Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

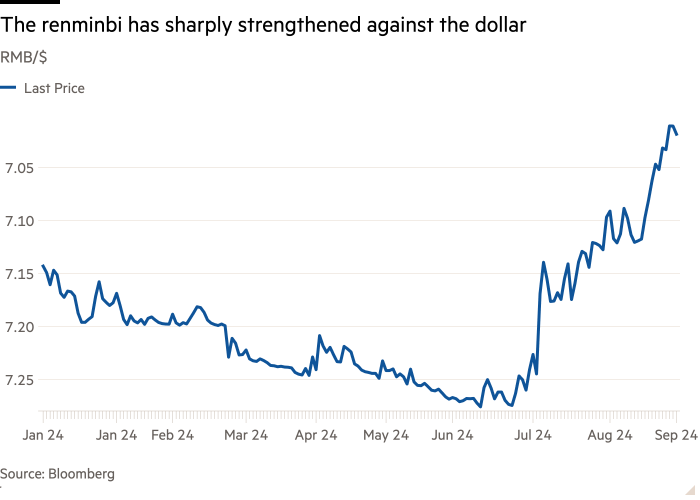

A strong rally in the renminbi is testing Beijing’s currency management policies, after China’s stimulus plans and the US Federal Reserve’s embrace of lower interest rates sent Asian currencies surging against the US dollar.

The renminbi’s spot exchange rate has moved tightly in sync with an official “fix” set by the central bank in recent weeks, indicating that Beijing is reasserting control of the currency as the US presidential election looms.

The People’s Bank of China kept the official rate at between 7.1 and 7.2 to the dollar for most of this year even as the spot renminbi stayed at the bottom of a 2 per cent trading band around the fix.

But in the past month it has allowed much more movement in the fix as the renminbi rose to 7 against the dollar on a spot basis, a sign that Beijing is engineering a controlled appreciation to smooth the effects of a rush back into Chinese assets from abroad.

“While Chinese authorities likely welcome the shift away from the relentless renminbi depreciation pressures which existed during the most of 2023 and 2024, it is likely that they are also keeping an eye on the pace of further appreciation,” said Nathan Swami, head of FX trading for Asia Pacific at Citi.

Swami added that a further rise in the currency could undermine the competitiveness of Chinese exporters who hold significant amounts of US dollars.

This year the central bank has disguised its market interventions by pushing state banks to buy dollars during rises in currency markets, such as the August collapse in carry trades. State banks’ net foreign assets rose that month, in a sign that such interventions were likely to have taken place.

China’s offshore renminbi, which trades more freely than its onshore counterpart, late last month dipped below 7 to the dollar for the first time since May 2023 as authorities launched a stimulus blitz in order to revive the economy and animal spirits in the country’s capital markets.

The strong rise in the offshore currency confounded many foreign investors who had taken short positions. Analysts at Goldman Sachs last week closed their short recommendation for the currency, noting that the stimulus “appears to be squeezing the remaining [renminbi] shorts”.

One trader at a big western investment bank said they had seen the currency’s rally exacerbated by investors closing out their short positions.

“As the authorities do more to support growth, the renminbi strengthened on the back of that,” said Manik Narain, head of emerging markets strategy at UBS, who pointed out that at just over 7 to the dollar the renminbi nonetheless remains “closer to its 10-year low than its 10-year high”.

Analysts said Beijing was also likely to keep a tight grip on the currency through a US election that could drastically alter the dollar’s path, if voters back Donald Trump’s policies of high tariffs that could weaken China’s export economy and strengthen the greenback.

“As the US presidential election approaches, some probability of higher US tariffs being imposed on China afterwards needs to be priced into the currency,” said FX strategists at Macquarie. “Even if those tariffs do not ultimately materialise, China’s own domestic struggles still argue for ongoing [currency] weakness until policy stimulus begins to bear fruit.”

“On the eve of the US election, we expect [the offshore exchange rate] to settle nervously near 7.10, lunging higher towards 7.30 by early 2025 on a possible Trump victory, or descending to 6.95 if [Kamala] Harris wins instead.”

But China’s dollar war chest remains formidable.

China’s foreign reserves stood at about $3.3tn in September and many of its exporters have amassed dollars from business abroad. Chinese state-owned banks were last week reportedly buying dollars on the onshore market in order to slow the rise of the renminbi.

The Malaysian ringgit, Thai baht and Indonesian rupiah have also surged in recent weeks as the Fed’s September rate cut sent investors looking for high-yield assets in Asia. Despite a rebound for the dollar amid an escalating conflict in the Middle East, many analysts expect continued appreciation for Asian currencies.

“The tide is reversing for weak Asian currencies, and given the fact the US pressure cooker is no longer there, we are on the descent of the dollar,” said Trinh Nguyen, senior economist for emerging Asia at Natixis.

Nguyen added that a stronger Chinese economy could benefit other Asian currencies, especially those of countries that count China as a top trading partner such as Indonesia or whose tourism economies partly depend on Chinese visitors such as Thailand.

“Chinese consumers will open their wallets if they feel more confident. These factors are quite supportive for emerging Asia.”