This article is an on-site version of our Chris Giles on Central Banks newsletter. Premium subscribers can sign up here to get the newsletter delivered every Tuesday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Consumption matters. Ultimately economic success is determined by how much people consume, however much Germany and China might measure their economic prowess by exports or the UK might fret about low investment. The purpose of investing or exporting is ultimately to enable people to consume more goods and services, whether these are private, such as a restaurant meal, or public, such as national defence.

Post-pandemic, the trends in real private consumption are remarkable. US spending has recovered to its previous trend levels, which were themselves a lot more dynamic than those in the Eurozone or Japan and a little faster than the UK.

In contrast, as the chart below shows, real levels of consumption in the Eurozone, Japan and the UK have been flat. On past trends, that is not much of a surprise for Japan with low growth and a declining population, but it shows much more lasting damage from the pandemic in Europe and something of a catastrophe in the UK relative to past trends.

The chart requires some explanation and some thought about monetary policy among central banks. First of all, it is important to note that growth in real household incomes does not explain the differences — these have been weaker in the US than the OECD average over the past two years and real wage growth has risen unambiguously only for lower income US workers.

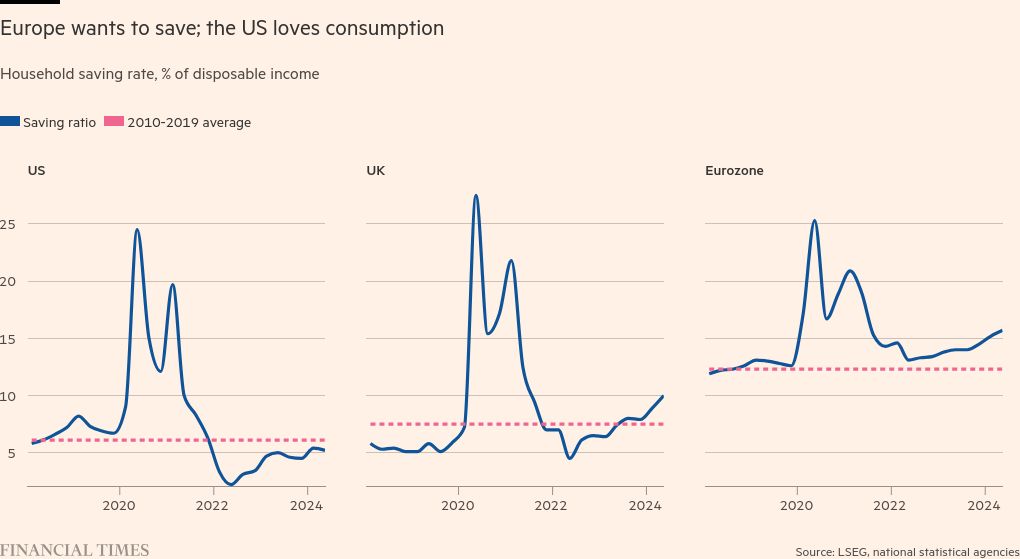

Instead, the big difference between the US and most other economies has been a drop in savings compared with the pre-pandemic period. Europeans got spooked by Covid-19 and its aftermath, while this appears to have been a minor inconvenience for US households.

My colleagues Valentina Romei and Sam Fleming explored this issue in detail over the weekend. In all parts of the world, savings rates surged when coronavirus was rife because households were unable to spend, especially on consumer-facing services, but dropped below long-term trends in the US, while staying much higher in the Eurozone and the UK.

Part of the reason for these massive differences in savings trends is likely to be related to greater pandemic and post-pandemic fiscal largesse in the US leaving American households with less of a repair job to do on their own finances. Part of the explanation clearly reflects the fact that Europe had a much worse external shock post pandemic, with the Ukraine war on its doorstep and a natural gas price energy hit that dwarfed what was experienced in the US. European consumers are still suffering from wholesale gas prices roughly twice the pre-2022 rate, so it is natural that they have made some adjustments.

