Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Southern Water, the heavily indebted utility controlled by Macquarie, has turned to investors for nearly £4bn in borrowings over the next five years at a time when water companies are under increasing pressure in debt markets because of the crisis at Thames Water.

Thames Water, which itself was formerly owned by Macquarie, was last week downgraded to the lowest reaches of junk because of its dwindling cash position, increasing further scrutiny on other utilities in the sector with strained finances.

While Southern is not in the same degree of financial peril as Thames Water, its investment-grade rating and its debt covenants have both come under pressure as the group’s total debts have exceeded £6bn, according to its most recent group accounts. Of that total, liabilities related to derivatives have ballooned past £1bn.

The yield on Southern’s short-dated bonds, due in 2026, has more than doubled over the past six months to reach 13.5 per cent, as investors now require a hefty premium to hold debt that would usually offer far smaller returns due to its near maturity.

The water monopoly, which serves 4.7mn customers in the south-east of England, met bond investors in recent days to update them on its credit situation and business plan.

In a presentation to debt investors published on its website, it revealed it planned to raise £3.8bn of debt over the next five years, telling them it had a “proven track record of capital raising”, having raised £550mn of fresh equity from Macquarie in the last financial year.

The utility also needs to raise £650mn in equity as pressures mount on its credit ratings and operating business, which is struggling with sewage pollution and potential water shortages.

The investor presentation comes after Moody’s in July put Southern’s credit rating on review for downgrade, putting it at risk of losing its investment-grade status with one of the major agencies.

Despite Macquarie having already injected hundreds of millions of pounds, “there is no certainty that it would make further contributions if the final determination makes continued low returns likely”, Moody’s said.

Southern’s chief financial officer Stuart Ledger said at the time of the downgrade that the utility had “an excellent liquidity position”.

However, in August 2023, the company’s lenders had to waive a loan covenant breach after its credit ratings and its interest coverage ratio, a measure of a company’s ability to pay its debt, fell below key thresholds.

Lenders agreed to waive these conditions until 2035, meaning Southern can continue to draw down all of its available borrowing facilities and raise new financing, while also allowing the utility to increase the limit on its gearing — a critical measure of debt-to-equity — from 74 to 75 per cent.

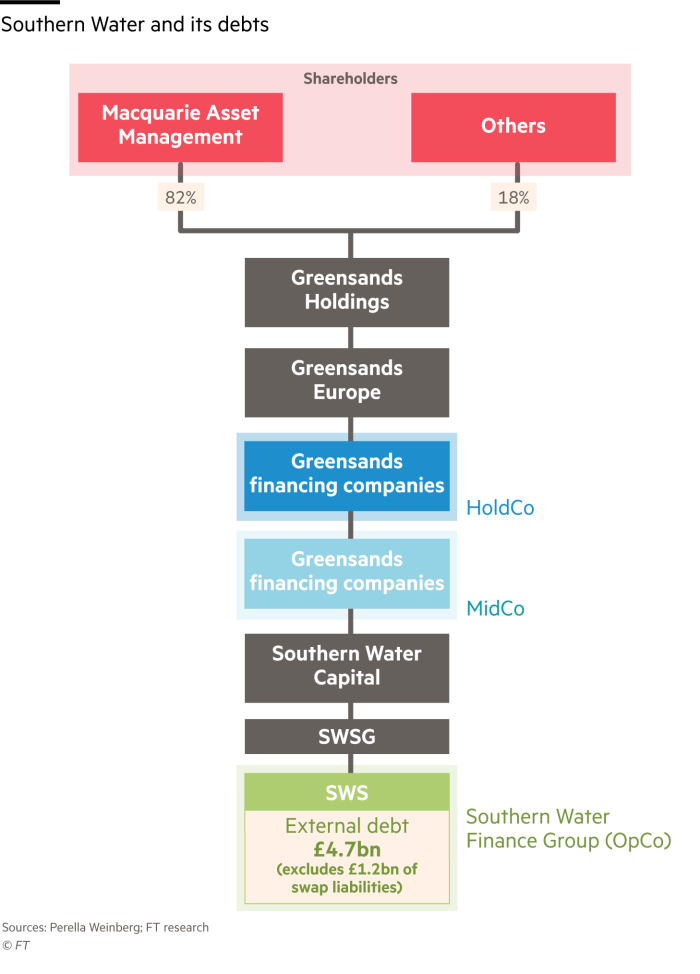

Within Southern’s complex structure, the regulated operating company, a “ringfenced” group that is supposed to be protected from stress at the holding companies above, is nevertheless running with gearing of about 70 per cent.

While lower than Thames Water’s gearing of about 80 per cent, the £4.7bn debt pile at Southern’s operating company, which makes up the group’s reported debt-to-equity ratio, leaves out almost £1.2bn of liabilities relating to its inflation-linked swaps.

These are not reported in the utility’s regulatory numbers, but if included, they would take the company’s gearing level to more than 85 per cent. Were the company’s creditors to demand a payment acceleration upon a default, Southern Water’s inflation-linked swaps would rank ahead of principal and interest on its senior debt.

The presentation also shows that Southern is asking water regulator Ofwat to allow it to increase the average annual household water bill to £734 by the end of the next regulatory period, higher than Thames Water and three other water companies cited as comparisons.

Thames Water, which saw investors backtrack on a commitment to provide £500mn of equity in March, became the first regulated water utility to lose its investment-grade rating when both Moody’s and S&P cut its credit rating.

While an equity injection at Southern Water from Macquarie could ease pressure on its operating company, its holding company also has £300mn of debt maturing next year. Representatives of Macquarie told investors at the meeting that it might need to negotiate an extension on this debt, according to one person who attended.

Thames Water’s holding company Kemble, which itself was established by Macquarie during its 2006 buyout of London’s water company, defaulted on its own debt in April, after its present shareholders backtracked on a pledge to put in fresh equity into the business.

Southern Water said the group had strong liquidity and was working towards a positive regulatory settlement. Macquarie declined to comment.

Southern Water’s finances under scrutiny

July 2021

Southern Water fined a record £90mn for dumping untreated sewage into the sea

august 2021

Macquarie takes over Southern Water in a deal agreed with regulator Ofwat

July 2023

Southern Water suspends dividend payments until at least 2025 as Fitch downgrades its debt to triple B

August 2023

Lenders agree to waive Southern’s covenants

October 2023

Macquarie injects £550mn in equity into Southern Water

July 2024

Moody’s puts Southern’s credit rating on review for downgrade

september 2024

S&P and Moody’s downgrade Thames Water’s credit rating