Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

This article is an on-site version of our Unhedged newsletter. Premium subscribers can sign up here to get the newsletter delivered every weekday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Good morning. AI has played a big role in the research that won the Nobel Prizes for chemistry and physics, and yesterday it was announced that frequent AI commentator Daron Acemoglu won the Nobel Prize for economics. Is this more evidence of an AI halo? Or proof that AI is the real deal? Email me: [email protected].

Robotaxis

Last Thursday, Tesla hosted a glitzy showcase of its future offerings. Investors and the press were served drinks by Tesla’s humanoid Optimus robots, while Elon Musk gave the world its first official look at the “Cybercab” and “Robovan”: driverless, pedal-less autonomous vehicles designed for Tesla’s “robotaxi” fleet, which will allow riders to hail self-driving cars.

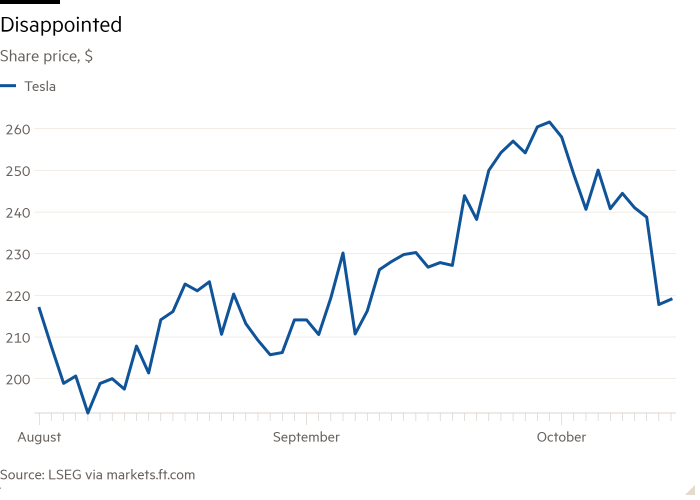

The market was . . . disappointed. Tesla stocks fell 8.8 per cent on Friday, and only partially recovered yesterday:

The reasons for disappointment varied (and were well documented by our colleagues in Alphaville). Little detail was provided about its cheaper Model 2, which investors had hoped might lift near-term earnings. Some felt the joyrides in the new vehicles were less than thrilling. And, as it turns out, the self-functioning robots were not so self-functioning.

Others were let down by the robotaxi offering itself. A lot of Tesla’s previous reports and press conferences have focused on Tesla’s full self-driving (FSD) software and the rollout of its robotaxi fleet, particularly the latter’s potential to obviate public transportation and unseat ride-sharing services such as Uber and Lyft — both of which saw their stocks surge as Tesla’s fell on Friday. As noted by our Lex colleagues, estimates for the expected value of the robotaxi market can range, but are very, very high: ARK Investments and Musk put it between $5tn and $8tn, while the more conservative RBC Capital Markets estimates it to be $1.7tn by 2040. In our piece from July, in which we tried to break down Wall Street’s earnings expectations for Tesla, we attributed $32bn of revenues to FSD software sales and robotaxis by 2029.

Tesla is not the only company trying to capture that market, though. It is up against Waymo, the autonomous driving company spun out of Google; Cruise, General Motors’ autonomous ride-hailing service; and Zoox, Amazon’s self-driving subsidiary. Is it possible that Friday’s market reaction was proof of investors feeling that Tesla may be losing the race? Some things that stuck out from Thursday’s presentation and investors’ and analysts’ reactions:

-

Timeline: Musk initially promised a robotaxi fleet as early as 2018. During Thursday’s event he wavered: “We expect to be in production for the Cybercab, which is highly optimised for autonomous transport, in . . . well, I tend to be optimistic about timeframes, but in 2026 . . . before 2027, let me put it that way.”

He committed to having some of the FSD capabilities for newer models available by next year in Texas and California, meaning that car owners or Tesla itself could potentially use FSD for taxi services. But it seems like Tesla’s official fleet of Cybercabs will not be up and running for a couple of years. Meanwhile, Waymo is already operating taxi fleets in four cities; one analyst told us they are “essentially ubiquitous in San Francisco”. It is also licensing its technologies to other companies and manufacturers. Cruise is operational in two cities, though it has hit some compliance and safety snares, and Zoox is testing its fleet in two states.

-

Compliance: One of the issues Cruise has run into is its proposal for a car without a steering wheel or pedals. Though the National Highway Traffic Safety Administration allows vehicles without either, Cruise paused production of its own offering after failing to get permission to scale production past 2,500 pedal-less vehicles per year. In a note to investors, TD Cowen states that Tesla’s ability to produce its own pedal-less, wheel-less Cybercabs could be “limited” given NHTSA’s previous production cap.

The same TD Cowen note also states that Tesla’s technological approach might not meet safety standards. While Waymo and Cruise use Lidar, a remote sensing technology, Tesla prefers to use cameras and machine learning, arguing it is the superior and more cost effective technology. TD Cowen sees Tesla’s refusal to adopt Lidar as “a potential regulatory hurdle longer term” and one that will certainly raise the cost of the vehicle if the NHTSA requires Tesla to adopt Lidar.

-

Cost: On Thursday, Musk said the Cybercab would cost about $30,000, approximately the same price as its cheaper Model 3 and Model Y. But he also said that it would not have a charging port, instead using inductive charging — which Tesla does not currently have infrastructure for, raising the cost of the rollout. He also said that running the Cybercab would cost $0.20 per mile and will charge about $0.40 a mile. But the current average cost of owning and operating a vehicle in the US is $0.81 per mile, and $0.40 seems very low. Musk’s cars would have to show significant cost reductions, or Tesla may have to raise the price closer in line with existing ride hailing services.

Unhedged does not pretend to know whether Tesla will win the race for autonomous fleets. As SpaceX’s booster-catching feat showed, Musk’s companies often achieve things that were once thought to be impossible. And while it seem to us that these are pretty steep hurdles and evidence that Tesla may be falling behind, some analysts we spoke with actually saw these as strengths. For instance, Edison Yu of Deutsche Bank told us that although Tesla might need to raise the price of the Cybercab and add Lidar in the short term, its camera-based technology was a long-term edge:

Waymo has taken a very long time to scale because, though it has some AI capabilities, it has to map entire cities and code for driving cases. That is hard, as opposed to running the data through a black box model like Tesla does. This will all come down to who can scale faster. Scaling software [such as Tesla’s] is the more efficient and lucrative approach.

Tesla already has a lot of training data from its semi-autonomous driving function. Once FSD is up and running and Cybercabs are under production, it may prove to be the safer offering and quickly capture market share.

Wall Street’s consensus estimate for Tesla’s 2029 revenue has fallen $10bn since we wrote our piece in July. Though we will not get new estimates based on Thursday’s event for a while, some investors think there will not really be an effect, as they already did not assume that Tesla would deploy its fleet in the next few years. Tom Narayan at RBC Capital Markets said, “2030 is not the bogey when we are dealing with robotaxi. It was disappointing to not get concrete numbers [on Thursday], but I don’t have Optimus or Robotaxi [generating revenue] in my forecasts for a couple of years anyway.”

One good read

Should we just give up?

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

Chris Giles on Central Banks — Vital news and views on what central banks are thinking, inflation, interest rates and money. Sign up here