Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Make Boeing iconic again! It is a bold goal from a tarnished American icon, and one that shareholders — who have seen Boeing stock halve in five years — can no doubt get behind. To make it more than just talk, new chief executive Kelly Ortberg will need manufacturing brilliance, patience and an awful lot of cash.

Ortberg has some immediate problems. Boeing made a loss of $8bn in the first nine months of the year. Striking workers and unfinished planes languishing in hangars intensify the rate at which its cash is going up in smoke. Some 33,000 machinists were due to vote on a new pay package on Wednesday. Even if they agree to go back to work, Boeing remains mired in production problems.

It is worth thinking through what an iconic-again Boeing would look like. In 2018, before the company was hobbled by two fatal crashes of the 737 MAX and a guilty plea for criminal fraud, Boeing made a record $101bn in revenue, delivering 806 commercial planes. This year so far it has made $51bn and delivered 291. Back at its peak, the company made $14bn of free cash flow; this year and next year, that number will be negative.

Those past financial aerobatics cannot be the kind of iconic Ortberg has in mind. Boeing’s previous figures were possible partly because it was horribly underinvesting in its planes, in the pursuit of keeping investors happy. That worked, until it catastrophically didn’t.

This time, what is in store is a slow — very slow — climb back to profitability. The $100bn of revenue may be possible again, given Boeing has a backlog of 5,400 commercial planes, but such generous cash generation almost certainly is not. At some point, Boeing will need a new plane too — which is likely to cost tens of billions of dollars.

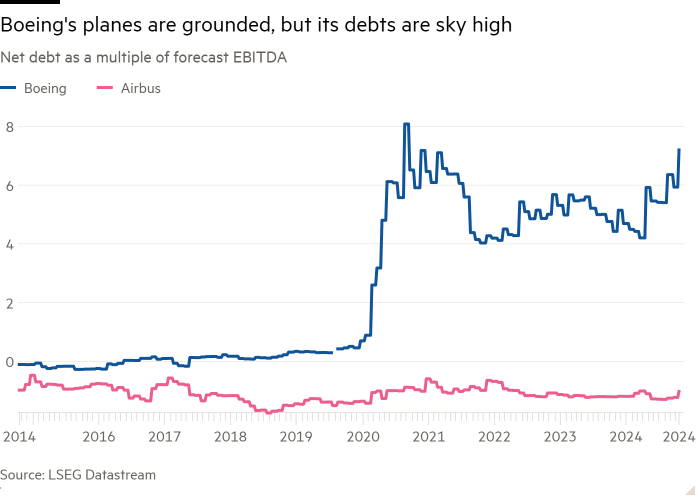

One area where Ortberg really could do with turning back the clock is Boeing’s balance sheet. It is currently weighed down with $58bn of debt — $44bn more than six years ago. Chief rival Airbus has production problems of its own, but at least it has more cash than debt. Raising equity could cut Boeing’s mountain of borrowings by maybe $15bn.

For now, Ortberg is mostly offering big promises to restore Boeing’s status as an example of “good culture”, starting with him spending lots of time on the factory floor. That has shades of General Electric turnaround boss Larry Culp, who likes to walk around his facilities brainstorming efficiency with his employees. Culp eventually rehabilitated his own fallen icon by breaking GE up. Ortberg’s flight plan might yet involve something similar.