Important as these two issues are, they were factored in to European Central Bank forecasts by June 2023, when the central bank expected 1.9 per cent consumption growth in 2024. By September this year, it expects only 0.8 per cent growth, demonstrating that real income gains across Europe are simply not translating into spending as expected. As long as inflation is under control, this must be dovish for Eurozone and UK interest rates.

Added to this is the fact that while Europe has a huge range of mortgage structures in different countries and vastly different household balance sheets, the transmission of high interest rates to spending is likely to be a little larger than in the US. (See last week’s speech by ECB executive board member Isabel Schnabel for more on these differences).

The caveat to this prescription of looser monetary policy in Europe is that the natural gas price shock suffered across the continent not only made consumers more cautious but also made them more determined to protect their real wages at a time of low productivity growth, which has probably generated more persistence in inflation. The conundrum is that Europe needs to loosen monetary policy more than the US but also must worry more about its inflation trends. It is a nasty combination.

If that is the big picture, data revisions in the US and UK have added some additional insights over the past few weeks.

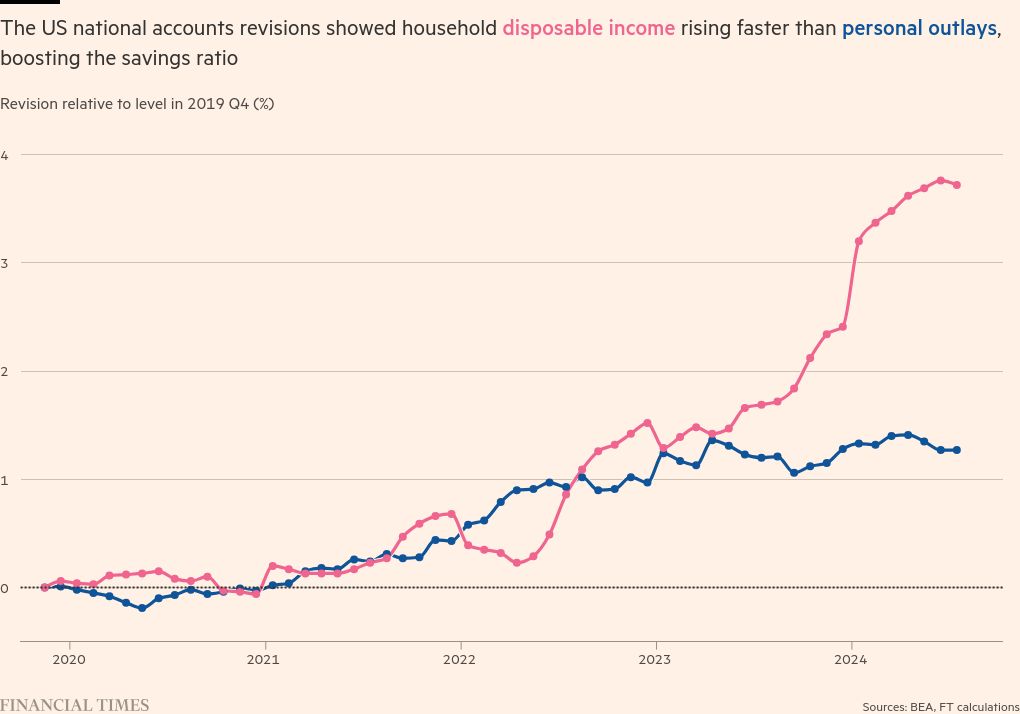

The US story has become brighter still. When the Bureau of Economic Analysis revised its national accounts at the end of last month, it raised the measured US savings ratio to around 5 per cent during 2024 from about 3 per cent in the previous releases. The chart below shows the extremely benign reasons for the upward revisions in savings. Compared with the pre-pandemic level, US disposable incomes have been revised sharply higher — almost 4 per cent up this year, while spending was also revised up but not as much.

