Latest news on ETFs

Visit our ETF Hub to find out more and to explore our in-depth data and comparison tools

Actively managed funds have taken more than 70 per cent of the management fee income accruing from net flows into US-listed exchange traded funds so far this year.

The figure, calculated for the first time as a result of this FT investigation, is a shot in the arm for an active fund industry that has been on the back foot as cheaper, passive index-tracking funds have seized an ever larger share of investors’ money.

Assets held in passive US ETFs and mutual funds surpassed those of active funds for the first time at the end of last year, according to Morningstar, after active funds suffered $450bn of outflows in 2023, even as passive ones took in $529bn.

But after initially ceding the fast-growing ETF market to passive funds, active managers are fighting back. Having embraced ETFs en masse, active ETFs have accounted for 28 per cent of net flows into US-listed ETFs this year, well ahead of their 8 per cent of assets.

And thanks to their far higher fees, this has translated into active ETFs grabbing 72 per cent of the management fee income emanating from the $588bn of fresh money piling into US ETFs in the first eight months of the year, according to calculations by Morningstar.

“Investors are increasingly embracing actively managed ETFs and while active ETFs are typically available for a lower fee than their mutual fund counterparts they are offered at a premium cost relative to broad index based strategies,” said Todd Rosenbluth, head of research at consultancy TMX VettaFi.

“Money is increasingly going into active ETFs and those fees are higher.”

Bryan Armour, director of passive strategies research for North America at Morningstar, said index-based investing “has largely been commoditised, which has forced asset managers to grow fee revenue elsewhere”.

“Actively managed alternatives ETFs have been the primary beneficiaries from that shift, especially for crypto ETFs and options-based strategies, like covered call and buffer ETFs,” he said. “You can accept low assets, if you have a high-fee product.”

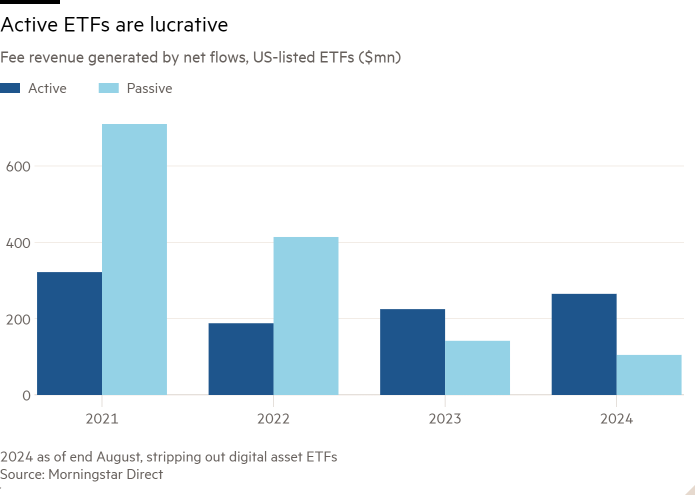

US-listed active ETFs generated $265mn of fee revenues from net flows in the first eight months of 2024, according to Morningstar data, well above the $105mn generated by passive ETFs.

This represents a sharp turnaround from 2022, when passive ETFs soaked up 69 per cent of the net new fee revenue, although the shift began last year when actives took the lead with a 61 per cent share.

The 2024 data has been calculated stripping out digital asset ETFs, principally the raft of spot bitcoin funds that launched in January.

If these cryptocurrency ETFs are included then the swing towards active is starker still. On that basis, active ETFs have generated $278mn of fee revenue from net flows this year, while passive ones have actually seen fee revenue decline by $26mn. *See methodology

This discrepancy is largely driven by the passive Grayscale Bitcoin Trust ETF (GBTC), which has had outflows of $20bn which, with its outsized 1.5 per cent fee, has translated into lost revenue of $152mn, more than outstripping the gains of all other passive ETFs, according to Morningstar.

“That’s a massive loss of fee revenue for Grayscale. It actually pushed the entire passive category negative, which is wild,” said Armour.

Two other bitcoin funds, the iShares Bitcoin Trust ETF (IBIT) and Fidelity Wise Origin Bitcoin ETF (FBTC), figure among the top 10 revenue winners this year. However, although they have amassed $30.9bn between them, their far lower fees of 0.12 per cent and 0.25 per cent respectively have translated into revenue gains of only $11.5mn and $12.7mn respectively.

More successful in this regard has been Volatility Shares’ 2x Bitcoin Strategy ETF (BITX), which Morningstar classifies as an active product. It may only have taken in $1.9bn, but with a fat fee of 1.9 per cent this equates to a $14.3mn gain.

Other big active winners by this metric have been the BlackRock US Equity Factor Rotation ETF (DYNF), with $13.9mn, the GraniteShares 2x Long NVDA Daily ETF (NVDL), $12.1mn, and JPMorgan Nasdaq Equity Premium Income ETF (JEPQ), $9.4mn.

“iShares effectively reallocated their model portfolios to DYNF and pushed in $10bn or so, when it had been struggling before that,” Armour said.

The biggest gainer has been a passive fund, however, admittedly a huge outlier. The VanEck BDC Income ETF (BIZD), which invests in publicly traded business development companies, a type of closed-end fund, may only have taken in $332mn this year, but its gigantic total expense ratio of 13.3 per cent has led to a bumper $19.1mn jump in fee revenue.

The 10 biggest losers include just one active fund — Cathie Wood’s flagship Ark Innovation ETF (ARKK), which with net redemptions of $2.4bn and a chunky fee of 0.75 per cent has lost $7.4mn of revenue due to outflows.

Aside from GBTC, the biggest loser has been the ProShares UltraPro QQQ (TQQQ), which tracks 3x the daily performance of the Nasdaq 100 but has shipped $4.3bn, and with a fee of 0.88 per cent has lost $18.1mn of revenue.

Other big losers include the SPDR S&P 500 ETF Trust (SPY), which has had the largest net outflows of all ETFs at $18.6bn; Grayscale again, with its Ethereum Trust (ETH); and the iShares iBoxx $ High Yield Corporate Bond ETF (HYG).

Next come SPDR Gold Shares (GLD) and the iShares Russell 2000 ETF (IWM). Armour described this duo as “higher-fee beta strategies that have seen outflows likely because of cheaper versions of the same thing”.

Rosenbluth believed active ETFs were likely to continue to grab the lion’s share of revenues from flows, given that their fees were typically around four times those of passive ETFs, meaning they only needed to secure a fifth of flows to achieve parity.

“I think 20 per cent of the flows towards active ETFs is foreseeable over the near term,” he said. “The trend towards active ETFs is going to remain strong. Some investors prefer active management and they are increasingly comfortable using ETFs.”

Armour sounded a note of caution, however. “Wise investors recognise that fees are the best predictor of future success — be mindful of who profits from high-fee ETFs,” he said.

Most active strategies “have had a tough time, compared to just holding the S&P 500 or a similar index that’s extremely cheap.”

Methodology

Morningstar’s methodology factors in when a flow occurs: an outflow in January would have translated into eight months of lost revenue by the end of August, one in February seven months of lost revenue etc. The metric only takes into account fee revenue arising from net inflows or outflows, not changes in revenue due to the impact of market fluctuations on pre-existing assets.