It’s a tough time to be a first-time buyer: you need a big income, a massive deposit and a marathon-term, 35-year plus mortgage. And if you manage all that, the chances are you won’t benefit from rapidly rising house prices as previous generations did.

Cue the cavalry horn: in recent weeks lenders have made a flurry of announcements suggesting they have the solution. Several are now offering to lend borrowers up to 5.5 times their income (compared with the usual 4.5 times limit). Nationwide is going even further, with an offer of six times income, and at up to 95 per cent of the value of the home.

The day is saved. Or is it? Because, while these products appear to be just what potential first-time buyers need, the reality is that due to the Bank of England’s lending criteria, they’re likely to achieve very little — and could even store up serious problems down the line.

When it comes to mortgage market regulation, there is always a tension between financial stability and trying to increase home ownership. Unsurprisingly, periods of looser lending criteria have tended to accompany rising rates of homebuying, from the 100 per cent loan-to-value (LTV) and endowment mortgages of the 1980s — which coincided with an uptick in home ownership — to the income self-certification mortgages of the 2000s — when it peaked at 71 per cent of households.

Since the financial crisis, the rate of home ownership has declined — and the idea that people could self-certify their income on their mortgage application has looked absolutely crazy. The balance has shifted towards financial stability: higher loan-to-value lending has been limited and potential borrowers have their bank accounts closely examined.

As for lenders, they’ve been restricted in how many higher loan-to-income (LTI) loans they can issue. Only 15 per cent of their new loans could be above 4.5 times income but, given the challenge of managing the flow, the actual figure peaked at around 10 per cent.

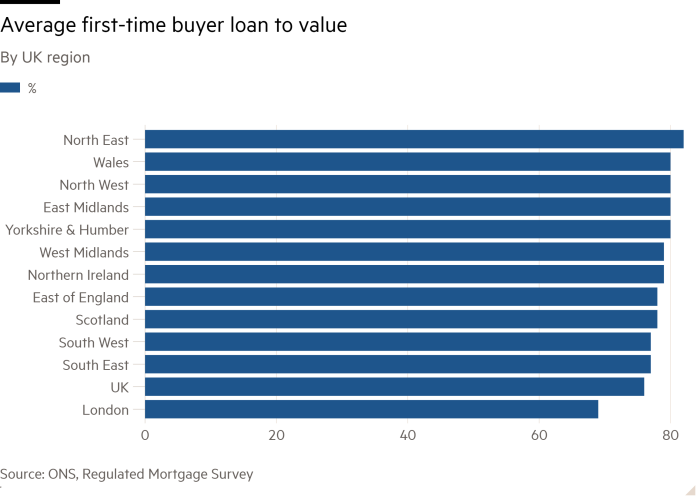

As a result, mortgages with high LTI and LTV ratios push the borrower into a section of the market where mortgage availability is heavily restricted and loans come with higher interest rates — therefore, despite having the biggest deposit barrier, first-time buyers in London have the lowest average LTV ratio of all regions as they aren’t able to afford the repayments on larger mortgages.

So there’s clearly an appetite for these new first-time buyer mortgages. The problem is, while interest rates are where they are, people won’t be able to afford them.

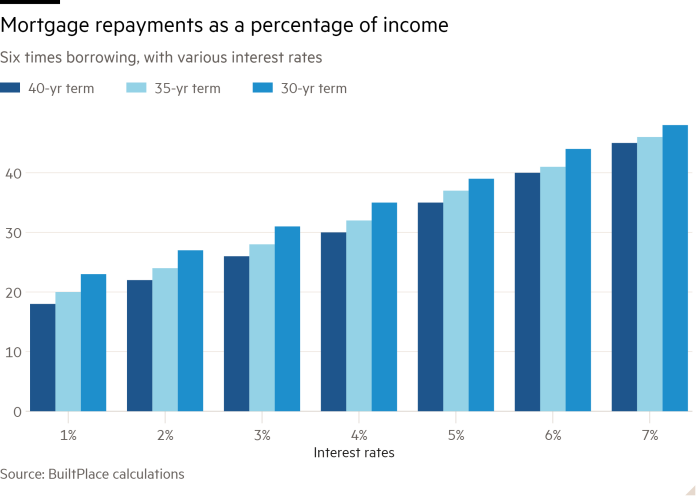

Repayment affordability depends on the mortgage interest rate, loan-to-income ratio and term. Despite the increasing prevalence of 40-year mortgages in recent years, the rise in rates has been substantial and the impact on borrowers’ loan-to-income ratios is clear — they have fallen sharply.