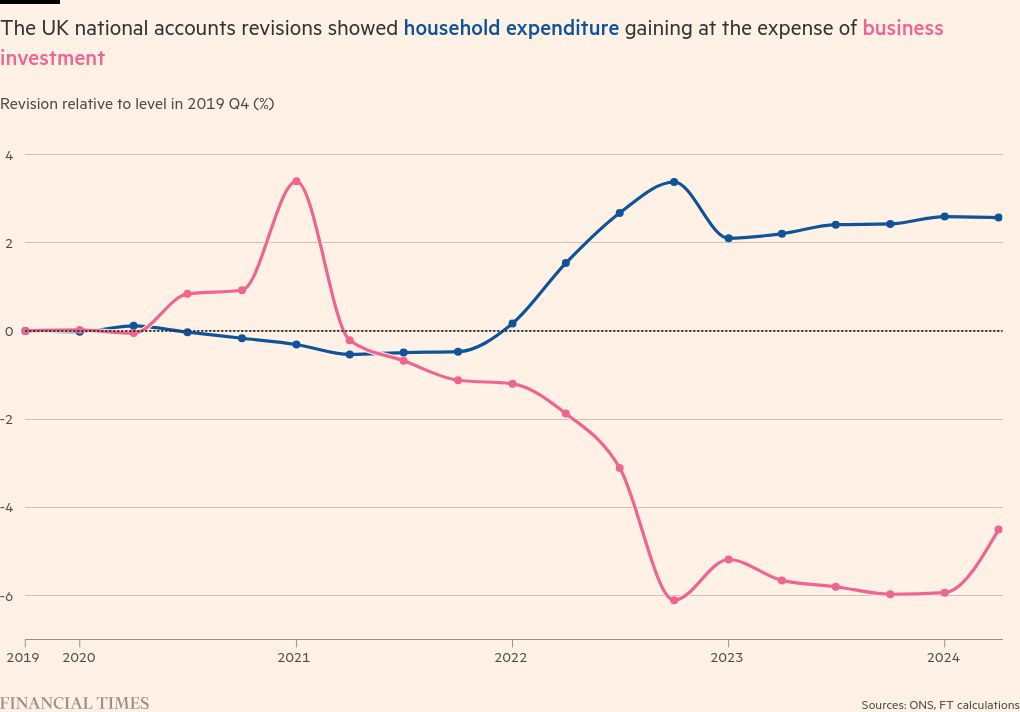

In contrast, revisions to the UK national accounts depressed the savings ratio by roughly 2 percentage points because spending was revised higher while incomes and GDP were broadly unrevised. Where did that increased private consumption come from? Lower business investment.

In an economy where people already worry that investment is not sufficient to maintain future consumption, the chart below showing these revisions is not exactly encouraging.

Apart from the fact that the US immediate economic environment is healthier than in Europe (we know), there is one important conclusion you should take from this analysis — Europe should be cutting interest rates and stimulating private consumption more than the US.

But Europe struggles to do this because the same shock that has undermined consumer spending has also made inflation a little more persistent.

A threat to central bank independence

Imagine the scene in early November if Donald Trump wins the 2024 US presidential election. He meets Federal Reserve chair Jay Powell and says afterwards: “I don’t believe the environment is ready for interest rates to stay at this level.” Everyone would shout: “Trump threatens central bank independence.”

This happened in Japan last Wednesday when new Prime Minister Shigeru Ishiba told reporters, following a meeting with Bank of Japan governor Kazuo Ueda, that “I do not believe we are in an environment that would require us to raise interest rates further”.

Cue a Japanese stock market rally, a drop in the yen and the inevitable revision from Ishiba of what he meant a day later. It was all a misunderstanding, he told reporters, and he was merely reflecting Ueda’s own view that the BoJ could take its time to assess the impact of its two rate hikes before deciding on another one.

It was a rapid lesson in the simple politics of talking about interest rates. Don’t.

