This article is an on-site version of our Trade Secrets newsletter. Premium subscribers can sign up here to get the newsletter delivered every Monday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

I’m in Washington DC for a few days this week ahead of the IMF/World Bank meetings where there’s a general air of fractiousness-just-short-of-crisis. The global economy’s ridden the inflationary shock and the pressures on developing country sovereign debt have reduced a bit, but the Fund and Bank are struggling to address problems with climate change and financing, and sometimes getting distracted with other things. I also look at an Asia-Pacific trade dispute with some unsettling implications. Charted Waters is on gold prices. Quick question for readers this week: if you had to point at one thing the IMF or World Bank have got right over the past five years, what would it be? Answers to [email protected].

Get in touch. Email me at [email protected]

Mind the financing gap

The imperative is clear. It was set out in the experts’ report commissioned by the G20 last year. We need to reverse the net capital flows out of the developing world, encourage growth, ease debt burdens and fund the green transition. Is it happening? No.

The World Bank needs more firepower for both middle- and low-income countries and isn’t getting it (yet). As I wrote last week, it’s having another go at trying to use public money to leverage large amounts of private capital to fund the green transition in developing economies. Private finance for infrastructure in poor countries has never really happened in the past and I’m going to go out on a limb and posit that it’s unlikely to suddenly happen now, notwithstanding the flurry of activity on the subject from the new World Bank president, Ajay Banga.

You can say that doing all of this through the bank itself via a massive capital expansion isn’t realistic, but then doing it through private capital doesn’t look very realistic to me either. If we’re going to be quixotic, let’s at least be honest about it.

In the meantime, the Fund has found itself a couple of displacement activities. One, as I wrote earlier this year, is to meddle in the climate issue even if it doesn’t have the cash or policy tools to make any difference. The IMF has needlessly got itself mired in controversy about governments’ fossil fuel handouts by producing subsidy estimates that don’t make much sense — muddying rather than clarifying the debate.

The other is to issue warnings about an incipient tide of protectionism, which it did loudly at the spring meetings this year and has escalated since. The thing is, we’ve heard this before. The Fund also warned about protectionism the previous year, in 2023, and in 2022. Going a bit further back, it said similar things in 2018, in 2017 and 2016, and since you ask, also in 2012, in 2011 and in 2010.

The general sentiment is fine, of course, but the IMF doesn’t seem systematically to explain why its past warnings didn’t materialise and why nonetheless you should pay attention to the new one. The Fund cautioning about protectionism is like a doctor telling you to eat more healthily and exercise, or a fortune-teller predicting you will take a long journey and meet a stranger. It’s not wrong, but it’s not news.

Dairy me

If you were going to pitch the action thriller “TRADE WAR — THE MOVIE” to a sceptical Hollywood producer, you probably wouldn’t come up with a dispute over dairy market access between New Zealand and Canada as a hook to grab the viewer. (Even if your casting search for the two prime ministers came up with Ryan Gosling as Justin Trudeau and Russell Crowe as Christopher Luxon.)

Still, despite the general vibe of niceness around the two countries, New Zealand’s announcement last week, that it would escalate a case under the Asia-Pacific CPTPP agreement to compulsory negotiation, was significant, and — surprise! — not great news for rules-based trade.

New Zealand originally brought the case against Canada over access to its dairy market in 2022 and won a ruling the next year. This latest development involves Ottawa’s failure to comply and reflects increasingly open frustration from Wellington.

Dairy, of course, is a politically sensitive issue at home thanks to the concentration of the industry in Quebec and the manoeuvrings of the Bloc Québécois. Canada has dairy like the US has the Jones Act, the EU has GMO crops and India has, well, most things. New Zealand also won cases against Canada over dairy in the WTO and encountered similar difficulties with getting them adhered to. The Canadian government expressed defiance against New Zealand last week, of course, but their hearts don’t really look in it.

This case is the first under the CPTPP’s dispute settlement process since the pact went into force in 2018. Impasse wouldn’t bode well for the thesis that a vigorous regionalism among like-minded free-trade countries can supplant the moribund multilateral system. Nor does the air of disunity bode well for the extremely tricky question of how the members deal with China’s application to join.

It’s particularly bad given New Zealand and Canada are supposedly like-minded internationalists on trade. Canada’s claim to be a defender of the rules-based system looked somewhat credible when it set up the Ottawa Group of countries in 2018 to explore ways of keeping the WTO alive. It looks considerably less so now that it has flouted WTO rules under pressure from the US by imposing huge tariffs on Chinese electric vehicles. It’s also drifting towards the Dark Side on carbon pricing, putting itself on the wrong side of future debates about climate and trade.

We’ll see what happens, but at the moment it looks like this case is heading towards New Zealand imposing countermeasures on imports from Canada. It’s hardly a huge amount of money or a vital part of world trade, but it’s not a good look.

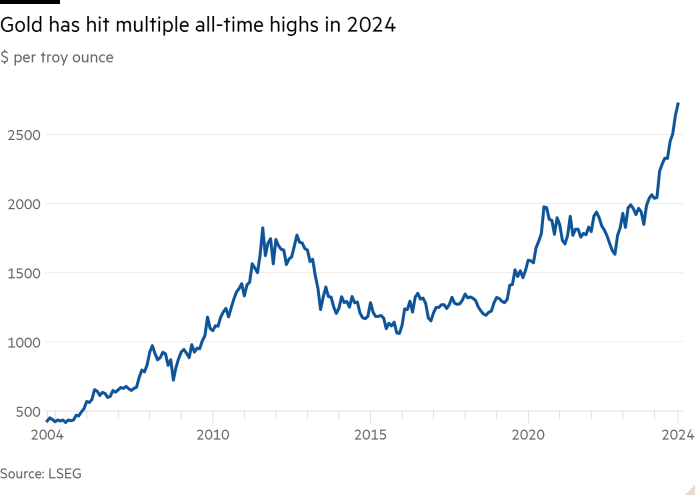

Charted waters

The price of gold is shooting higher, despite inflation and inflation expectations heading down. Is this surprising? Is gold’s age-old role as an inflation hedge coming to an end? No. It’s never been a good inflation hedge and no one knows why it goes up and down. Don’t sweat it.

Trade links

-

The FT’s tracking index for global economic recovery shows that political and economic uncertainty are dragging on confidence and growth.

-

The economist Brad Setser argues that the real threat to globalisation comes from unhealthy integration rather than fragmentation.

-

Adam Posen of the Peterson Institute warns about the dangers of Donald Trump’s election.

-

The Unhedged team interviews former Trump economic adviser Kevin Hassett on the policy of reciprocal tariffs.

-

The UK needs a more constructive approach to rebuilding its relationship with the EU, says the FT’s editorial board.

Trade Secrets is edited by Harvey Nriapia

Recommended newsletters for you

Chris Giles on Central Banks — Vital news and views on what central banks are thinking, inflation, interest rates and money. Sign up here

Europe Express — Your essential guide to what matters in Europe today. Sign up here