the price of 6 as the probability-weighted average of two outcomes: one in which the country stays a dysfunctional, near-failed state — in which case the debt would eventually become virtually worthless — and another in which at least some hint of prosperity and stability returns, and some kind of debt workout is eventually achieved, which might cause the debt to trade at about 20c (but realistically probably not much higher).

Under this analysis the probability of the first outcome would be close to 70 per cent, while that of the second outcome would be the residual 30 per cent.

If this model is broadly correct, the more recent price of almost 9c would be consistent with a reduction in the first outcome’s probability to 55 per cent and an increase in the second outcome’s probability to 45 per cent.

In other words, the market is now implying a 15 per cent higher probability (in absolute terms) and a 50 per cent higher probability (in relative terms) to the scenario that Lebanon will become a semi-prosperous, semi-peaceful state — even while the Israeli ground operation continues unabated, the country’s economy is paralysed and civilian casualties mount.

Is this increased optimism consistent in any way with the most recent political developments in the country? The credit rating agencies certainly don’t think so. Here’s what Moody’s said in a report earlier this month:

The unfolding conflict within Lebanon’s own territory compounds an already very bleak credit picture and undermines the Lebanese government’s efforts to stabilize the economy through increased dollarization. The conflict’s population displacement will exacerbate weaknesses in the country’s already stressed health and social conditions. Also, a degradation of infrastructure and public services further undermines any prospect of economic recovery in the near term.

That FATF has now placed Lebanon on its “grey list” is another blow to any hopes of its financial system returning to health any time soon.

But bond traders appear to be more optimistic. The new price of 9c suggests that at least some have bought off on the scenario that the possible elimination or severe castration of Hizbollah will cause a measurable improvement in the country’s governance, its willingness to implement long-overdue reforms and sign an IMF agreement, and ultimately its ability to restructure its external debts.

So how realistic is this?

The plausible (ish) scenarios

Here are five potential pathways for Lebanon and Lebanese debt, of which only the first two are positive.

1. Israel achieves continued success against Hizbollah and in effect amputates the organisation so badly that it ceases to dominate Lebanese politics and loses its ability to obstruct necessary reforms. Lebanon proceeds to implement those reforms, signs an IMF agreement and successfully restructures its external debt.

2. Hizbollah recovers from its initial setbacks and fights Israel to a standstill inside Lebanon, similar to what it achieved in 2006. This enhances Hizbollah’s standing within Lebanon and leaves the party stronger than before. Nonetheless, Hizbollah becomes more integrated in the Lebanese body politic and begins to co-operate with the movement to implement reforms, sign an IMF agreement and ultimately restructure the external debt.

3. Same as (2) with Hizbollah stronger even than before the ground offensive. But this leads to no reforms, no IMF agreement, and no restructuring of the external debt.

4. Israel achieves continued success against Hizbollah and ends its dominance of Lebanese politics; but the remaining Lebanese factions turn out to be incapable of national reconciliation and unable to sign an IMF agreement, so no debt restructuring is forthcoming.

5. Israel damages Hizbollah severely, but the organisation remains the most powerful political group within Lebanon and is able to continue impeding reforms, obstructing an IMF agreement and thus stymie any debt restructuring.

Anyone who’s lived in the Middle East will know to discount the optimistic scenarios, and therefore be understandably sceptical that the Lebanese bond rally can be sustained.

Gimme options

A lot of FT Alphaville readers will know this already, but the best explanation for the seemingly bizarre price action in Lebanese bonds can be found in options theory.

The value of an option typically increases — sometimes quite measurably — when the underlying asset experiences rising volatility. That is especially true for heavily “out-of-the-money” options. These are cheap because the likelihood of them coming good before they expire is so fantastically unlikely. But if they do then the pay-offs can be astronomical.

And in most option pricing methodologies greater volatility mechanistically increases their value, because it improves the chances of improbable outcomes.

Assume you’ve bought a one-year call option on Microsoft with a strike of $100 when the spot price is $80 and the stock’s volatility is 20 per cent. Subject to reasonable further assumptions regarding the stock’s dividend yield and the risk-free interest rate, we can calculate that the value of this option, at inception, is slightly higher than $1.

In effect, the option is very cheap because the likelihood that the spot price at expiration will exceed $100 is low, given the current price of $80 and the 20 per cent volatility. In fact, it is approximately 85 per cent probable that the option will expire out-of-the-money, and you’ll lose your premium. In other words, that you’ll suffer a 100 per cent loss. However, if the spot price does rise above $100, the gains can be big. For example, if Microsoft hits $105 you’ll realise a 400 per cent profit.

More relevantly to the Lebanese eurobond situation, we can also calculate that if the spot price does not budge but volatility rises from 20 per cent to 30 per cent, for example, the owner will double their money. If the volatility doubles to 40 per cent then the option quintuples in value.

Now comes the “killer insight”: a deeply distressed equity or debt security is analogous to an out-of-the-money call option in the following two respects at least:

(i) it is very cheap and thus has a (modest) probability of producing returns in the hundreds of percentage points, like the Microsoft call option above,

(ii) it has a high probability of returning negative 100 per cent or something close to it — the expected outcome if Lebanon proves wholly unable to reconcile internally, implement necessary reforms and restructure its external debt.

You’d therefore rightly expect that Lebanese bonds become more valuable when the country becomes more volatile, something that has undoubtedly occurred since the initiation of the Israeli invasion and the assassination of Hizbollah’s Hassan Nasrallah.

This might easily explain the price increase from 6c to 9c. And from here, who knows.