What I’ve been reading and watching

-

In a hawkish dissent from current fashions, Andréa Maechler, deputy general manager at the Bank for International Settlements, warned last week that central banks should “exercise care” when assuming supply shocks are transitory. Raising interest rates to prevent a transition to persistently higher inflation regimes is safer, she suggested. Full speech here

-

Hurrah — Turkey’s inflation rate has fallen below 50 per cent. Anecdotes are awful, but having spent two weeks in the country I did not see any signs of rampant inflation which, for an economist, was mildly disappointing

-

Europe will get a little more inflationary after imposing tariffs on Chinese electric vehicles; the US a little less so after dockworkers suspended their strike action

-

On the anniversary of the October 7 Hamas attacks, rising tensions in the Middle East have pushed oil prices up again

A chart that matters

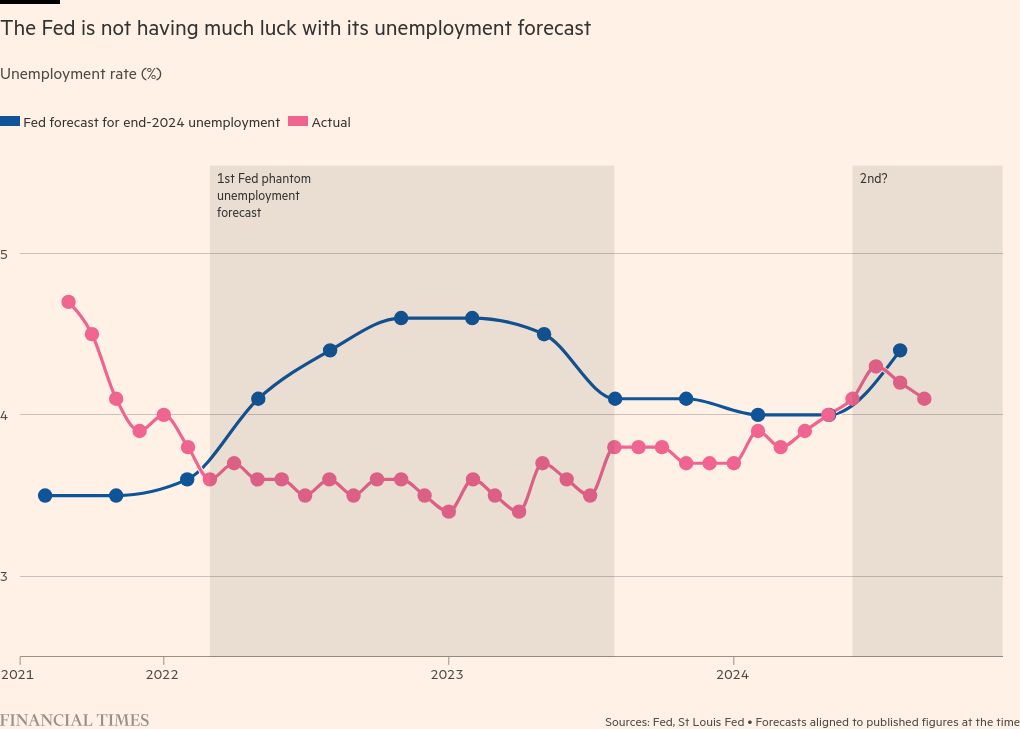

There is little doubt that last week’s US jobs numbers were excellent. The unemployment rate dropped to 4.1 per cent in September from July’s peak of 4.3 per cent. Payrolls beat expectations to rise by 254,000 in the month, with upward revisions to July and August too. No wonder the New York Fed president told the FT this week that the data was “very good”.

What was good for the US economy — low inflation and low unemployment — was not so great for the Federal Reserve’s analytical capabilities, however. As the chart shows, the Fed is pretty clueless about trends in US unemployment.

The chart shows the Fed’s forecast for end-2024 unemployment at the time the forecasts were made against the actual rate. In 2022, it expected monetary tightening to raise unemployment. That did not happen and the Federal Open Market Committee threw in the towel in September 2023, expecting unemployment to stay low. Then, the actual rate crept up and just at the moment FOMC members raised their forecasts to reflect this, the data immediately fell back again.

The chart below shows the perils of data dependency. Of course, no one should be complaining that the summer rise in unemployment was a bit of a blip. But the Fed did not see this coming.

Recommended newsletters for you

Free lunch — Your guide to the global economic policy debate. Sign up here

Trade Secrets — A must-read on the changing face of international trade and globalisation. Sign up here