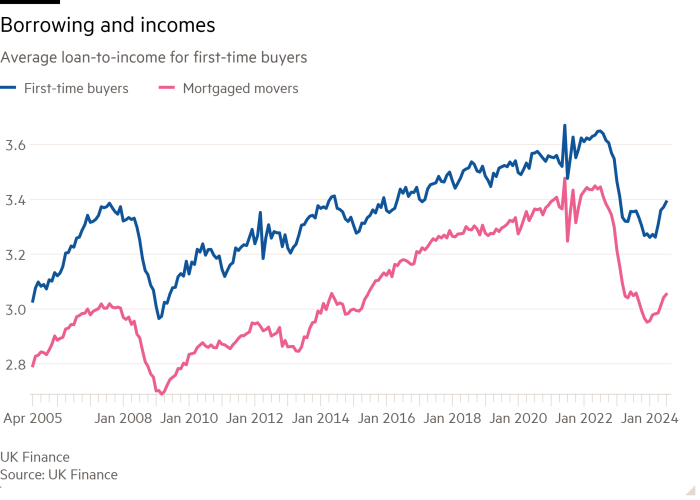

Average loan-to-income ratios for both first-time buyers and mortgaged movers have fallen since 2022. In the first three months of the year, just 5 per cent of loans were above 4.5 times income, according to the BoE, well below the usual 10 per cent or so. Even with a rate of 4.99 per cent and a mortgage term of 40 years, a six times income mortgage would cost 35 per cent of gross income — that’s double what the average first-time buyer was paying in mid-2022 and expensive even for most private renters.

Paying more than 30 per cent of gross income on repayments has typically been seen as the “danger zone” where arrears rise sharply, but recent research warns that even above 15 per cent the risk of payment shortfalls increases significantly.

Given the risks and regulation surrounding higher LTI mortgages, getting one of these “danger zone” loans may be an impossible dream for all but a few buyers. Current mortgage rates will be a further limit — it would take a 2 per cent rate to bring the repayment ratio down on a six times income mortgage to the current average for first-time buyers — and these new products may have already generated more headlines than they will new homeowners.

Regardless of how successful these mortgages are now, they are a clear signal of the direction that lenders are charting. They have an eye to lower mortgage rates in the future, with many already offering sub 4 per cent deals. Some retail-funded lenders — those with savers’ deposits to lend against — may be taking the chance to squeeze competitors that rely on financial market interest rates.

As a result of falling rates, average loan-to-income ratios have already recovered slightly from their lows at the start of the year — and lenders appear very keen to increase their lending above the 4.5 times income limit when mortgage rates allow. They clearly hope that by focusing on first-time buyers they will persuade regulators it is a sensible decision.

Lenders are feeling more optimistic about their chances — and there are arguments in their favour. The first is that younger buyers may be more likely to benefit from wage growth thanks to career progression. That could quickly reduce the LTI ratio from its initial high level by the time their fixed rate period ends. The second is that the fallout from higher rates has been relatively well contained over the past two years: arrears and repossessions have risen, but are well below 2009 levels.

This suggests that perhaps the balance between home ownership and regulation was tilted too far towards the latter. With the new government targeting an increase in home ownership, easing lending restrictions will be a tempting opportunity for quick wins.

If these regulatory barriers ease and mortgage rates fall further in the coming years, prospective first time buyers may welcome having access to these higher LTI mortgages. However, there remains a bigger question. If this market does take off, will it also compromise the prospects of future generations by further reinforcing high house prices?

Whether the housing market is in a boom or bust, first-time buyers are the one group always motivated to purchase — especially given the shocking state of the private rented sector. They have an incentive to maximise their purchase price by borrowing as much as possible — and, given that the broken housing ladder makes it much harder to trade up to a larger home these days, it can make sense to stretch their finances to the max for that first home. If these products become more popular and you’re not using them — or cannot access them as a lower income borrower — there’s a chance you’ll miss out.

Higher house prices will clearly be bolstered by increased competition and bigger mortgages in a supply-constrained market. The higher LTI mortgages that flow from these prices come with more risk and marathon mortgage terms — costing more in interest and limiting access to older borrowers locked out of 40-year deals. And the broader point is that those higher repayments could be spent elsewhere in the economy.

There’s no single answer to finding the right balance of risk versus access to home ownership, but it’s one the new government and regulators will unquestionably need to address.

Neal Hudson is a housing market analyst and founder of the consultancy BuiltPlace